- The Moneycessity Newsletter

- Posts

- Is VENTURE X Still The Best Card for 2024?

Is VENTURE X Still The Best Card for 2024?

Quantifying the points from different credit cards and comparing them apples to apples is a daunting task. I built a comprehensive credit card spreadsheet that compiles all the best cards from Chase, Capital One, and American Express. Just enter your budget to learn which card is mathematically the best for you.

Brian Glass

September 28, 2024

I have made $4,159 in points over the last year using one single credit card. But is it still the best credit card?

To find out, I’ve compiled all the relevant credit cards in my spreadsheet from Chase, Capital One, and American Express. These are the premier travel credit cards, and I’m going to use real spending examples to find out mathematically which credit card is returning the most value.

On the go? Watch my video HERE.

Is VENTURE X Still The Best Card 2024?

My Favorite Card Last Year

First, the credit card that I’ve been using over the last year which has got me so much value is the Capital One Venture X credit card.

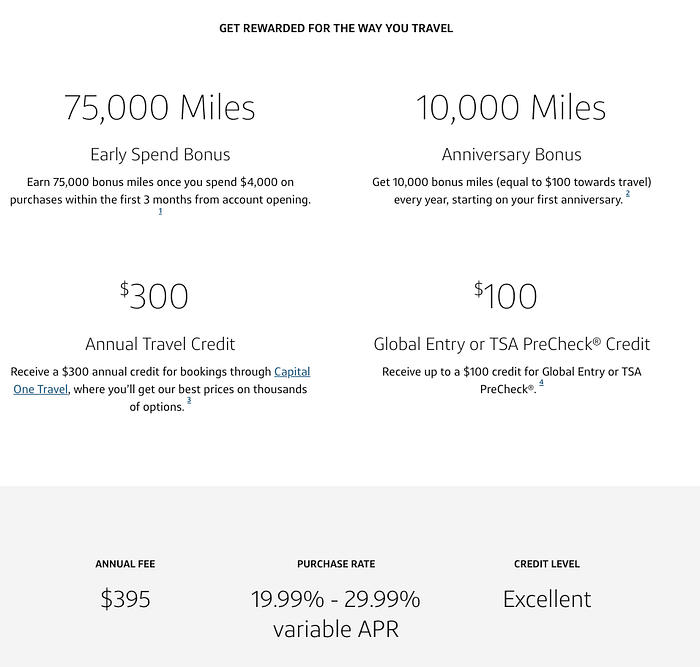

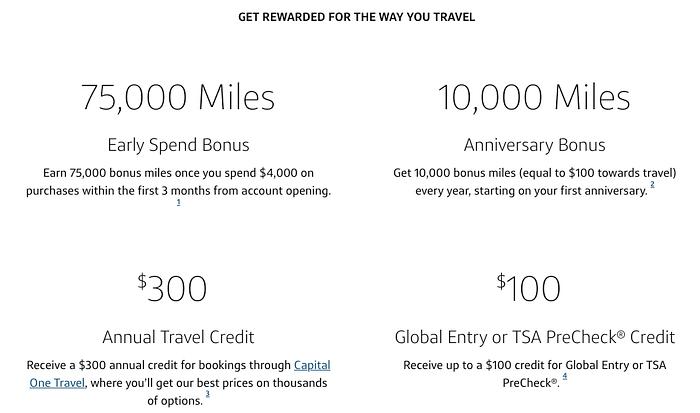

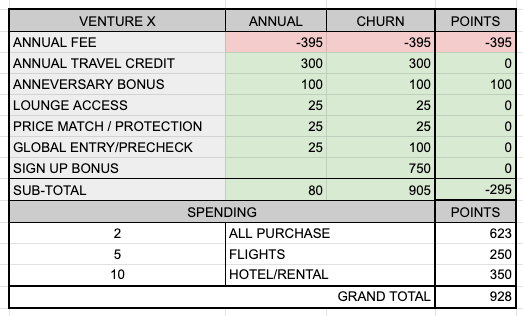

Annual Fee

This is a travel-oriented credit card with a high annual fee of $395. However, don’t let that scare you because it has tons of free bonuses that make the annual fee irrelevant.

Venture X Travel Credit Card

I get $300 every year in travel credits. So as long as I’m taking one trip per year, one flight is all it takes and $300 is taken out of that annual fee which for me is guaranteed. I’ve got family out of town. We’re going to take at least one vacation. That $300 credit is happening.

Venture X Bonuses

And then on my anniversary, I get $100 in free points. So instead of a $395 annual fee, it’s really just a $5 credit guaranteed every year to hold this credit card.

That’s one reason why I’m a huge fan of the Venture X but let’s get on to where I’m getting my points.

Travel Credit

So in travel credits, I got the $300.

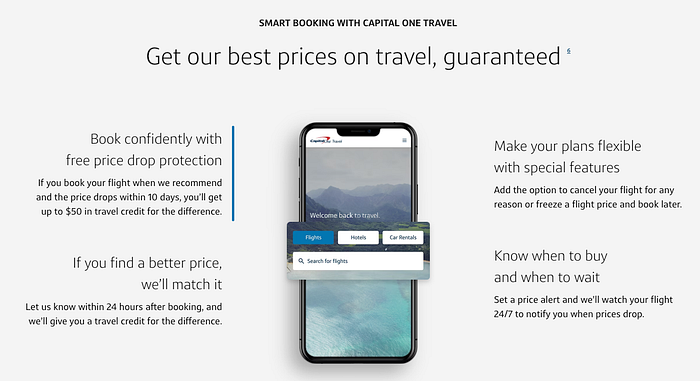

Price Protection: I got $130 and this was not a perk that I knew existed until I did an audit of where my points were coming from. Over the next 10 days, if the price dips, I get a credit for the difference up to $50. We took a lot of trips in the last year so I got a lot of credits for that and I didn’t even know that was a thing.

Price Matching: A big complaint on using the travel portals is that they jack the prices up on the portals to compensate for the perks that they give you. Well, on Capital One that’s not a concern because if you look at the direct pricing with the airlines, if it’s a cheaper price, you can get that price matched and then you still get price protection if the price drops on the portal over the next 10 days so that’s pretty big.

TSA Pre-check/Global Entry: Every 4 years, when I renew either of those memberships, I get a $100 credit towards that.

Venture X Price Protection

Basic Spending

For just basic spending, I got $2,578 in points.

2 miles per dollar spent on all purchases

5 miles per dollar spent on flights and vacation rentals booked through the Capital One portal

10 miles per dollar spent on rental cars and hotels

Venture X Miles per Dollar Spent

Lounge Access

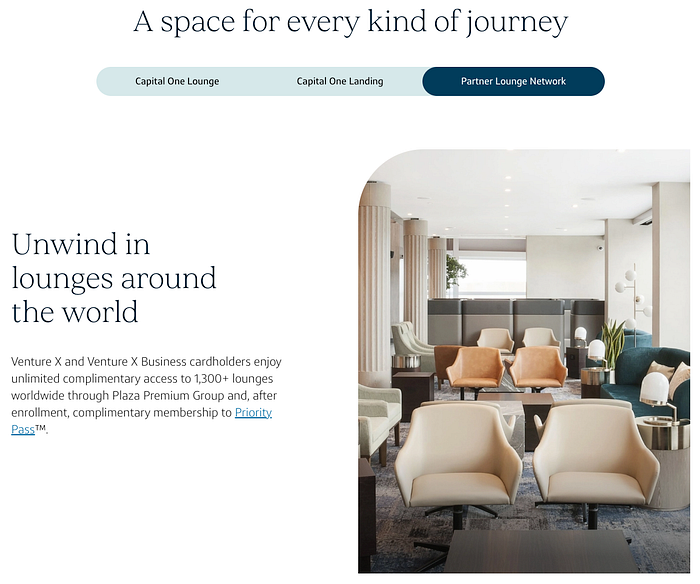

I got $300 in lounge value, and this is another one that I could take more advantage of next year. At first, I thought I was only able to go to the Capital One Lounge but after looking at the fine print, I’ve now realized that I have access to the Priority Pass which gives me access to thousands of lounges worldwide. So, it should have been $600 in value.

Capital One — Priority Pass

Annual Bonus

My annual sign-up bonus, in this case, was $750. On my anniversaries, it’s only gonna be $100 going forward.

Captial One Annual Perks

This totals to $4,159. Now, if I subtract the annual fee, my net benefit would be $3,764. Clearly, the Capital One Venture X is a badass credit card, but is it still going to give me the most value?

My Credit Card Spreadsheet

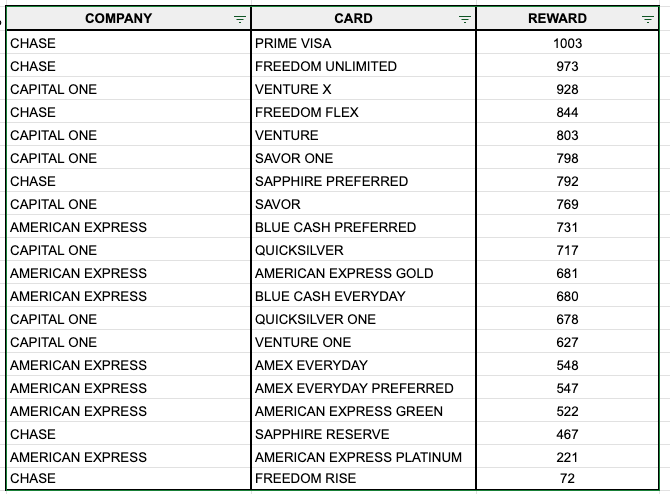

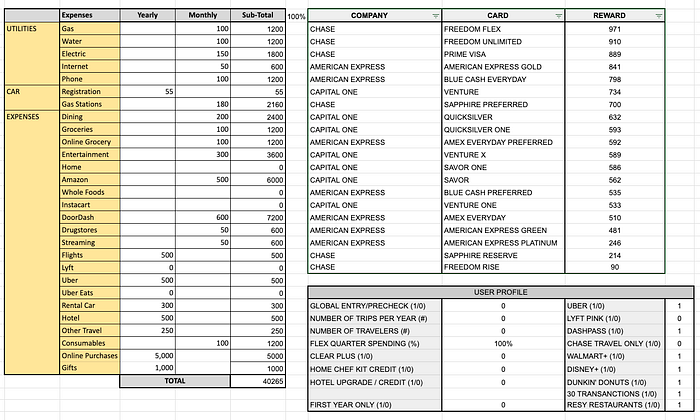

So here is my dashboard on my credit card spreadsheet.

Budget

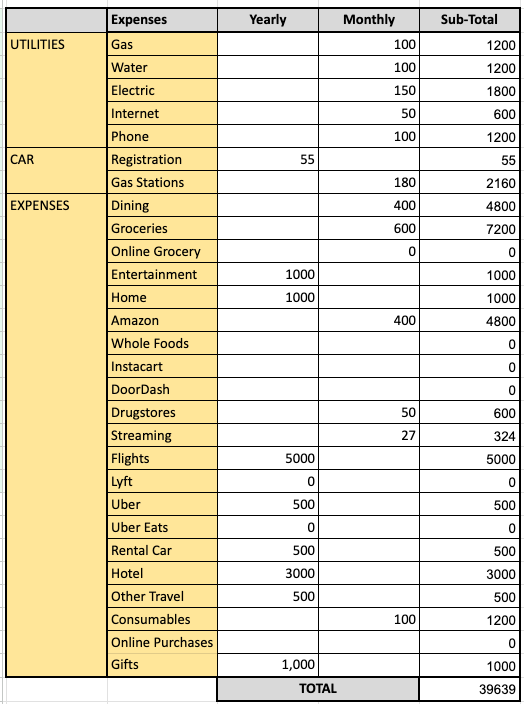

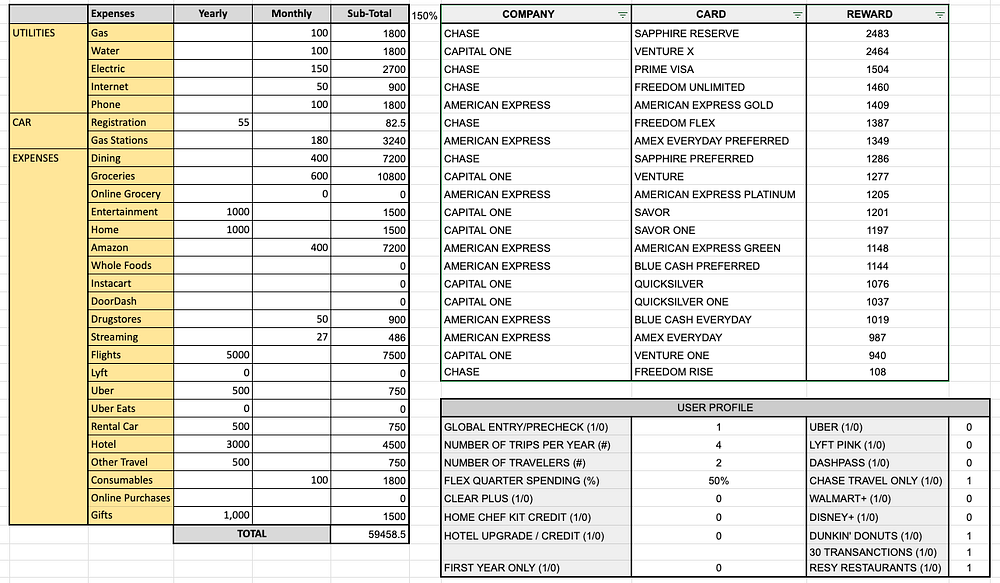

The first section on the left is my budget of roughly how much I’m planning to spend on my credit card. I’ve got every category you can think of but most importantly, I have all the categories that are showing up on the credit cards. Some spending categories are going to affect a bonus or if different spending categories are going to give more or less points per dollar spent, those are broken out on this budget.

I’ve got all my utilities, gas, water, electricity, internet, and car expenses. And then the expenses section is just your typical credit card expenses so I’ll hit some of the bigger categories that are going to be the ones that really drive which credit card is going to be right for us.

Dining: $4,800

Groceries: $7,200

Amazon: $4,800. My wife is an Amazon fiend

Flights: $5,000

Hotels: $3,000

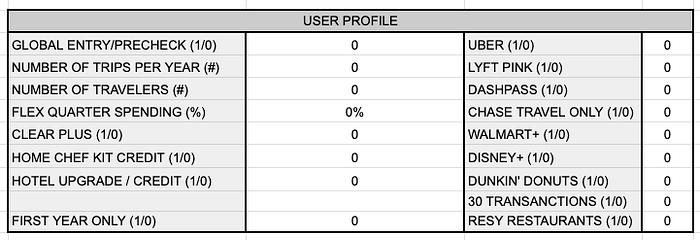

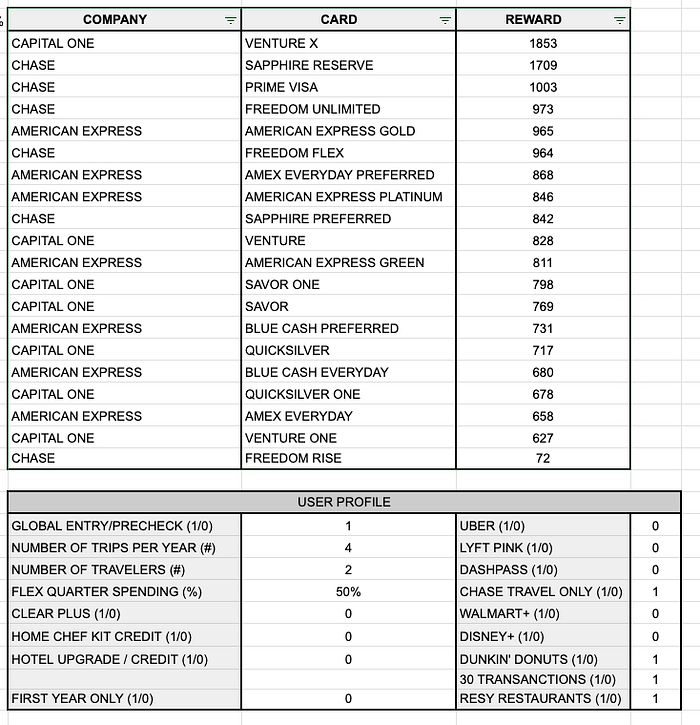

User Profile

The user profile section in the bottom right section is where I determine which bonuses I’m actually going to take advantage of.

Right now, I’ve got zero in all of these categories. And most of them, I either put a one or a zero. A one for yes, I’m going to take advantage of it, and a zero for no, I’m not. For a couple of these, I need to actually put in a number or a percentage other than one or zero.

So all of these user profile numbers will affect how many points the backend tabs are calculating. For example, if I go to the Capital One tab, I can see Venture X.

On the right, all of these points are for annual travel credit. This is a zero because I have zero trips per year so it’s not tallying in the annual travel credit. For lounge access, it’s got a zero in there because it does not count any travel per year. Price match protection, another zero. Global Entry/Pre-check, that’s a zero. Sign-up bonus, that’s a zero because I’ve got a section here for the first year only.

This is for when I want to look at churning a credit card because some credit cards give you a lot of bonuses in that first year alone. But for this pricing exercise, I don’t want to know about year-one-only bonuses. I want to see which card is going to be the best year after year after year.

Ranking

The final section in the top right of this dashboard is the ranking of the credit cards.

Currently, this ranking is taking into account my current spending and my current user profile which is a zero across the board. With that in mind, the best credit card for me currently is the Prime Visa.

My Top Credit Card This Year

It’ll be interesting to see how this ranking is going to change after I start changing my user profile.

Global Entry/Pre-check: My wife and I will utilize that. So I’m going to put one in that category.

Number of trips per year: We’re expecting four trips in the next year.

Number of travelers: I’ll put two for my wife and I.

Flex quarter spending: This is for the Chase Freedom Flex card. We think we’ll hit the 50% of the Chase Flex spending categories that change every quarter.

Clear Plus or Global Entry/Pre-check: We’re not going to use it.

Home Chef: This is where they ship you pre-packaged meals for you to cook at home. We don’t do it.

Hotel upgrade credit: This is something that I could only utilize with American Express if I was going to be staying at hotels for sure every time in their hotel program. I don’t think we will. Sometimes we hit Airbnb so I’m going to leave a zero in that category.

First-year only: I’m going to keep a zero because I want to know beyond the first-year bonuses.

Uber: We don’t use it.

Lift Pink: No.

DoorDash: No.

Chase Travel: Yes. I would use the Chase Travel portal if a Chase credit card came up.

Walmart Plus: We don’t use it.

Disney Plus: They went downhill.

Dunkin’ Donuts: Sure. Why not? I could use some donuts.

30 transactions/month: I’m going to say yes.

Resy Restaurants: This is for making reservations at special restaurants. I’ll put a yes there

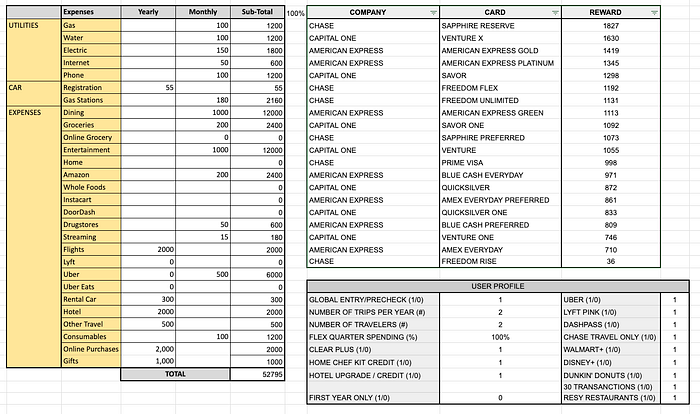

So after filling out that user profile section, I will now go to the top right table to find my top credit card.

And once again, the Capital One Venture X is the top credit card for me. This is calculating the $1,853 minimum in value that I would receive if I stick to this spending profile.

Now, one thing to note about these travel credit cards is the more you spend, sometimes a different credit card will jump out on top. And then if you’re spending less, a different credit card might win.

There is a cell on the top left of this table where I can decide if am I gonna hit 100% of my budget or hit less or more.

So first, let’s check and see if I spend 150% of my budget. I’ll re-sort for the top credit card and now the Chase Sapphire Reserve is just barely on top of Venture X by about $19.

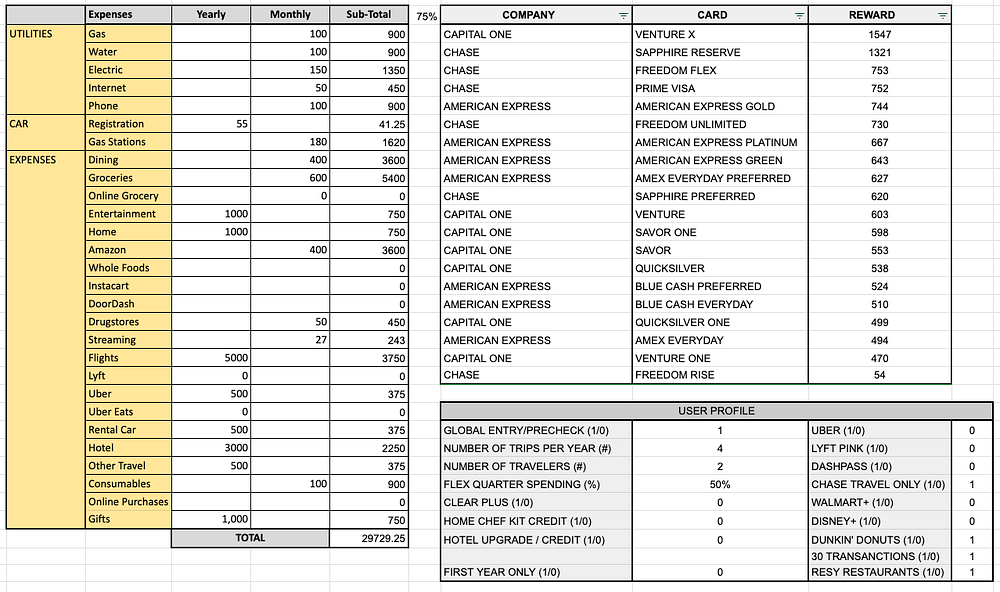

Now let’s check the other end. If I’m only spending 75% of my budget and re-sort from best to worst. And the Venture X is still on top with Chase Sapphire Reserve in second place.

Which Credit Card is the Best For You?

Clearly, the Capital One Venture X credit card is undisputedly the best credit card for my type of spending. But what credit cards are going to be the best for some of y’all out there who don’t spend money the way I do?

The Hermit

So the first type of person I want to look at is the hermit build who doesn’t go on flights, travel, or go out to restaurants as much. They want to have stuff brought to their door so they’ll do Amazon, DoorDash, and other online purchases.

In the budget section, you can see the top-hitting categories now are Amazon while dining and groceries have gotten lower. DoorDash is up there at $72 per year. I left $500 in there for flights and $5,000 per year for online purchases.

In the user profile section, I’ve zeroed out all of the travel-related user profile perks. So we’ve got 100% on the flex quarter spending.

I’ve got one in there for Uber, one for DoorDash. Walmart plus, sure. Disney plus. Dunkin Donuts. Yes to 30 transactions. And no to the Resy restaurants.

So with this user profile and this type of spending, the top credit card is now the Freedom Flex credit card. In fact, the top three credit cards are all Chase credit cards: Freedom Flex, Freedom Unlimited, and Prime Visa.

Now, you can tweak some of the spending and some of the user profiles to see which credit cards come out on top in different situations.

If you didn’t think you could hit all four quarters of the flex spending (they change the category on you every quarter), you can set the cell to the top left of the Ranking table at 50% and do a re-sort. Now the Freedom Unlimited is on top.

If you’re spending 75% of your budget, the Freedom Flex is now on top.

If you’re spending 150% over budget, the Freedom Unlimited is on top again. It’s no longer the Freedom Flex.

The Spender

The next type of spender I want to look at is the person who likes to go out for dinner. They like to go out to the bars.

In the budget section, I’ve got way more money in the dining category and $1000 per month in the entertainment category. I’ve trimmed flights and hotels down to $2000 and also trimmed down the online purchases.

In the user profile section, I’m assuming two trips per year for two travelers. We’re going to keep the flex spending. And then on the right, I’m putting in everything. We got Uber, Lyft, Pink, Dash Pass, all of it.

So with that in mind, the new top credit card is the Chase Sapphire Reserve.

If you exceed that budget at 150%, the Chase Sapphire Reserve is even more so on top.

And then if we trim the budget down to 75%, Chase Sapphire Reserve is still on top.

So What Now?

You can see with the different types of spending, the different types of user profiles, you can use this spreadsheet to see which credit card is going to be the best one for you.

However, this spreadsheet is only looking at one credit card at a time. Click HERE where I share the best combination of credit cards with the least amount of cards.

Catch you on the flip side.

Reply