- The Moneycessity Newsletter

- Posts

- Why You Always Sell Your Stocks at the BOTTOM (and How to Stop)

Why You Always Sell Your Stocks at the BOTTOM (and How to Stop)

We are plagued by cognitive bias when navigating the investing world. Making the big decisions when an investment is way down or way up is a recipe for disaster. We cannot eliminate our biases completely, but there are steps we can take to mitigate the damage.

Brian Glass

July 06, 2024

Why is it so tempting to sell a winning stock early? I know in my brain that time in the market beats timing the market.

However, when I’m staring at a big green candle on the stock chart, it’s just so tempting to take those gains and sell early.

Meanwhile, I have no problem holding onto a losing stock, stubbornly holding for it to go back up in value.

Why can’t I just do that with the winners?

There are many cognitive biases in investing, but there are 3 in particular that are the most insidious.

I also came up with a 3-step system that drastically improves my chances of making a sound and logical decision instead of an emotionally compromised decision.

Before I talk about how I overcome them, let me first shine a light on these three biases.

On the go? Watch the video HERE.

Why Do People Sell Stocks Too Early?

Investing Cognitive Biases

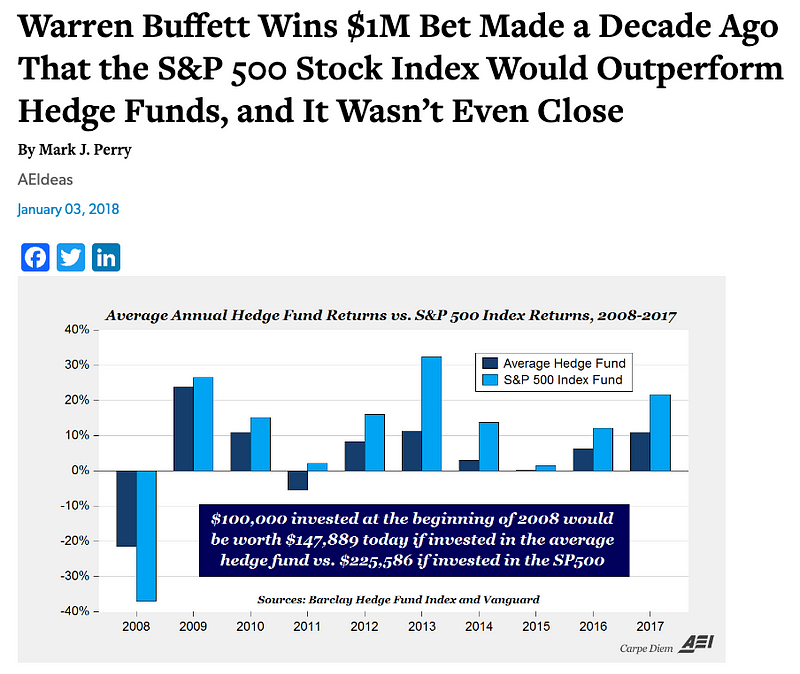

Warren Buffett is famous for his one-million-dollar open bet to hedge funds, particularly the hedge funds that have high management fees.

He bet that the S&P 500 would outperform these hedge funds over 10 years. Only one hedge fund took him up on his offer and sure enough, they lost.

If we invested $100,000 in the hedge fund starting in 2008, we would come away with a little over $140,000 whereas if we invested in the S&P 500, we would come away with over $220,000.

Warren Buffett Bet Against Hedge Funds

If we look at the performance, you can see only in year one did the hedge fund outperformed the S&P 500. They lost 22% instead of the S&P 500 losing 37%. But then every year after that for 9 years, the S&P 500 won.

It’s so hard to beat even for the professionals because it lets its winners ride and it cuts its losers.

So let’s start with cutting the losers.

Anchoring

The reason it is so hard for me to cut my losers is because of the cognitive bias anchoring.

Whenever I purchase a stock, my mind anchors what I believe the fair price to be for that stock at my purchase price.

Even if there’s new information that comes out hurting the value of the company and dropping stock price, my bias is still anchoring my fair value at that purchase price.

In fact, it would even make me tempted to buy more of that stock which in some cases is just the worst thing that you can do.

When you have a bad investment, you need to cut it loose.

Let’s say my stock has dropped and it’s now worth $5,000. I imagine that if I never invested in that stock and I was holding $5,000 in my hands right now, would I invest in that company right now with a new $5,000?

If the answer is no, I’ve got to cut it loose and sell it, especially when there’s the added benefit of tax loss harvesting.

If I sell a company at a loss and get out of there, at least I can use that capital loss to offset a capital gain and save some of my taxes.

Loss Aversion

The second component of the S&P 500 success is letting its winners ride. And the cognitive bias that makes this so hard is loss aversion.

It is so much more painful to lose money than it is to gain money in the stock market.

Because of this, if I have a stock that’s going up, it’s so tempting to lock in those gains because I’m so afraid of losing the gains whereas I should also be equally factoring in the possibility of additional gains.

When I have an investment that has appreciated in value rapidly, I ask myself two questions to give myself a little check: am I having a loss aversion moment or is this company truly risen beyond its fundamentals?

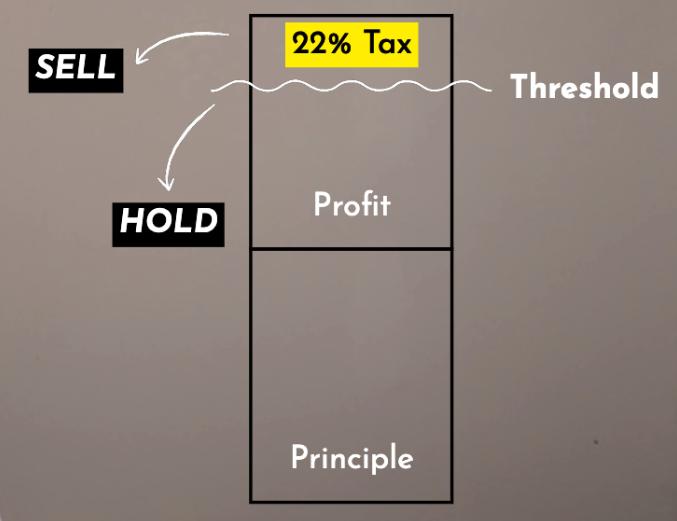

Tax Margin of Safety — Illustration by author

Question 1. If it has risen so much, has new information come out that puts this company significantly higher than what I think it’s worth?

And it has to be significantly higher because if I sell that stock, I’m going to take a tax hit right then.

Say, I’m in the 22% tax bracket. If this stock is not at least 22% higher than what I think my upper threshold is for owning the stock, then I might as well hold it. If I sell it, I know for a fact I’m losing 22% of those gains.

Question 2. Is there another company that I’m equally excited or more excited about that I can put that money into?

Unless there’s a much stronger investment, It’s very risky to sell a company with strong momentum unless it’s just way off the charts.

Mental Accounting

The next cognitive bias is very related to both the loss aversion and the anchoring. And this one tricks me into selling my winners to buy more of my losers or just open a new position.

This cognitive bias is called mental accounting.

It’s where we tend to see the importance of different money differently depending on the position that it’s in.

If money is in the loss category or the principal category, you see it as I need to be less risky with this money whereas if I have money in the gain category, it’s easier for some reason to be more risky with it.

The classic example is when you go to the casino.

If you start off with $100 bankroll and you’re like “All right, I got to make this $100 last the night”. And if you have an early win where you bump up to $200, it’s so easy in your mind to treat the $100 principle differently and guard it more safely than the $100 gain.

This is a cognitive bias.

Money is fungible. It doesn’t matter what category it’s in. It has all the same value and should be treated with the same risk profile.

So what can I do to stop my own brain from betraying me when I’m investing?

I’ve given this question a lot of thought and I came up with a 3-step system that drastically improves my chances of making a sound and logical decision instead of an emotionally compromised decision.

My 3-Step System

Step 1

The first step of my system happens when I buy a new stock, I make reasonable expectations and a plan for what I’m going to do in different scenarios.

I make a limit sell order and a stop loss order for if it rises above my fundamental analysis or falls below my fundamental analysis.

Using Automation to Sell — Illustration by Author

Now that’s great, but there will be new information that comes out that I will have to react to in the moment. So setting your stop loss and your limit sell is a good start, but it can’t be all I do.

This is where step two of my system comes in.

Step 2

It’s whenever I have to make a new decision and change my stop loss or my limit sell, I have to be acutely aware of my biases.

I have to remember that I can never eliminate them completely because whenever I stop thinking about them, that’s when I get bit.

So whenever I’m making a new change to a stop loss or limit sell, I have to read through the biases that I commonly fall victim to make sure they’re just fresh in my head so I can have better chance of overcoming them.

Step 3

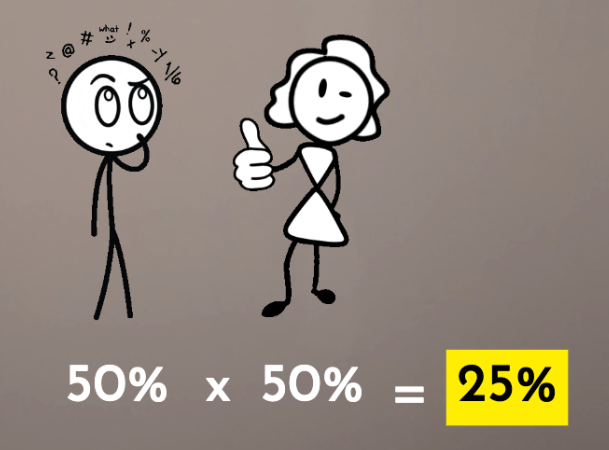

And then the third step is checking with an accountability partner.

For me, it’s a spouse check. Natalie and I always talk to each other before we make a big buy or sell of a stock.

I start by telling her my plan and my expectations. And then in the moment if I’m getting a little bit emotional, she can remember what my thesis was for that investment, recognize if I’m breaking away from that thesis, and ask probing questions accordingly.

Strength in Numbers — Illustration by Author

If there is a 50% chance that I’ll be emotional and make a mistake and a 50% chance that she’ll be emotional and make a mistake, combined there’s only a 25% chance that we’re both going to make a mistake.

So it really cuts our odds in half of making a mistake if we always bounce those ideas off of each other.

So What Now?

Another option that has been incredibly effective for me in eliminating the chance of biases coming into play is investing in ETFs.

An ETF or an index fund will handle the share rebalancing automatically. So I don’t even have to worry about making a mistake, falling victim to a cognitive bias and selling a winner and doubling down on a loser.

So if you’re curious to see how I evaluate ETFs and how I pick ETFs that tend to outperform the S&P 500, check out this video right HERE.

Catch you on the flip side.

Reply