- The Moneycessity Newsletter

- Posts

- 4 Unusual Investments You Can ACTUALLY Do

4 Unusual Investments You Can ACTUALLY Do

What is the best unusual investment for passive income? We have all been told to invest in assets but that’s like your doctor telling you to eat healthy. It’s super vague and very difficult to start. Most of conventional wisdoms were just either stock-related or not passive at all. Out of frustration, I decided to make my own list of UNUSUAL, PASSIVE, and EASY investments that I can begin from my phone.

Brian Glass

May 13, 2024

We’ve all been told to invest in assets, but that’s like your doctor telling you to eat healthier. It’s super vague and it’s difficult to get started.

Maybe you have considered real estate because you like the idea of passive income, but it is really expensive. It has a high barrier of entry and with a single house being so expensive, it’s hard to get diversification. I don’t want all my eggs in one basket.

Maybe you’ve considered trading stocks or options, but like me, you have two cats and you just can’t afford the volatility of the market.

When I was browsing Reddit on the toilet as one does, I came across a post that really sparked my interest.

REDDIT POST: What are the best sources of information for discovering unusual investments?

Unfortunately most of the comments were stock related.

Then when I took my search to Google, I searched for unusual or alternative investments and all of the lists pretty much looked the same: gold, fine wine, expensive art, Pokemon cards….

The problem with all of these investments is they are not passive at all. It’s like me buying a second job for myself. I would have to constantly buy items, store them, organize them, and then sell them just to make a profit.

Out of frustration, I decided to make my own list of four unusual, passive, and easy investments that I can start on my phone on the toilet.

Let’s go.

On the go? Watch the video HERE.

1. Real Estate (not REIT)

On nearly every single list of alternative or unusual investments, you can find some reference to real estate whether that’s investing in haunted houses, dude ranches, or drive in movie theaters.

My issue is the same:

High upfront cost

Lack of diversification

Having to manage the thing.

Don’t get me wrong one day I would love to have enough money to invest in vacation rentals across the world in the most beautiful and fun locations. But until then I want a way to invest in these rentals without putting all of my eggs in one basket.

To me, what is appealing about investing in vacation rentals and even single family homes is the income generation, the capital appreciation, and the relative safety of the sector. And right now, single family homes are in really high demand.

Housing Market Prediction for 2024

I found a way to make all that happen without needing to fund the entire investment, doing the work, or needing the expertise.

You can invest in fractional ownership of vacation rentals on a fund like Arrived which is actually backed by Jeff Bezos and it allows you to buy fractional ownership in single family rental homes and vacation rental properties.

Forerunner, Bezos back Arrived, a startup that lets you buy into single-family rentals for ‘as little as $100’

I can invest as little as $100 into an individual property, whether that’s a vacation rental or a single family home. Or if I want to build up my diversified exposure faster than I can invest directly into a portfolio of many different single family rentals. Unfortunately, they do not have a fund for vacation rentals yet. I hope they do have that option in the future.

Of course, there are more traditional ways that you can gain exposure to single family homes in a diversified way by investing in a REIT which stands for Real Estate Investment Trust. It trades like a stock and it gives you diversified exposure to many different types of real estate depending on the individual REIT that you’re investing in.

Vacation Rentals on arrived.com

However, REITs do not allow you to invest in an individual vacation rental like Arrived. In fact, I’m not aware of any REITs that primarily are invested in vacation rentals. If you are familiar with one, please let me know in the comments, I would like to read up on it.

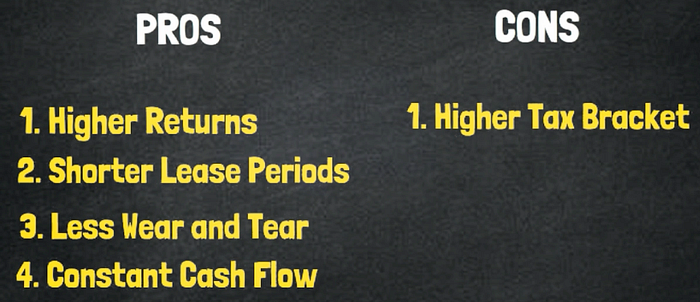

Investing in vacation rentals resonates with me a bit more than investing in individual single family homes because you have a greater potential for higher returns.

Illustration by author

I can also get other little benefits from having shorter lease periods as the property will be less likely to have catastrophic damage. I won’t be surprised when a multi year tenant moves out and has completely trashed the place.

While it is nice to receive a constant flow of extra income, there is one downside associated with investing in real estate funds, and REITs for that matter, that is the tax implications.

The bulk of dividends received from rental properties are taxed as regular income, as opposed to qualified dividends, which have lower taxes (at least for now as of 05/2024).

Illustration by author

For instance, if I held a dividend stock for more than a year, the dividends would be taxed at 0% for earnings under $95,000 for a married couple, and then only taxed at 15% above $95,000 in earnings and all the way up to a yearly income of $584,000.

On the other hand, the majority of my real estate income would be taxed at our regular income tax bracket, which would be 12% for earnings under $95K and then 22% for earnings above $95K.

2. Municipal Bonds

These tax issues led me to my second uncommon investment. This one is incredibly safe and gives me the ability to make passive income tax free.

The higher my income, the more valuable this investment is to me.

Let’s use the same assumption as before.

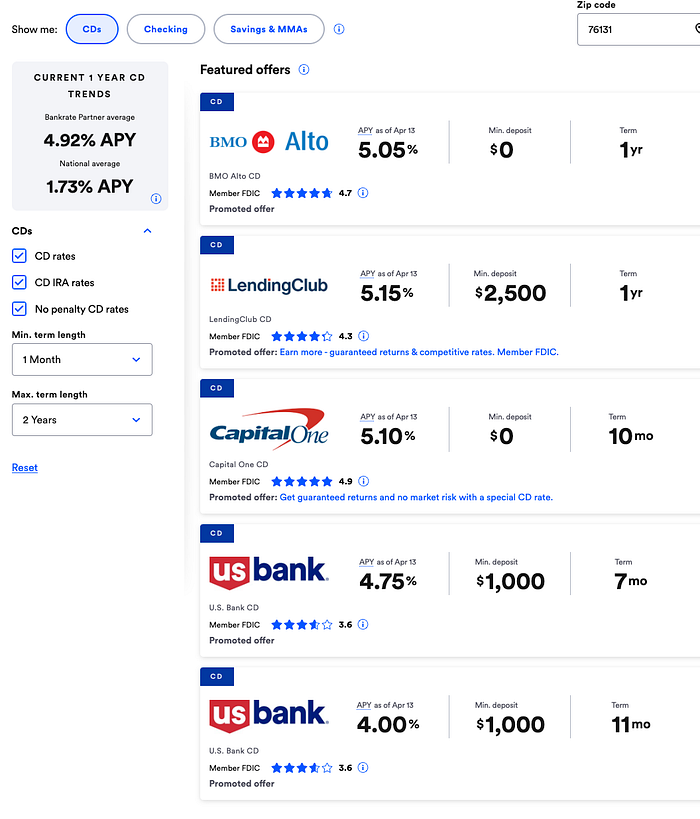

My wife and I have a household income of $95K and we want to invest some extra money for additional passive income. We’ve got a few common options, which would be to stick our cash in a high yield savings account or to buy certificates of deposit (CDs).

Best CD Interest Rates on Bankrate

According to Bankrate, the best rate for CDs at the moment is around 5.15%. Because we would have to pay taxes on those extra gains, the effective yield would be dropped from 5.15% down to about 4%. And that rate would only be guaranteed for one year. If interest rates were to drop, then you would not be able to find CDs with a rate of above 5%.

I was not impressed by this arrangement because I went longer term and higher yields. This led me to discover municipal bonds. I can take advantage of the high yields now, lock in those rates for many years, and make all this income tax free.

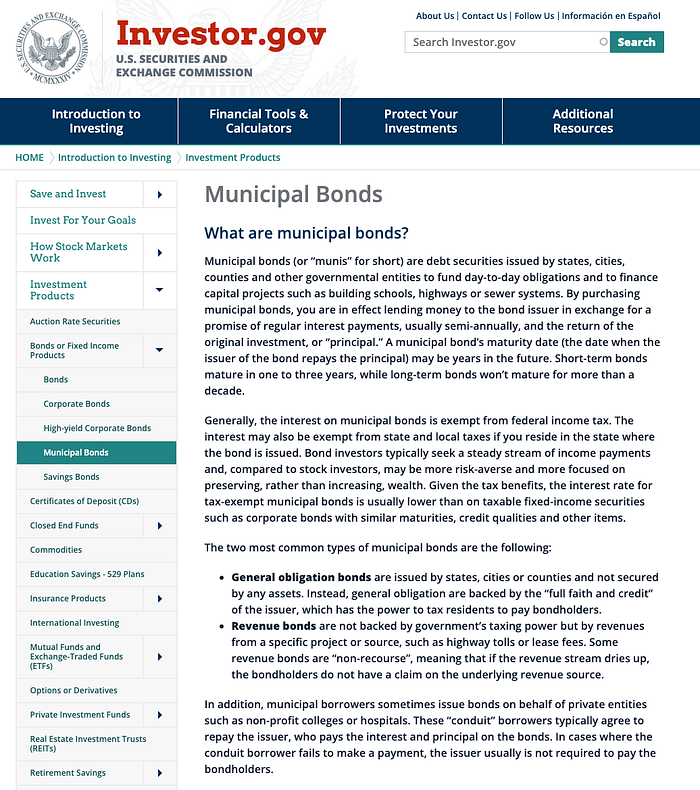

What are municipal bonds

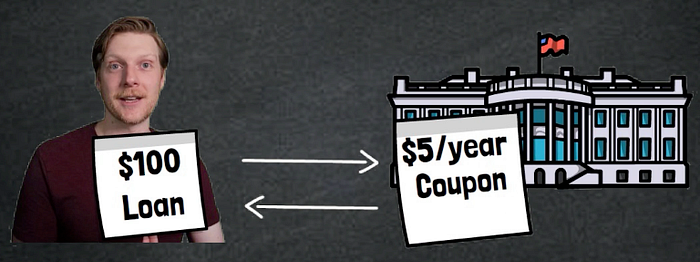

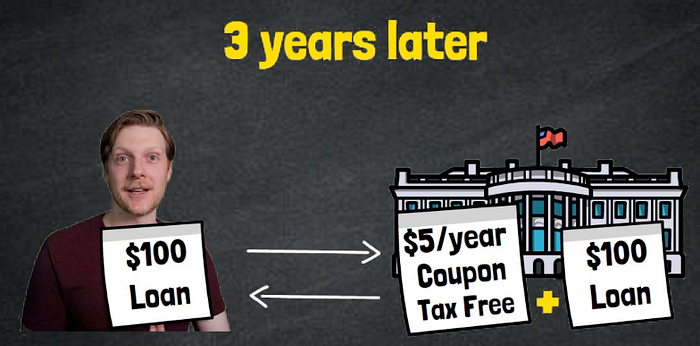

A municipal bond is a debt security that is issued by a government entity. In other words, you are loaning the government money and they are paying you a dividend over the life of the loan until they pay you back your principal when it expires. Except in this case, the dividend is called a coupon.

Illustration by author

Eventually the bond expires. This is known as reaching maturity where the government entity pays you back the principal that you loaned and all the coupons you made are the tax free gains.

Illustration by author

Municipal Bond Examples

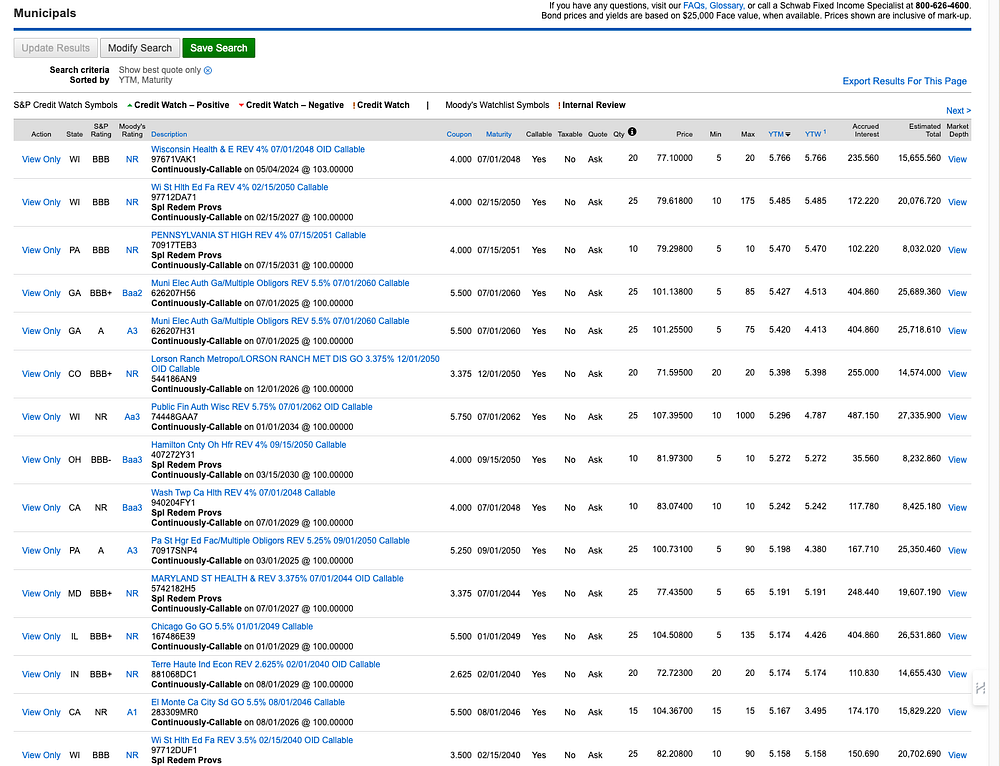

Here are some examples on Charles Schwab of municipal bonds that I could buy right now.

Municipal Bonds on schwab.com

The first thing that I like to look at is the YTM and the YTW. This stands for yield to maturity and yield to worst.

The yield to maturity (YTM) is your total return that you would receive, expressed as an annual rate if you were to hold that bond until it expires.

The yield to worst (YTW) is the total return that you would receive expressed as an annual rate if the bond is called early.

When I say called early, what I mean is some bonds can be closed out early by the government entity if they decide to pay you back your principal early. In this first example, the third line under the description says that this bond is continuously callable on May 5th of this year, even though the maturity date is July 1st of 2048.

The reason a government entity would want to call a bond early is if the interest rates dropped, they can get a new loan at a lower rate and pay back the old loan, which was at the higher rate.

Illustration by author

So back to our example, the yield on this bond is 5.766% which is a pretty damn good yield.

Next. I like to look at the call away date. In this case, anytime after May the 4th. You can expect this bond to be called away if rates drop in a significant way. Now, what we’ve been hearing in the news, the Fed might be increasing rates this year. But, you cannot count on holding this bond for a long time just because it’s callable any time after May 5th. You never know what the interest rates are going to do.

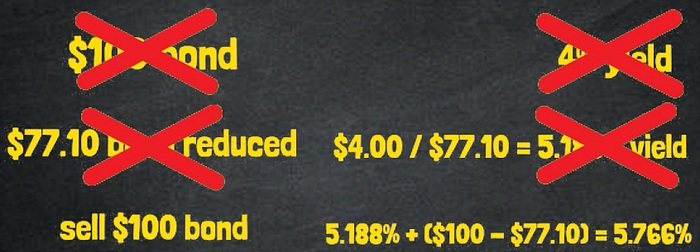

Next we look at the current price and compare it to the face value. The current price on this bond is $77.10, which means it is trading at a discount. If the bond gets called early, then we would get paid $103, not $77.1. The main reason a bond would trade at a discount is if interest rates increased since the inception of the bond. We can see in this case that the coupon is $4 on a $100 bond. This is considered a low rate, 4%.

Municipal Bonds on schwab.com

Why would anybody buy a $100 bond at 4% when they could just put their money in a high yield savings account and get over 5%?

For this bond to be competitive, the price had to drop so that the effective yield would increase. A $4 coupon on a $77.10 bond is a 5.188% yield.

Illustration by author

Then after adding capital appreciation when we sell it for $100 at maturity or $103 if it gets called early, it brings the yield even more up to 5.766%.

Illustration by author

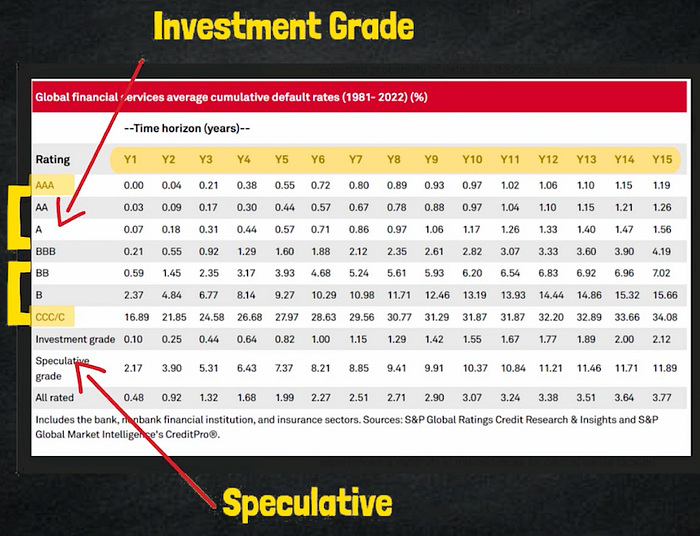

4. The final thing to look at is the credit rating. The highest credit rating and therefore the least risk is a AAA rating, while the lowest rating and the most risk is a C rating. Anything at or above BBB is considered investment grade and anything lower is considered speculative.

Generally a higher rating gives you more security, but a lower yield while lower ratings give you less security, but in return you get a higher yield return.

I like to look at the historical data on different grades of bonds to get a feel for the risk levels.

Illustration by author

You can see on this chart that we have different ratings, percent failure rate over different time horizons. The time horizons go from 1 year all the way to 15 years and the ratings go from AAA down to C through CCC.

The bond that we’re looking at has the lowest level of investment grade, which is BBB which historically fails 4.19% of the time after 15 years. That’s a little bit risky for my taste so I’m going to look for a bond that at least has an A rating. An A rating historically fails 1.56% of the time after 15 years.

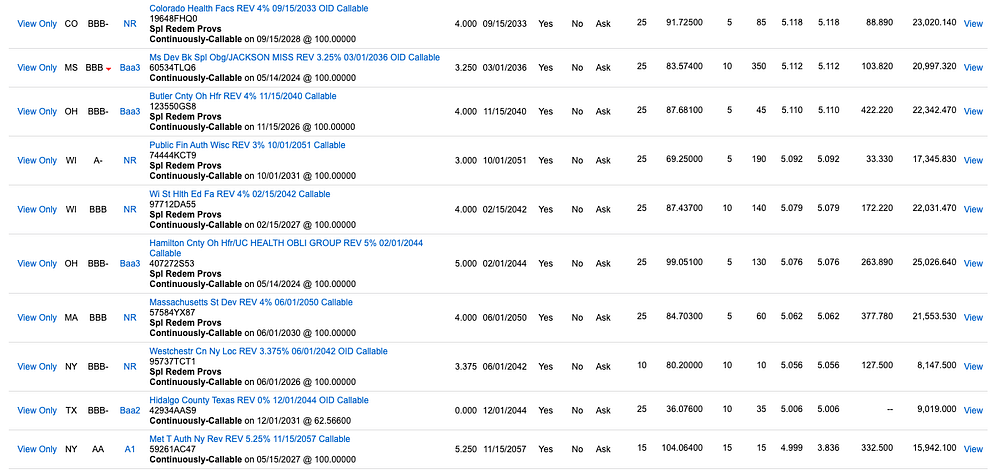

Municipal Bonds on schwab.com

If we scroll down to a bond that has this rating, this bond has a yield to maturity of 5.092%. It has an A rating and can be called anytime after October 1st of 2031 and currently is trading at a solid discount. It is trading at $69.25.

Municipal Bonds on schwab.com

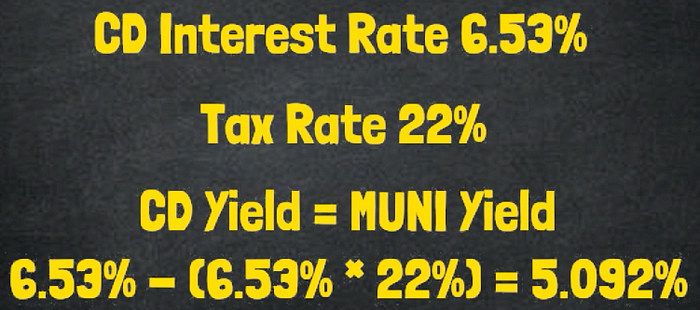

With a tax free yield of 5.092%, this municipal bond would perform as well as a taxable CD that’s a certificate of deposit that has a yield of 6.53% and it would last a minimum of 6 years since it is only callable in October of 2031.

Illustration by author

So with a municipal bond, not only can we get longer guaranteed durations, we can also get a higher yield which means more passive income for me.

3. Collectibles (not Pokemon Cards)

Before I get to my personal favorite of the unusual investments, I do want to address the most common one.

These appear in so many lists that I see on Google, and there is a huge variety. I’m talking coins, Pokemon cards, fine wines, whiskeys, watches, you name it.

Unusual Investments that are Reinventing the Market

I’m talking about collectibles.

If you really know the market, then you can find success with this strategy of buying, storing, and selling these collectibles down the road for a profit.

For instance, if I was going to do this, I could probably make a profit selling rare bourbons. I know the market pretty well, and I know I’ve seen rare bourbons on the shelf.

Ultimately, I decided against it because it is just too much work and I would be tempted to drink my investments.

Anyway, one thing I did want to add to the conversation on collectibles is magnifying your returns by combining this strategy with churning credit cards.

If you are collecting items that can be purchased with a credit card, then it would be easy to stack up the signup and cash back bonuses.

Illustration by author

For instance, if I managed to buy and flip $6,000 worth of rare bourbon using the chase ink business credit card, then I would earn $750 from the sign-up bonus and another $90 in cash back. In total, that would increase my investment returns by 14%. And 14% is pretty good especially considering the average annualized returns for the S&P 500 is 10%.

So yes, the returns on collectibles can be pretty good especially when you combine them with credit card churning, but it is hardly passive between managing several credit cards and flipping a bunch of items.

In my opinion, this is closer to a side hustle than a passive investment.

4. Preferred Stocks

If you are only looking for passive income, then this next unusual investment is the way to go. If a stock in a bond could make a baby, this would be it.

This investment has the high yield of a corporate bond, but it also has the favorable tax structure of a dividend stock.

I’m talking about preferred shares of stock.

And yes, this is an actual category. It doesn’t just mean stocks that are good. These are like corporate bonds.

Companies issue these stocks when they’re trying to raise capital, and they pay a very high yield.

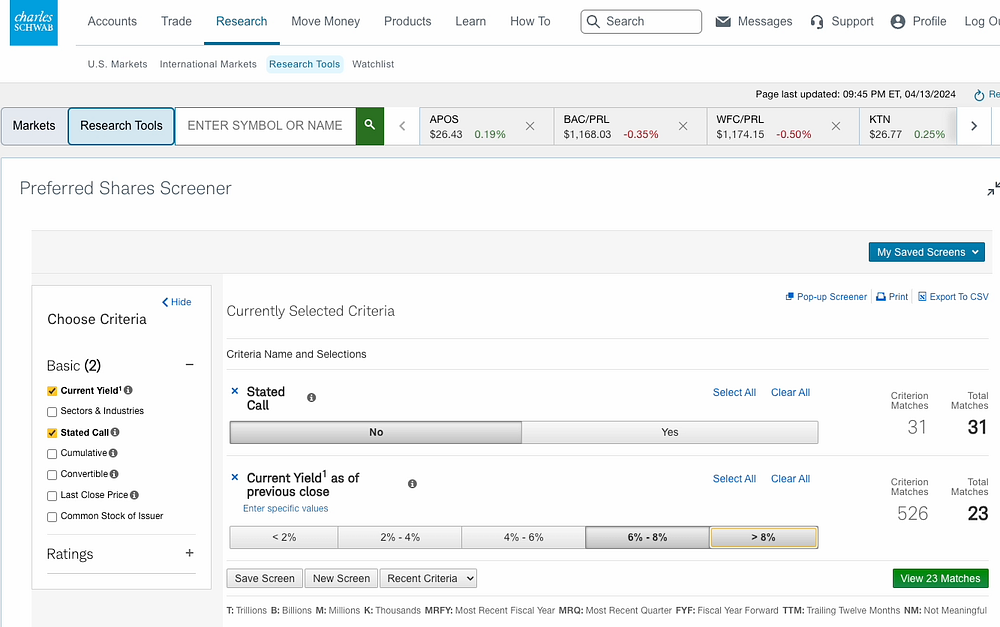

There are many different flavors of preferred stock, and they have a lot of different components, so you do have to look at the details, but the ones I like to focus on are relatively simple.

1. No Call Preferred Stocks

Sometimes a preferred stock can be called away early, similar to what we saw with the municipal bonds. These are callable, but the ones I like to invest in are not callable.

Preferred Stocks on schwab.com

2. Constant Preferred Stocks

Other types of preferred stocks can have a constant yield or a variable yield. Stocks that have a variable yield can change their yield as interest rates go up and down. I don’t like this, so I like to invest in preferred stocks that have a constant yield.

Preferred Stocks on schwab.com

The only way that it can change a little bit is if the share price goes up and down, which indirectly affects the yield but the dividends are always constant.

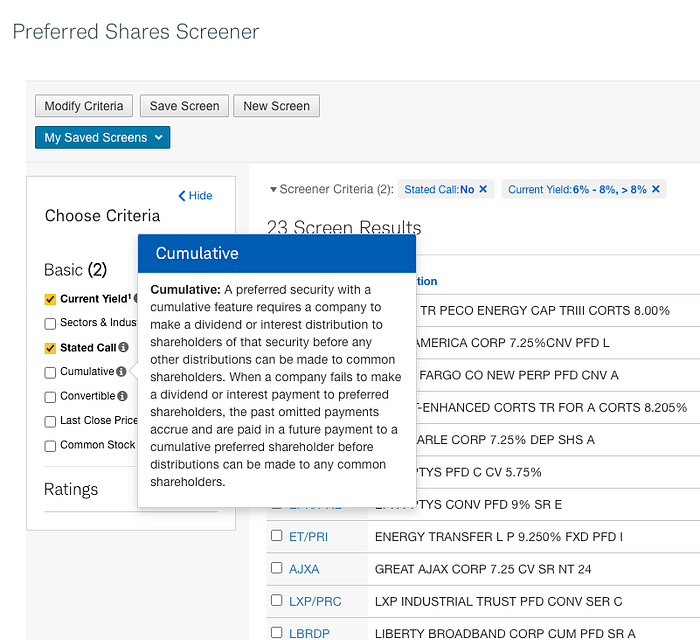

3. Cumulative Preferred Stocks

Apart from having a high yield, it is also nice to invest in a preferred stock that is cumulative. This comes into play whenever the company gets in trouble and has to pause their dividend.

Preferred Stocks on schwab.com

As soon as the company is able to resume their dividend, they are obligated to pay their preferred shareholders all of the dividends that they missed while it was paused, while the company is not obligated to pay all of its common stock shareholders. So this is a nice way to ensure that you’re going to get all of the dividends that you planned on getting, although you might get them a little bit late.

Another little bonus on preferred shares in general is that a company generally is obligated to pay out its preferred shareholders first if it goes out of business and has to liquidate its assets. So you get a little bit of a downside protection there if you invest in a preferred stock.

No Call and Constant Preferred Stock Examples

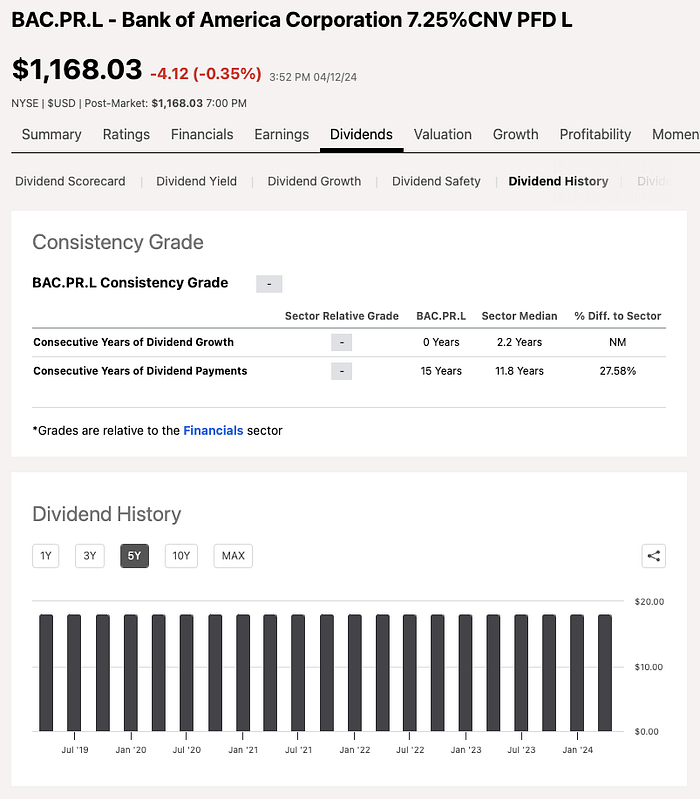

The first two preferred stocks that I want to show you are from well known and well established banks: Bank of America and Wells Fargo.

Preferred Stocks on schwab.com

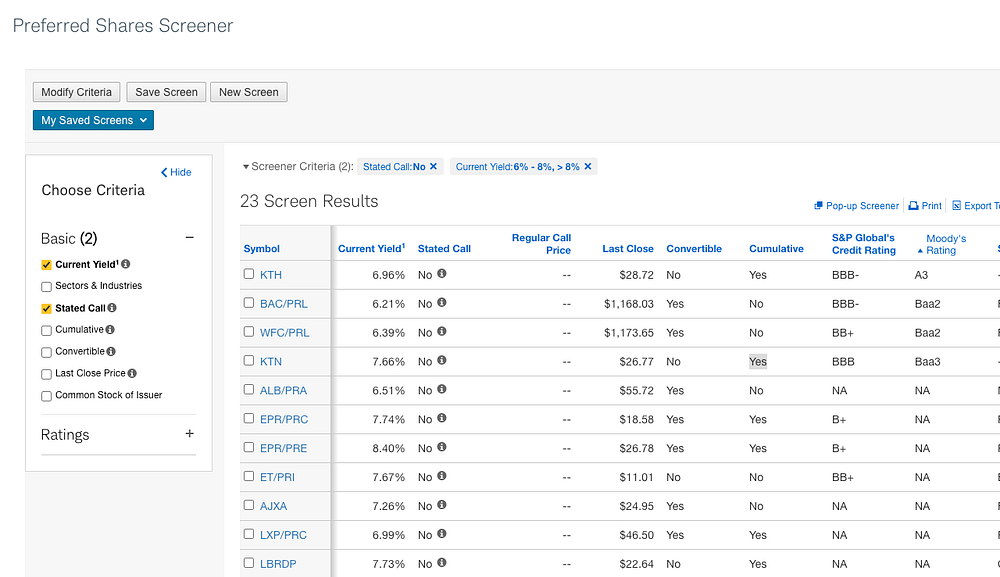

Both of these preferred stocks are trading at a solid premium, about 17% because they are pretty sought after. The face value of the shares are $1000 and both are yielding a little bit over 6% at the time.

If you buy one of these shares, you can count on receiving about $70 every year for the rest of your life at least while these banks are still around.

Unfortunately, neither of these preferred bank stocks are cumulative, so if they get in trouble and have to pause their dividend, you will be missing out on income just like all of the common stock shareholders.

Preferred Stocks on schwab.com

This is unlikely to happen because both of these preferred stocks have a very high credit rating with Standard Poor and Moody.

If you go to Seeking Alpha, you can see that both of these banks have consecutively paid their dividend for the last 15 years on these preferred shares, which is since their inception.

Bank of America Preferred Stock on seekingalpha.com

Wells Fargo Preferred Stock on seekingalpha.com

Cumulative Preferred Stock Examples

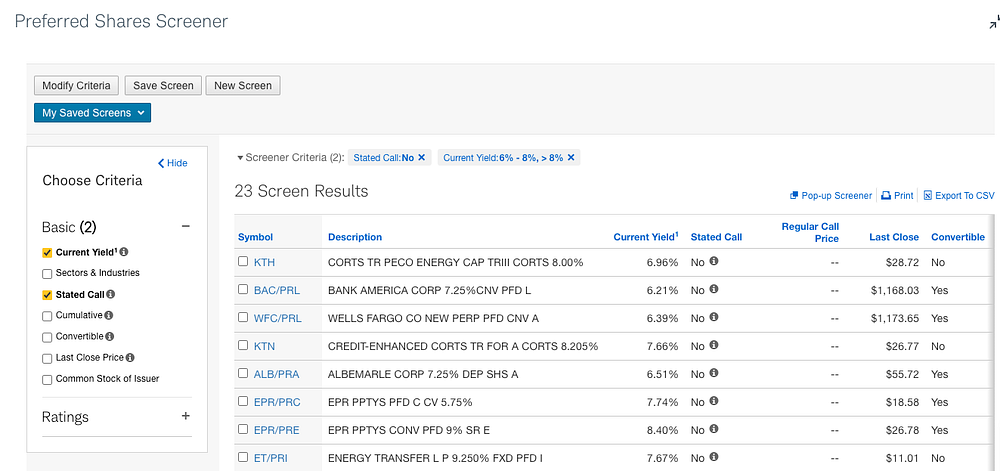

The other two preferred stocks that I want to show you are cumulative.

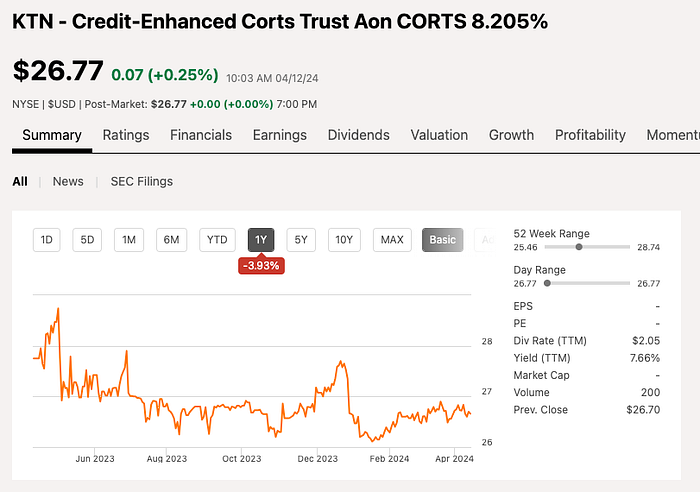

The first one is KTN. This is the preferred stock for AON PLC.

KTN on seekingalpha.com

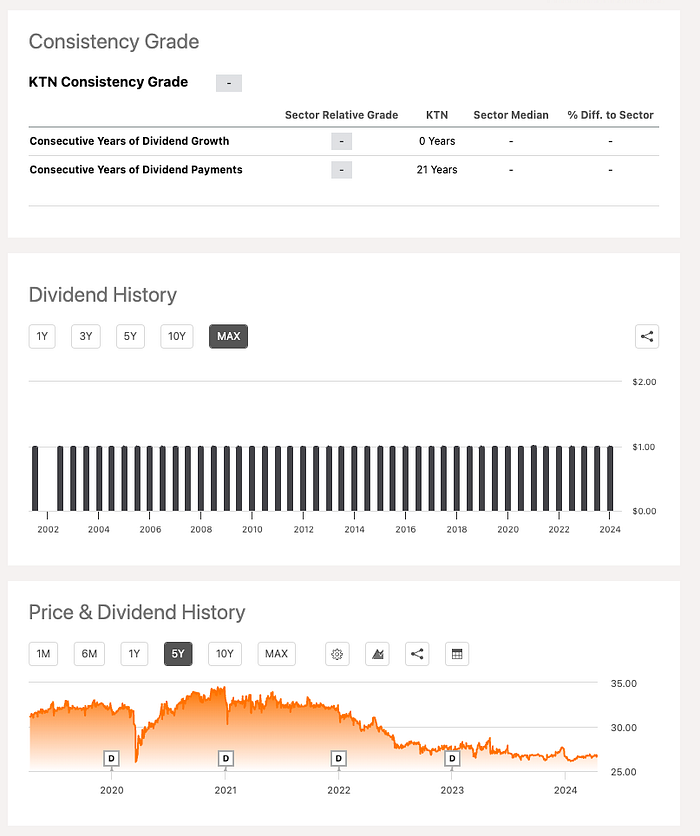

AON is an insurance broker based in Ireland and the preferred stock currently yields a ridiculous 7.66%. KTN also has a solid track record, paying the dividend every year for the last 21 years.

KTN on seekingalpha.com

Another thing I like about this stock is that the share price is much lower than the bank stocks which we’re trading at over $1,000 per share. This preferred share is just $26.77. It is also trading at a premium like the bank stocks but the premium is historically low.

KTN on seekingalpha.com

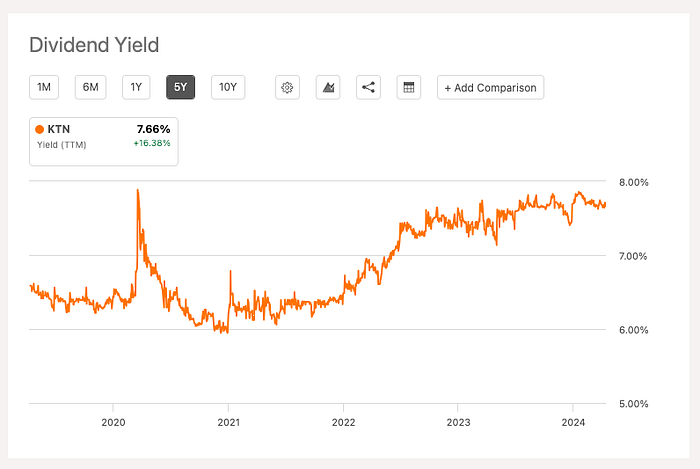

On Seeking Alpha, I can look at the historical dividend yield and we can see that it rarely extends above 7% so this stock is trading at a discount.

KTN on seekingalpha.com

Best Cumulative and High Yield Preferred Stock

The last preferred stock that I’m looking at is also cumulative and has a high dividend yield.

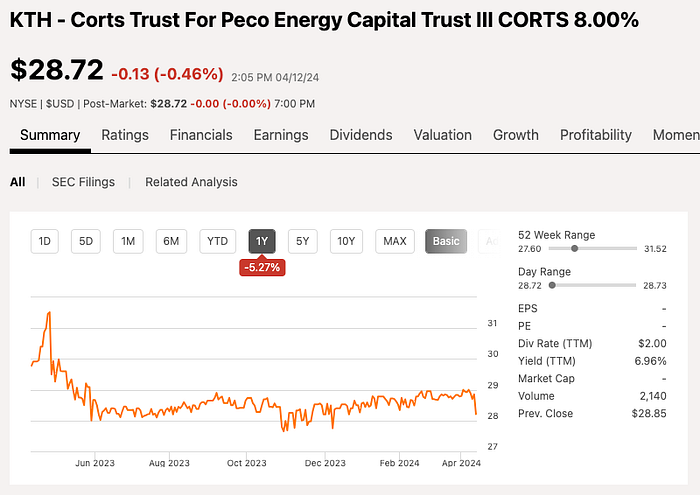

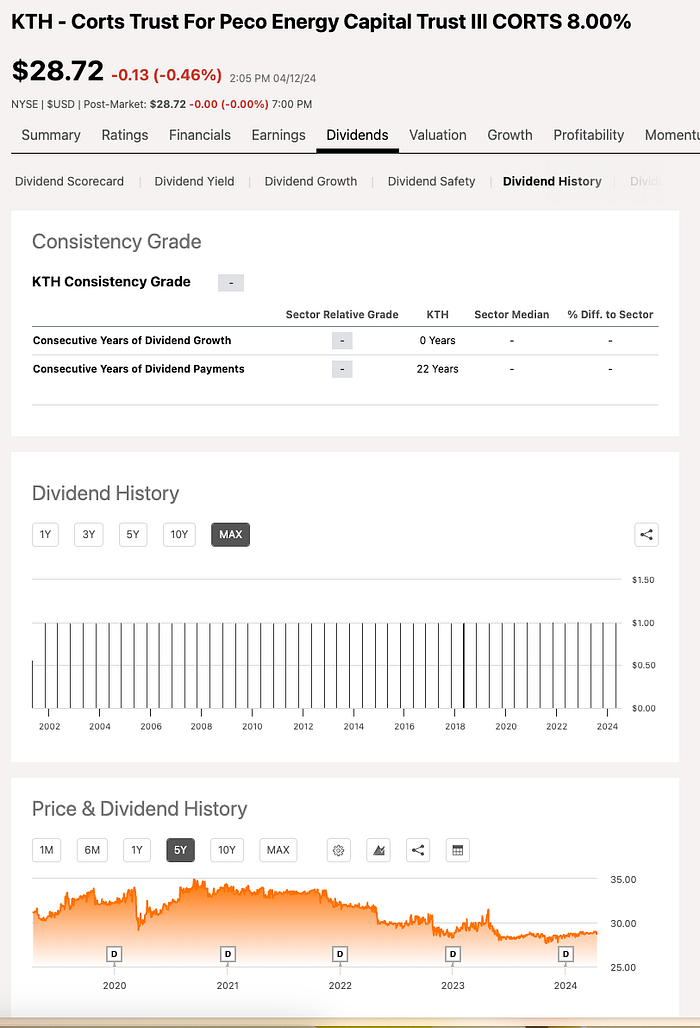

KTH is PECO Energy’s preferred stock with a current dividend yield of 6.96%.

KTH on seekingalpha.com

Just like with AON’s preferred stock, KTH is trading at a relative discount. Other than the giant middle finger in the middle of the yield graph reminding me that I missed out on a really good time to invest, you can see that the yield rarely approaches 7%.

KTH on seekingalpha.com

KTH is trading at a premium. Its current price is $28.72 or $3.72 above the face value.

KTH on seekingalpha.com

KTH may have a slightly lower yield than KTN but it does have the highest Moody credit rating out of all the preferred stocks that I have looked at so far and has been consistently paying its dividend for 22 years.

So What Now?

What I love about all of these unusual investments is the income generation and added diversity.

I tend to invest most of my extra income into common stocks and ETFs. So having access to these high income generating assets will not only boost my diversity, but also increase my returns during a market downturn.

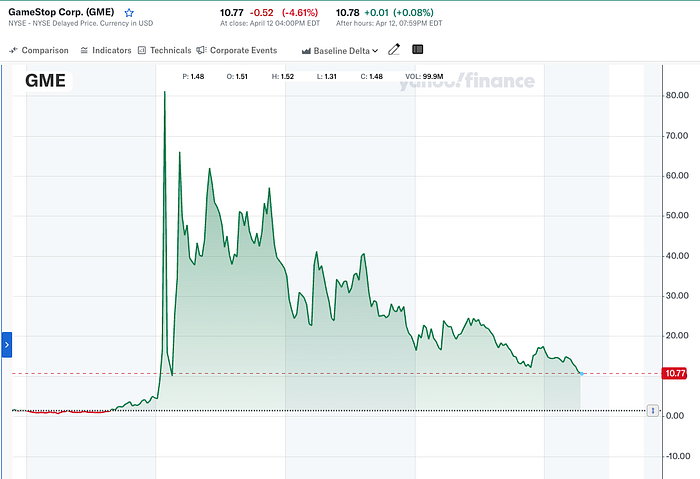

As much as I hate to admit it, the emotional aspect of investing is difficult to avoid. In 2020, when I invested in GameStop, I let my emotions get the better of me and I pulled my money out way too soon and missed out on a lot of extra gains.

GameStop (GME) on Yahoo Finance

Low risk and fixed income investments make it way easier to sleep at night when all you hear on the news is how the next market crash is right around the corner or we’re about to have World War III.

So if you prefer income generation over the ups and downs of capital gains and capital losses, then I hope you found these unusual investments valuable. Otherwise, if you enjoy buying and flipping rare collectible items, more power to you. I don’t know how you do it.

Now there is still one thing that I haven’t told you. There is one more investment that I really like that did appear on a few of these Google lists of unusual investments, and I’m doing it right now.

However, this one is not a safe income generating asset. This one is risky and it’s kind of a meme stock but for now, it is relatively unknown. I’m going to share all about my election related stock play HERE where I’m going after a 10x gain.

Catch you on the flip side.

Reply