- The Moneycessity Newsletter

- Posts

- This Is How Compounding Works

This Is How Compounding Works

Compounding is the key to turning small actions into massive results over time - and understanding why it works could change your financial future forever.

Brian Glass

December 07, 2024

Most people only learn about compounding when it’s too late.

If I started saving just $10 a day in high school, I’d have over $200K right now just from sticking to that alone. At 40, I’d have almost $0.5M. At 50, I’d have over $1M just from skipping my morning Starbucks or saving my weekly allowance in high school.

It feels like a punch in the gut to think about what I’ve missed.

Compounding is the only guaranteed way to turn a small amount of money into millions of dollars. Even Albert Einstein says that compound interest is the eighth wonder of the world, but just like the pyramids of Giza, it’s hard to appreciate them until you experience it for yourself.

I’m going to answer:

Why compounding is a powerful tool even if you’re starting with small amounts of money?

Why it’s worth the wait?

How you can start building wealth no matter what your age is or your experience level?

Watch the extended version HERE.

The Weed Analogy

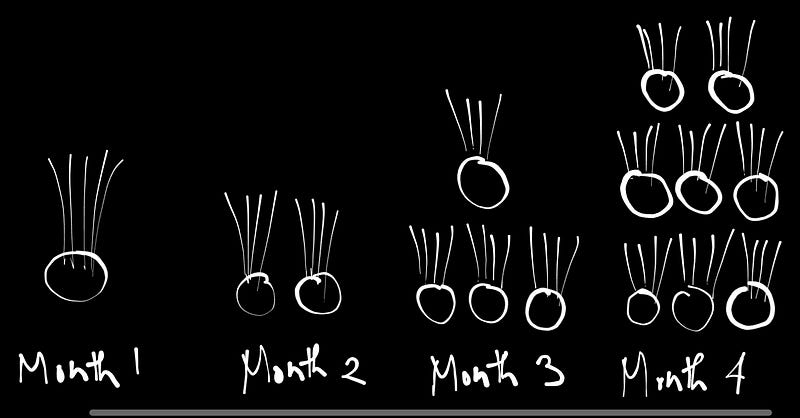

Earlier this year, I got a crash course in compounding from the most unexpected teacher: nutsedge in my backyard.

Nutsedge is a tricky weed that spreads underground through little balls called nuts. These nuts multiply, creating more nuts and sprouting even more weeds. It was summer, it was hot, and I was done dealing with it. I figured, “No big deal — if I wait a few months, I’ll just have three or four times as many weeds.”

But what I didn’t factor in was compounding.

In reality, one nut makes another nut in a month. By month two, both of those nuts are making nuts, so now there are four. By month three, there are eight, and by month four, sixteen. I didn’t have three or four times the weeds — I had 16x the weeds. That’s the dark side of compounding.

Compounding — Illustration by author

It’s exactly how credit card debt works. Leave a small balance alone, and it doubles and doubles until it’s completely overwhelming. The longer you wait, the harder it is to get rid of.

But compounding isn’t all bad. I’m tackling my nutsedge problem by planting Asian Jasmine, a ground cover that grows over time and eventually chokes out the weeds. That’s my “investing.” While the jasmine grows, I’m also staying on top of the nutsedge — pulling it out every chance I get, just like paying off debt before it spirals out of control.

Compounding is powerful, whether it’s working for you or against you. All it takes is one seed, the right conditions, and one more thing to grow into something massive.

The Power of Time

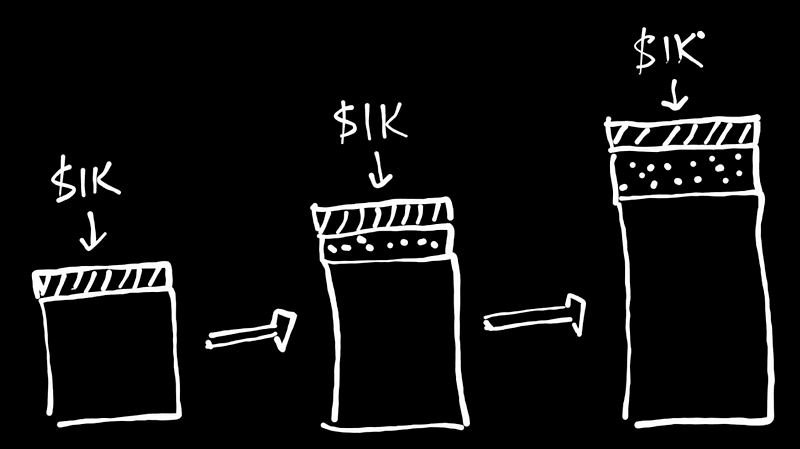

Critical mass is the tipping point in both investing and debt — where compounding takes full control.

For me, it’s like dealing with nutsedge. If I can pick 256 weeds a month, I’m fine. But once the nutsedge starts growing at 1,000 or 2,000 weeds a month, I’m overwhelmed. It’s out of my control. That’s critical mass, and no one wants to hit it with debt.

On the flip side, critical mass is exactly where you do want to be when it comes to investing. There are two big milestones for critical mass:

1st Milestone of Critical Mass — Illustration by author

My first big milestone is when the interest my portfolio earns beats how much I’m adding to it from my salary. If I’m contributing $1,000 a month to my portfolio, once compounding starts generating more than $1,000 a month on its own, things get a lot easier.

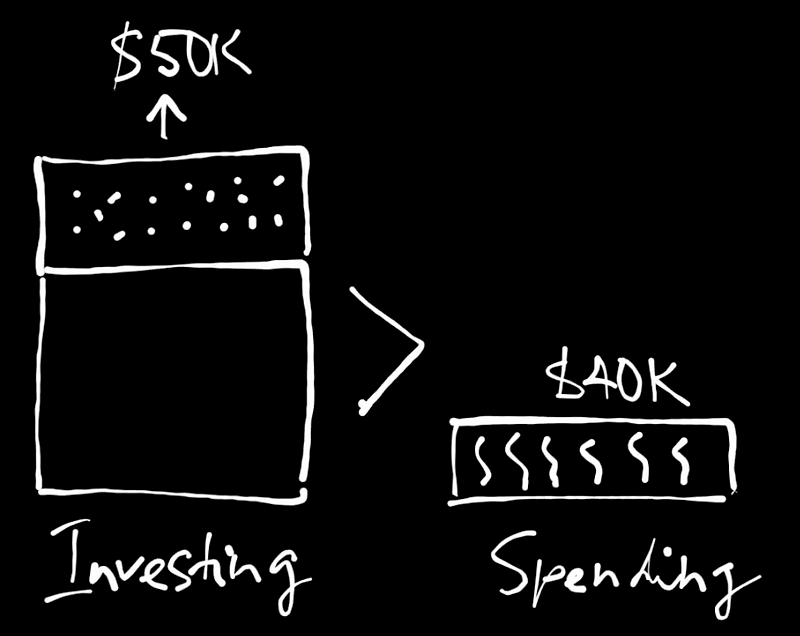

The real magic happens when compounding generates more than I can spend — the second milestone. If my portfolio earns $50,000 a year and I’m only spending $40,000, I’ve reached financial independence. From there, compounding keeps accelerating, and my wealth grows faster than I can spend it.

2nd Milestone of Critical Mass — Illustration by author

The key ingredient to all of this is time. No matter how much money you invest, time is non-negotiable for reaching that first milestone where compounding really kicks in. It might take years, but once it happens, the process speeds up.

So, what if you didn’t start investing in high school? I didn’t either. Is it too late to take advantage of compounding? Not at all. There’s another variable in the compounding equation, and it can make all the difference.

The Magic of Consistency

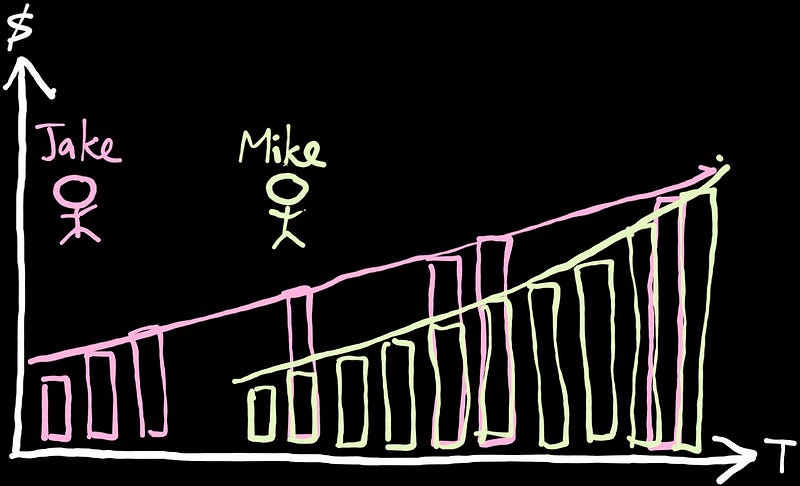

There are two types of investors: Mike and Jake.

Jake started young — his parents made him invest his allowance in high school. He got a great head start, but by college, investing wasn’t on his radar anymore. He was more focused on enjoying life — going out, upgrading his lifestyle, and putting off investing. When he did invest, it was inconsistent. One year he’d put money in; the next, he’d skip because he wanted a nicer car or a better apartment. He never stuck to a plan or increased his investments as he earned more.

Mike, on the other hand, started much later at 30. He regretted not investing earlier, so he committed to fixing it. He put $1,000 into his investments every month without fail. And as he earned raises, he increased that amount to keep up with inflation.

Time VS Consistency — Illustration by author

With this discipline, Mike is set to hit $1 million by age 50. Meanwhile, Jake, despite his early start, won’t reach the same milestone because he wasn’t consistent.

Starting early is powerful — it gives you a huge advantage. But without consistency, time alone won’t get you to financial independence.

Financial independence is about the freedom to live on your terms, not hoarding money. If financial independence is important to you, check out this video HERE.

Cheers!

Reply