- The Moneycessity Newsletter

- Posts

- 5 Things To Avoid If You Want To Be Rich

5 Things To Avoid If You Want To Be Rich

Understanding wealth creation is more nuanced than mimicking the lifestyle of the wealthy. We will explore five major wealth traps that can hinder financial growth. We delve into the importance of compounding, diversifying investments, and continuous personal and professional growth.

Brian Glass

July 23, 2024

The path to wealth is not the same as the path of the wealthy. Rich people buy expensive cars, expensive houses, and expensive things.

And don’t get me wrong. Someday, I’m going to want some of those things but those are not the actions that optimize wealth creation.

If I take the wrong step or build the wrong habit early in life, it could set me back years or decades.

I did not want to fall into one of these wealth traps, so I consulted the greatest investors, philosophers, and a little bit of my own experience, and did the math on the first wealth trap which is buying a house too early.

On the go? Watch the video HERE.

5 Things to Avoid if You Want to Be Rich

1. Buying a House Too Early

There are three major costs to buying a house too early.

First, opportunity costs.

When I put that lump sum into the down payment, the closing costs, and furnishing the house, I am leaving returns on the table.

Second, I now have concentration risk.

I have the bulk of my life savings in one sector, in one location, one neighborhood not even one country. It’s in one neighborhood. If a building goes up nearby or the school district starts to get worse, then all of my investment is going to lose value.

I’m not diversified at all when I have a big chunk of my life savings in my house. If my house loses value, suddenly I’m now trapped in that house as well.

The third major problem in buying a house too early is reducing my mobility and opportunity prospects.

If my wife or I gets a huge job opportunity that requires us to relocate, owning a house makes that much more difficult.

Cost of Rent vs Mortgage

The majority of the costs in homeownership are in the closing costs when you buy and when you sell. If I have to do those two actions in too short of succession, then I’m losing money big time on my house.

And this also plays into the concentration risk. If my school district shits the bed and I lose a ton of value on my house, I might have to pay the bank just to sell my house. And if I don’t have the money, then I’m stuck.

For instance, if I have a $300,000 loan from the bank and suddenly I can only sell my home for $200,000, if I can’t come up with $100,000 dollars, I’m not moving.

So that is an extreme case. But the moral of the story is if I can’t be light on my feet, then buying a house too early could cost me big and this also leads into the next big wealth trap which is complacency.

2. Complacency

The power of compounding is absolutely necessary to build wealth and it doesn’t just apply to compounding my money. It also applies to compounding my skills and my marketability.

Being stagnant in my career and not growing my skills would absolutely kill my chances at building wealth.

One of the three great stoic philosophers, Epictetus, says:

“The trials you encounter will introduce you to your strengths.” — Epictetus

This is a great reminder that I must continue to challenge myself. If I become soft, then I am cheating myself out of finding my greatest strengths through challenge.

And utilizing my greatest strengths will be absolutely necessary if I’m going to build real wealth.

If I’m not pushed by challenge to innovate and to change and adapt, then I will be complacent.

One of the other great Stoic philosophers, Marcus Aurelius, says:

“Is any man afraid of change? What can take place without change? What then is more pleasing or more suitable to the universal nature? And can you take a hot bath unless the wood for the fire undergoes a change? And can you be nourished unless the food undergoes a change? And can anything else that is useful be accomplished without change? Do you not see then that for yourself also to change is just the same, and equally necessary for the universal nature?” — Marcus Aurelius

One thing that makes it much easier for me to continue to push myself and challenge myself is that the people around me and the people I work with are doing that every day.

If I was surrounded by the wrong people, people who were dragging me down, who were not pushing themselves and who were complacent, I would be tempted to do the same thing.

3. Surrounding Yourself With the Wrong People

The third major wealth trap is surrounding yourself with the wrong people.

You may have heard the phrase that you become the average of the people you spend the most time with and I don’t think that is far from the truth.

The people around me, if they’re going in the same direction that I want to be going in, then they’re going to motivate me and hold me accountable.

If I’m talking to my closest friends about what my goals are and my aspirations, they’re going to know if I’m not accomplishing those goals and they’re going to hold me accountable.

Peer pressure into healthy habits can happen just like peer pressure into unhealthy habits.

If you’ve ever seen crabs in a bucket, then you are aware of the crab mentality. When one crab starts to ascend and climb out of the bucket, the other crabs will pinch on and pull them back down into place.

Whether it is conscious or subconscious, people in a group want to be on the same level.

If one person starts to ascend past their peers, the others may drag them back down onto their level. If I can continue to push myself to challenge myself, build new strengths, and continue to surround myself with the right group of people, then I will make money.

The next question is, what do I do with that money?

4. Putting All Your Money in a Savings Account

The fourth major wealth trap is putting my money in a savings account and not investing it.

Not investing my money will halt me on my path to wealth in three different ways.

First, inflation.

A high yield savings account will not keep pace with the rising cost of living. If I am losing my spending power at a faster rate than I am gaining money in my savings account, then I’m not even treading water.

Second, I’m missing out on the compounding growth of the market.

Compounding is absolutely crucial to building wealth.

Jack Bogle points out that your money would double every 10 years at a 7% interest rate, but that’s not even the average stock market returns.

The S&P 500 returns on average 10% per year which would double your money every 7 years. If you want access to this increase in wealth, you’re going to have to invest in the stock market.

Increased returns are not the only benefit of investing in the stock market.

The third problem with a savings account is taxes.

Every year that I get interest in a savings account, I have to pay taxes on those gains. Whereas if I buy securities in the stock market, I can delay those taxes until I sell the security.

I can compound my wealth over time without being slowed down by paying taxes on that growth every single year.

The only thing that would stop me from taking advantage of the power of compounding in the stock market would be the fifth major wealth trap, spending excessively.

5. Spending Excessively

Unfortunately, compounding works against me just like it works for me.

Whenever I spend too much money on a good or service, I am not only losing that cash. I’m also losing the opportunity cost of investing in the stock market.

Spending excessively does not just cost me the dollars today, it also brings an opportunity cost. I’m not getting to enjoy the power of compounding on that money.

For instance, if I spend an extra $10,000 on a vehicle that I didn’t need to, in 20 years, that’s going to cost me $67,275. Because in the stock market with a 10% return, that money is going to double every 7 years.

And if I buy a car, it’s costing me money in two other ways.

A car is a depreciating asset.

So if I spent $20,000 on the car, I’m not going to get to sell it at the end for $20,000. I’m going to lose more money there. And if I had to have a loan to pay for that car, then I’m losing money on the interest rate as well.

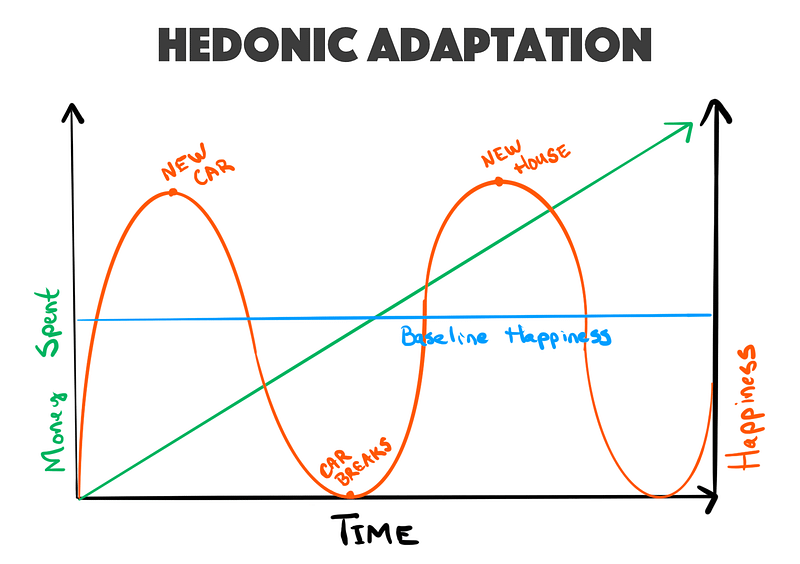

And the worst part is, the more luxuriously I spend, it doesn’t even increase my happiness because of the principle of hedonic adaptation.

Hedonic Adaptation Explained

Humans return to their baseline level of happiness after they’re in a scenario after they’re in a situation for enough time.

This works for both the negative. If you’re suffering, you’ll eventually return to a base level of happiness.

It also works if you’re spending luxuriously on the positive end. If I’m spending $100,000 a year, eventually I’m going to return to my baseline happiness. I’m going to feel the same as when I was spending $50,000 per year.

So falling into the spiral of hedonic adaptation is one wealth trap that I absolutely want to avoid because happiness is what I’m after and wealth It’s just the tool that I’m using to get there.

So What Now?

And this is the real problem because many people find themselves with real wealth and they are still unhappy.

There are miserable millionaires out there. And this fact makes me uneasy because I’m on the quest to build wealth, and maybe I’m doing something wrong along the way that is setting me up for failure.

So to find out, I decided to compile the stories on Reddit of people who got rich, retired, and regretted it.

Check out this video HERE to see the common threads and the lessons I learned.

Catch you on the flip side.

Reply