- The Moneycessity Newsletter

- Posts

- 99% of Investors Are Wrong About TESLA

99% of Investors Are Wrong About TESLA

Tesla is perhaps the hottest stock on the market and always the center of attention. But, is Tesla a good investment? I use the discounted free cash flow model to determine a fair price for 11th largest company in the world.

Brian Glass

August 24, 2024

Right now is NOT a good time to buy Tesla stock, stick around if you want to know why.

On the go? Watch my video HERE.

99% of Investors Are Wrong About TESLA

My Method

For this analysis, I am using the discounted future free cash flow model based on analyst predictions for future growth and I am laying out what kind of growth Tesla actually needs to justify the current share price today.

I love using this model because it’s very easy to understand and it’s very intuitive. Free cash flow is the money that a company uses to pay off its debt, reinvest in future growth, pay out dividends, and/or perform share buybacks. Basically, the free cash flow is my return on investment.

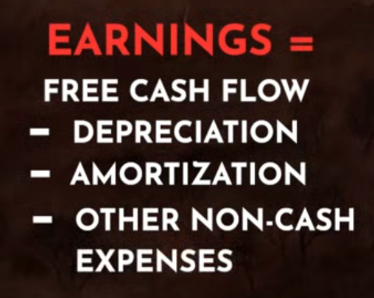

I don’t care about the earnings per share as much as I care about the free cash flow per share.

This is because the earnings will be reduced by depreciation, amortization, and other non-cash expenses. Free cash flow better represents the amount of cash that a company actually has to return value to shareholders.

I want to know how much free cash flow a company is generating right now and how much it expects to grow that free cash flow in the future.

Let’s look at their annual report.

The Business Side of Things

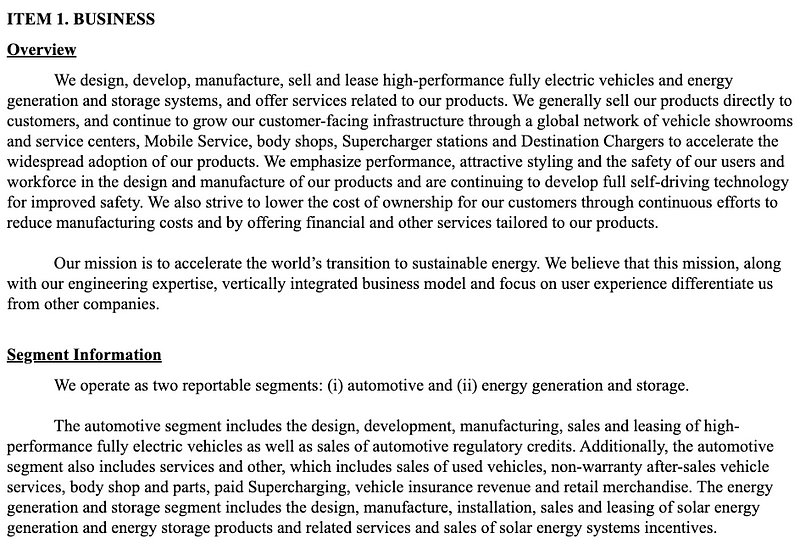

Tesla has two major segments where they offer products and services:

Automotive

Energy generation and storage

Automotive

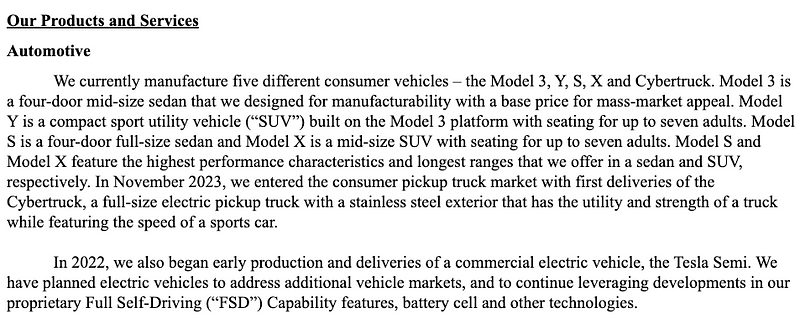

Looking at their products and the automotive segment, they have their model 3, model Y, S, and X. Recently Tesla came out with their Cybertruck. And of course, the Tesla Semi is imminent.

The Tesla Semi is the one that I am most excited about going forward because I think it has the most potential for growth. Tesla has already cornered the market and done really well with their Model 3 and Model Y. But, I think competition is going to start to eat into those revenues.

Energy Generation and Storage

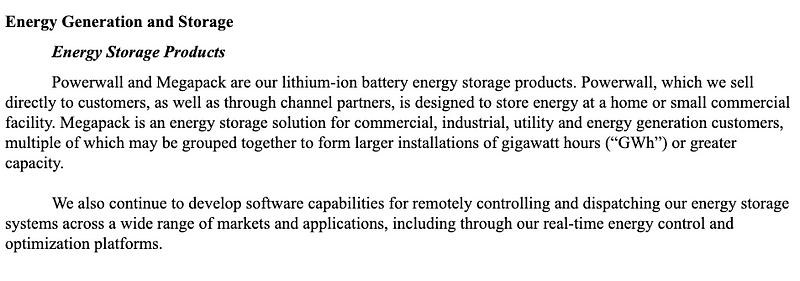

In the Tesal energy segment, they’ve got their power wall and mega pack energy storage. For energy generation, the solar roof is what I’m most excited about. Forget about putting solar panels on an existing roof. Tesla is combining the two systems. The shingles will be the solar panels.

However, products aren’t the only thing that Tesla has going on. They also have really exciting technologies.

The Technology Side of Things

Automotive

In the automotive segment, they have a proprietary powertrain and lithium-ion battery, and they have an improved manufacturing process all proprietary, so that gives them a leg up over their competition.

Tesla is developing self-driving AI, which is the most exciting part about the automotive branch where they use vision-based tech. Tesla has access to tons of field data which they can leverage to one day produce autonomous Tesla ride-hailing and robotics.

These are the kinds of things that they’re looking to expand into in the future. I think that is very exciting. Being able to have your Tesla go out do ride share without you having to drive is awesome.

Energy Generation and Storage

In the energy generation and storage segment, they have modular battery systems, software, and a solar roof that integrates with their power wall.

Another opportunity that Tesla has for revenue growth is public charging. Tesla has now made their supercharging stations available to other car manufacturers. With their current headstart in charging infrastructure, Tesla is poised to capitalize on EVs from other manufacturers.

The Other Thing

Tesla is also offering insurance and continues to benefit from the automotive regulatory credits.

This is where other car companies are required to purchase these regulatory credits from Tesla if they are not producing green energy products like Tesla is.

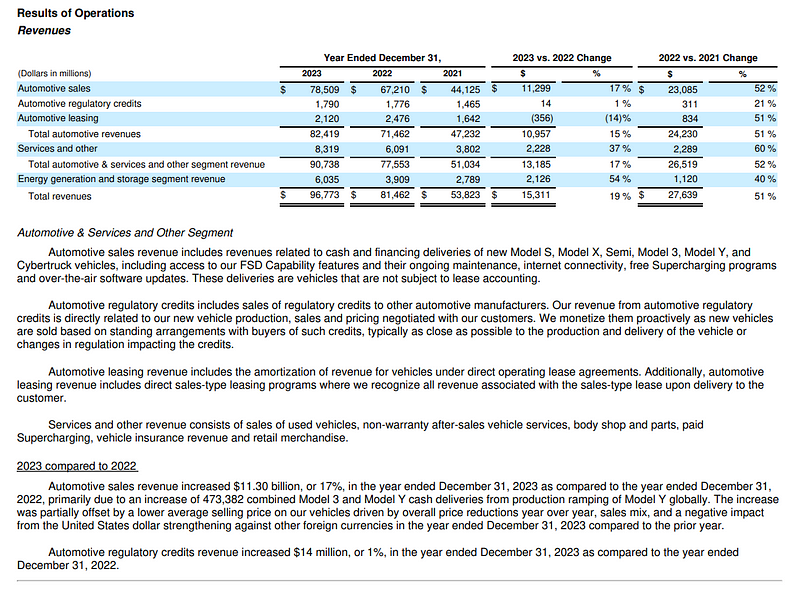

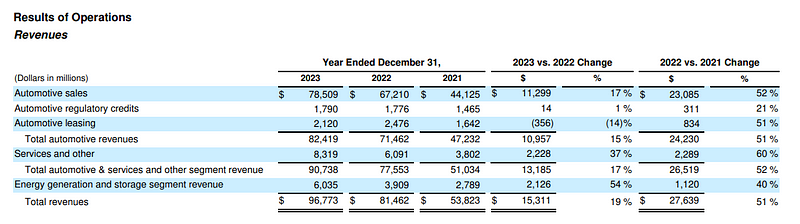

The Revenue Breakdown

Automotive Rev

All of the sources of revenue mentioned in Tesla’s annual report sound good in theory, but let’s see how Tesla is performing over the last few years.

If we look at their revenue breakdown, automotive sales have increased by 17% from 2022 to 2023.

Unfortunately, Tesla does not include a breakdown of their Semi revenue specifically. Tesla does specify that most of the revenue increase is primarily due to the combined sale of the Model 3 and the Model Y and cash deliveries from production ramping for Model Y globally.

Tesla is suffering from reduced margins due to a lower average selling price. This was slightly offset by a decrease in cost per unit. This trend will only get worse as more manufacturers bring EVs to the market.

Services & Other

The next big revenue breakdown is “Services and other” where they have used vehicles, vehicle services, body shop and parts, paid supercharging, vehicle insurance revenue, and retail merchandise. This segment grew 37% from 2022 to 2023.

However, they have had a margin decrease in this segment as well, and that’s due to the same issues discussed in the previous section.

Energy Generation & Storage

Finally, Tesla’s energy generation and storage experienced a 54% revenue increase from 2022 to 2023. That’s really exciting.

Tesla’s total growth in revenue is 19%. $78.5 billion of their revenue, which is the vast majority, is coming from their automotive sales.

Nothing is Perfect

Even though Tesla has achieved strong revenue growth, it has substantial risks going forward.

Competition

First of all, competition. Tesla’s margins are getting eaten away because they’re having to sell their vehicles for a lower and lower price.

It’s only a matter of time. Electric vehicles are getting more and more popular both in the US and internationally so competition is eating away at Tesla’s US markets, Chinese market, and the European markets.

The regulatory credits are also at risk when we’re talking about competition. If more and more car manufacturers are coming out with EVs, then they’re going to be less reliant on Tesla for the regulatory credits, thus eating into another revenue stream for Tesla.

And finally, with AI, Tesla is not going to be the only company that is going hard on self-driving vehicles.

NVIDIA has recently declared in its annual report that they’re going to start going after the autonomous vehicle segment.

Leadership

The next big risk factor that I see is Elon Musk himself. He’s not fully focused on Tesla.

We saw with the recent CEO pay debacle where Elon Musk is getting paid $55 billion from Tesla and one of his big reasons for wanting this big paycheck is to go after landing a human on Mars. He is pulling money and attention out of Tesla.

In Tesla’s annual report to shareholders, they have a rick section:

“We are highly dependent on the services of Elon Musk, Techno King of Tesla and our chief executive officer.”

How I Calculate Intrinsic Value

So now that we’ve built a narrative for ourselves by looking at the annual report, the next step is to determine the kind of growth required for Tesla to justify their current share price.

And for this, I like to look at my discounted future free cashflow model. I come up with 5 different estimations for the intrinsic value of Tesla with my discounted free cash flow spreadsheet.

Three of the estimations utilize analyst projections for future revenue. My resource for analyst projections is StockAnalysis.com.

The fourth projection uses the past 5 years of revenue to extrapolate future revenue.

The fifth projection is used to attack the problem from the other side. I will use the current share price to determine what the implied revenue and free cash flow margin growth are.

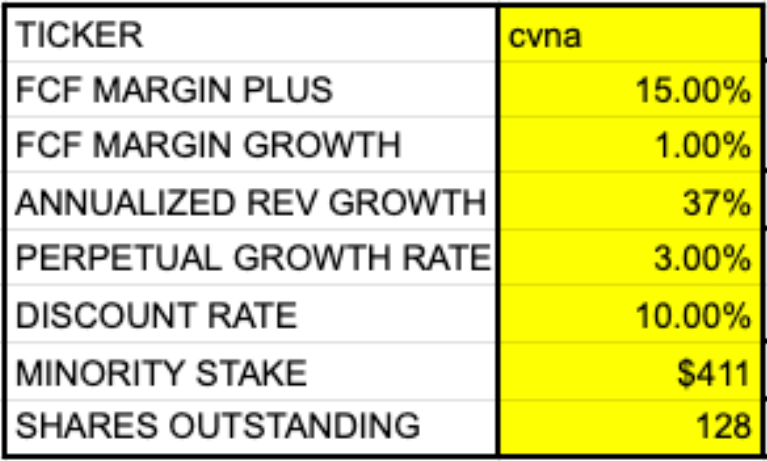

The sections in yellow are the assumptions that I have to make.

Ticker

For the first cell, I type in the ticker and my spreadsheet will automatically scrape the web and fill out all of the financial information for Tesla as well as the analyst predictions.

This took me a long time to put together but the hard work pays off.

Free Cash Flow Margin Plus & Growth

The FCF Margin Plus and FCF Margin Growth allow me to tweak the projected free cash flow that I derived from the analyst predictions.

My spreadsheet will automatically take the average free cash flow margin over the last 5 years and multiply that by the analyst projections for future revenue growth to determine an initial free cash flow projection.

Annualized Revenue Growth

The Annualized Revenue Growth cell is where I determine what rate of growth will justify the current share price.

Perpetual Growth Rate

The perpetual growth rate is the rate at which I’m projecting Tesla is going to grow into infinity after the 5-year prediction.

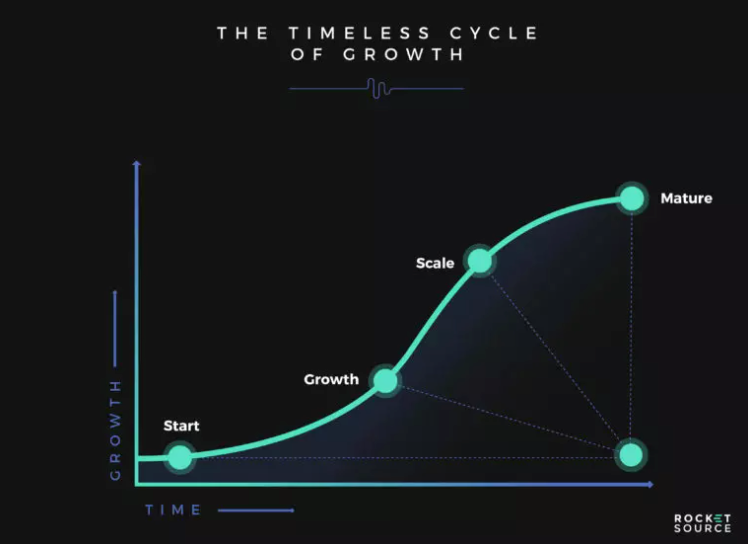

The typical growth curve of a company looks like an S curve.

The typical growth curve of a company

In the beginning, growth is very slow. After a company proves its business model and popularity starts to rise, it has entered the growth phase. The company will then continue to scale and eat up as much market share as possible. Finally, when the company becomes mature and the growth levels off, this is where the perpetual growth rate comes into play.

The perpetual growth rate will resemble inflation — the growth of the economy. No company can grow faster than the economy forever because it would eventually dwarf the entire economy.

Discount Rate

The final assumption is the discount rate.

I like to use a company's Cost of Equity for this rate. The discount rate represents the return a company must offer investors to compensate for the risk of investing in the stock. That is also taking into account the inherent risk of investing in that company versus the market’s overall risk.

The last information that I must manually enter into my spreadsheet is the minority stake and the shares outstanding in millions.

I will eventually adjust my spreadsheet to scrape this information automatically as well. Both of these are available on a company's financial documents.

Current State

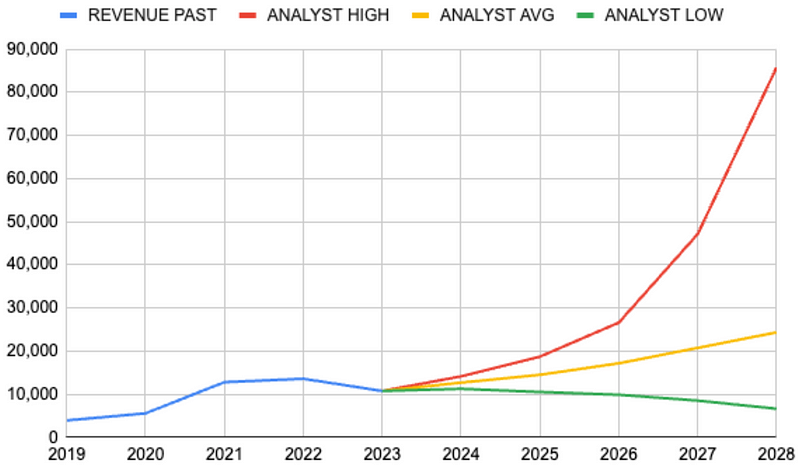

The first graph shows the high analyst prediction in red, the average in yellow, and the low in green.

With Tesla, there is a huge spread with the high analyst prediction. We’re looking at nearly a 6X increase in revenue over the next 5 years for the highest projection.

If we search companies ranked by market cap, Tesla is already the 11th biggest company in the world. Are they really going to be able to 6X their revenue over the next 5 years?

Even with insane growth over the next 5 years coupled with an average FCF Margin of 6.18%, the analyst's high prediction only results in a $142 intrinsic value for Tesla while Tesla’s current share price on the day I’m making this article is $240.

Even at this insane growth trajectory, Tesla is still overpriced using the discounted future free cash flow model.

What If We Get Lucky?

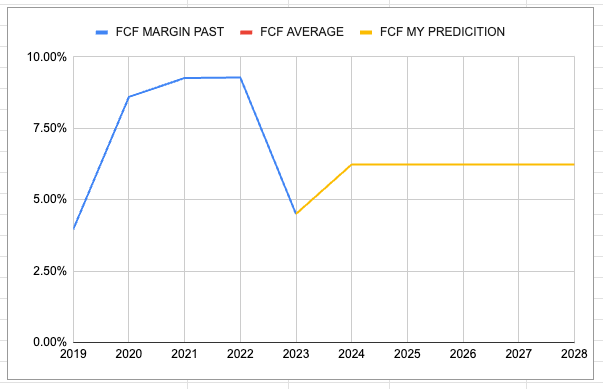

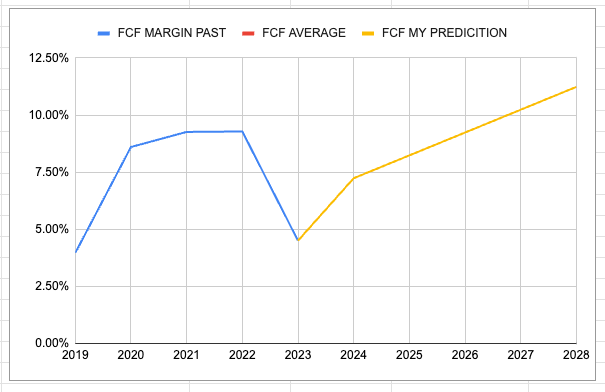

One thing we can tweak is we can increase their free cash flow margin. So right now I’ve got Tesla’s free cashflow margin going into the future at their average over the past 5 years, which is 6.18%.

If I enter “1%” in the “FCF Margin Growth” cell, then my spreadsheet will calculate a new intrinsic value based on the following FCF graph and high analyst prediction. The resulting intrinsic value is $250.

So this is the growth scenario that Tesla needs in order to make today’s share price worth it.

They need an annualized growth of 43% every year for the next 5 years and then 3% per year after that. And then they need to become increasingly more profitable with an increasing free cashflow margin.

In my mind, this is just not a likely scenario.

More Likely Scenario

If Tesla was to grow at a more modest pace of 15% per year, then that would put their share price at $91 per share.

Even if they were able to continue their past growth, which has been an explosive 31.5% — putting them at the 11th biggest company in the world, that just puts Tesla’s fair share price at $167 per share.

Remember that S curve? Is Tesla really going to keep scaling to that extent over the next 5 years? I find that doubtful.

The typical growth curve of a company

With all this in mind, Tesla has a lot of exciting things on the horizon and lots of really cool opportunities for revenue growth. I am most excited to see the development of Tesla’s Semi, self-driving AI, and Solar Roof.

However, all of that has to go perfectly.

Tesla has to have insane revenue growth and insane free cash flow growth to justify their current share price.

So What Now?

For me, I’m going to wait.

I’m not going to buy Tesla at today’s share price. I’m going to wait for this company to come down a bit. And then maybe if I have a bigger margin of safety, I would be excited to jump into Tesla as an investment.

Just not today.

Earlier I mentioned that NVIDIA is jumping into the autonomous vehicle market. If you’re curious to see if NVIDIA is a good investment, I already made a video and wrote an article analyzing their intrinsic value using the discounted future free cash flow model.

Catch you on the flip side.

Reply