- The Moneycessity Newsletter

- Posts

- Why Buying a House is the WORST Investment of My Life

Why Buying a House is the WORST Investment of My Life

You’ve heard it before: “Renting is throwing money away’’ but is buying really better than renting? Today we’re going to do the math taking into account opportunity cost. I will compare the cost between owning and renting taking into account the down payment, closing costs, mortgage payments, maintenance, tax, and insurance for buying a home in Texas.

Brian Glass

February 26, 2024

How many times have you heard the phrase “Paying rent is like throwing away your money. You’ve got to buy a house”?

Well, I’m sick of hearing it.

So I’m going to destroy this saying right now by showing you how the cost of homeownership compares to the cost of renting an apartment and investing the difference dollar for dollar.

If you’re thinking about buying your first home as your primary residence solely because you think it’ll be a good investment or you’ve been hearing that you’re throwing away money on rent, then stop what you’re doing because buying a home will be the worst investment of your life.

On the go? Watch the video HERE.

Why Buying a House is the WORST Investment of My Life

Keep in mind, this goes out to the people who do not need a house for the space. If you’re married with four kids and ten cats, then you might need a house.

The key takeaway here is that buying a house is a lifestyle decision, not an investing decision.

You guys have been saying in the comments how much you love my spreadsheets, so I’ve got a good one for you today, this time with graphs.

How Much Upfront Cost to Buy VS Rent?

The first bad thing that happens when you’re trying to buy a home is you need to save a significant sum of money. You got to have enough for the down payment, closing costs, and furnishing your new home.

I live in Texas so all the numbers I’m throwing at you are going to be Texas averages so that we can compare everything apples to apples.

Buying

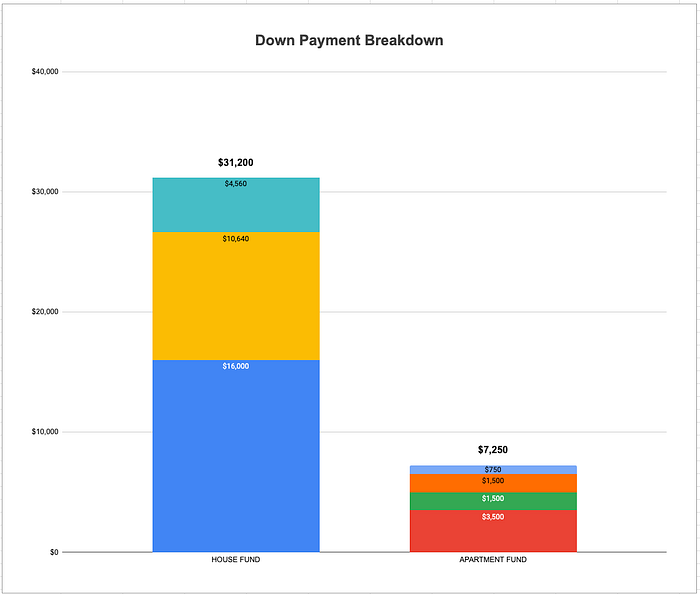

The average Texas home is worth about $304,000.

Typically first time home buyers are looking to put as little down as possible. I know I was. It is difficult to save 20% for a down payment. So we’re going to go with the minimum allowable down payment for most conventional loans, which is 3.5%. This comes out to just under 11k for a $304,000 home.

The average closing cost for a buyer in Texas is about 1.5%. This comes out to about $4,500. This means you need to save about $31,000 before you can even think about buying a home.

Buying a House VS Renting an Apartment visualization by author

Now, if you’re going to rent an apartment on the other hand, you still have to save up a small sum of money.

Renting

The average rent in Texas for a 2-bedroom apartment is about $1,200. In my experience, this just seems a little low to me, so I’m going to bump it up to $1,500 per month for this comparison.

In order to get a new apartment, you typically have to save up first month, last month’s rent, and a security deposit. In total, for this average Texas apartment, you’ll need about $7,250 in the bank.

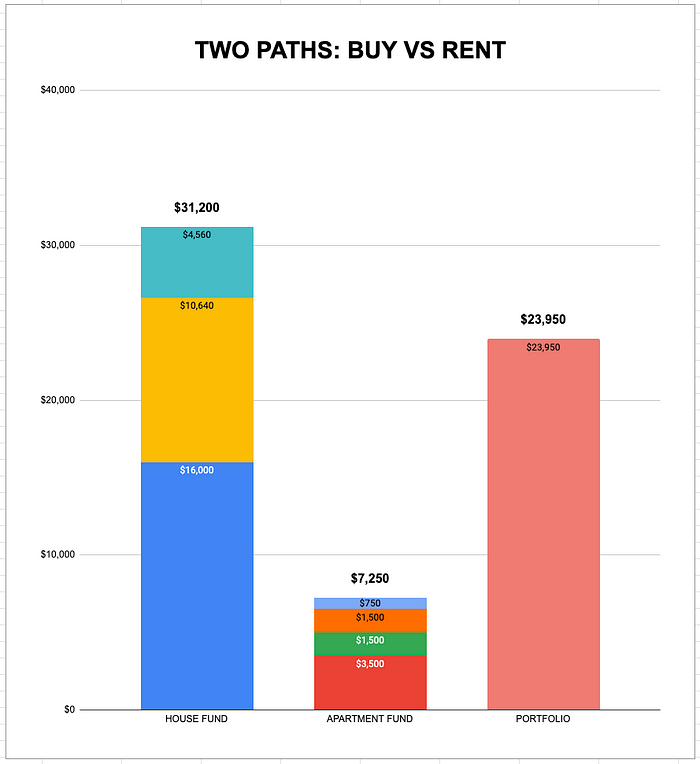

So if this is your situation, you’ve saved up $31,200 and you’re trying to make the choice between:

Do I want to go with the home route? You can put all that money into getting into a house.

Do I want to go with the apartment route? You can put some of it up to get an apartment, and you can put the rest in your stock portfolio.

Buying a House VS Renting an Apartment visualization by author

For this comparison, we’re going to assume that all investments in your stock portfolio, are in an S&P 500 index fund, which averages about 10% per year.

On the other hand, your house will appreciate, on average, about 4.7% per year. Obviously, some years will be much higher than others, but over the long term, this is what you’re going to be looking at.

Upfront Cost Comparison between Buying VS Sharing

So let’s put both paths at square one on the left hand column. I’ve got expenses and on the right hand column I’ve got equity or portfolio value.

Expenses

When we’re talking about expenses, we’re talking about the money that you’re throwing away.

When you own a home, you will be throwing away money.

When buying a house, you can pretend like you just lit that the closing costs on fire. You’re not getting it back.

When renting, the security deposit, you might get it back, but we’re going to include the first month, the last month, and the security deposit as expenses for now.

Equity

The down payment doesn’t count as throwing away money and the cost of furnishing doesn’t count because both of those things are being utilized.

The down payment goes into the principle of your home.

The furniture will count as an asset because you will get to keep the furniture when you move or sell it on Facebook Marketplace.

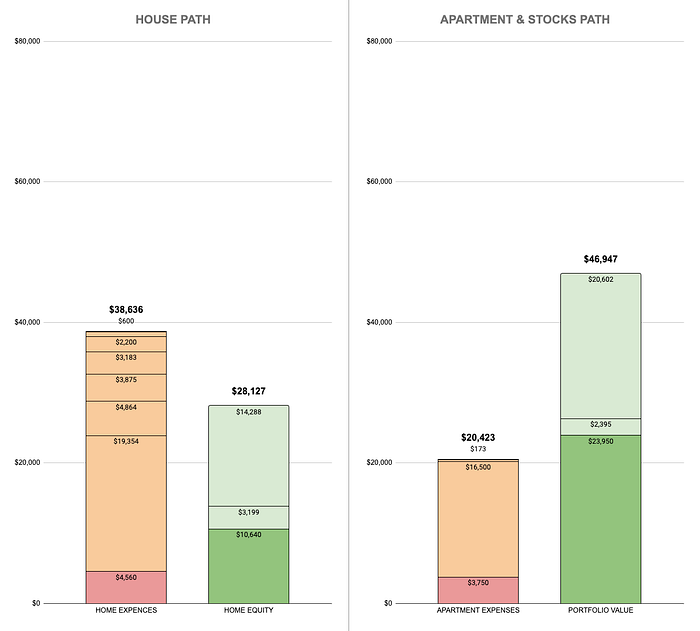

As you can see at square one, the house has higher expenses and lower equity while the apartment has lower expenses and higher portfolio value.

Let’s see how this changes after we look at our first full year of expenses in both categories.

At a glance you can see it’s not looking good for the homeowner. There are much more expenses than the apartment and you have much less equity.

Mortgage Payment

Before I get into the breakdown on all these costs, let’s look at how your mortgage payment is divided between fees, interest, and principal.

Mortgage Payment Explained in Taxes and Fees, Interest, Principal, and Balance

When I hover over the breakdown for the first year in mortgage payments, you can see that you are paying $11,540 in taxes and fees, $19,354 in interest, and only $3,199 in principal.

All of your mortgage payments all year, you’re only gaining $3,200 in equity. The rest of that money, your interest, your taxes, your fees.

That is analogous to the rent money that you’re throwing away when you rent an apartment. You can just light that money on fire. It’s gone.

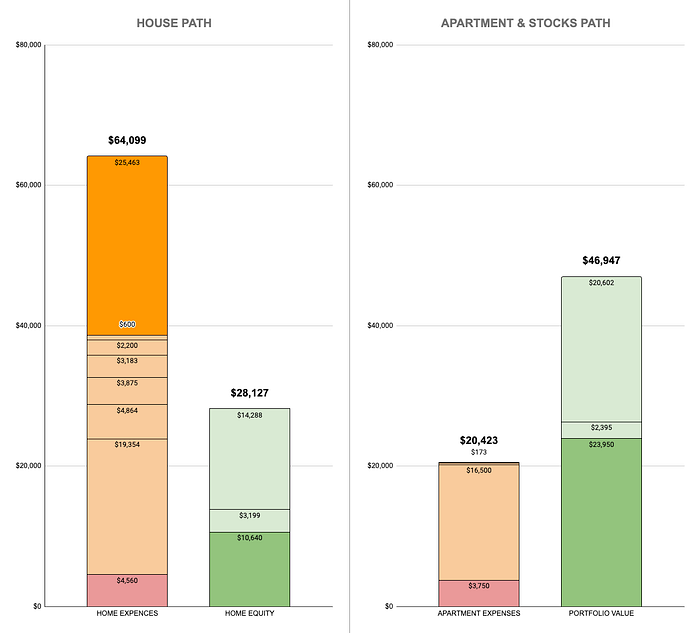

Year 1 Comparison between Buying VS Sharing

House Path

Buying a House VS Renting an Apartment visualization by author

That first chunk at the bottom is your closing costs. The second chunk, $19,000, is your interest. The third chunk is your taxes, $4,900. The fourth chunk is your home insurance, $3,875.

Then you’ve got your maintenance. For home maintenance, we’re going with the 1% rule. This means that over the long term, you’re going to average 1% of the house’s value in maintenance fees.

Now, some years you’re not going to have any maintenance. And then other years, you’re going to have a lot. You might have to replace your HVAC system. You might have to replace your roof. Your plumbing might freeze one year, and you’ve got to deal with water leaks. Over the long term, you’re going to average 1% in fees per year.

The next row is your mortgage insurance. Because we went with the lower down payment, just $3.5%, you’ve got to pay this fee until you get up to 20% equity in the house. On average, the PMI is about a 0.5% to 1% in Texas, so we’re gonna just split the difference. We’re gonna assume 0.75%. This comes out to $2,200 per year.

In the mortgage calculator, you can see in 2034, this is the last year that you have to pay the PMI. That section at the top, taxes and fees, reduces after this year. It is at this time that you have 20% in equity. That happens after 10 years of owning the house.

Mortgage Payment Explained in Taxes and Fees, Interest, Principal, and Balance

Back to the expenses breakdown.

That last little section at the top of $600 is an HOA. In Texas, the average HOA is somewhere between $100 and $200. I decided to go a little bit cheaper on this one because not everyone is going to have an HOA. I went with $50 per month coming out to $600 per year.

Our year 1 expenses for owning a house does not include the principal. The principal goes into your home equity section.

Notably, our home expenses come out to $38,636, while the expenses for our apartment only comes out to $20,423.

What are we going to do with all this difference?

We’re going to invest it.

Apartment and Stocks Path

Buying a House VS Renting an Apartment visualization by author

In our stock portfolio, you’ve probably noticed by now that the portfolio of the apartment path has grown substantially.

Remember the dark green sections of the home equity and the portfolio value is the sum that we had at the beginning of the year. And then the lighter green sections is how much we’ve added throughout the course of the year.

On the portfolio value, $2,395 was our 10% gain on that initial sum of money throughout the year. And then the $20,600 is the difference in expenses that you would have had to pay on the house versus the apartment.

So in these two paths, if you went down the housing path, you would end up with $28,127 in home equity. And then with the same amount of money, you could have ended up with $46,947 in stocks in your portfolio.

It only gets worse from here.

House Path — Selling Within the First Year

Whenever you go to sell your house, you’re going to have another huge chunk of expenses.

There are some reasons, especially for a first time home buyer, why you might be forced to sell your house in the first year or first two years.

You might have a job opportunity.

You might need to move to be close to family.

You might need to get a bigger house because you get married and want to build a family.

These are all reasons why if you jump into a house too soon and then you’re forced to make a lifestyle change down the road, you’re going to be forced to sell your house before you’re ready.

This is the final comparison for year 1.

Buying a House VS Renting an Apartment visualization by author

If you’re forced to sell that house, you’re going to get hit with this bright orange expense of $25,463. This is our closing costs as a seller. On average, the seller can expect to pay between 6% and 10% of the selling value of the house. In this case, I split the difference with 8% so when you’re looking at your home equity.

Yes, your house appreciated by $14,288, and yes, you got $3,200 in principal. But all of that gets eaten up, and then some, by the closing costs.

This is one of the biggest reasons why you really want to give pause before buying your first home. Are you really in a position in life where you know you’re not going to have to sell too soon?

Another point I haven’t brought up in this case is capital gains tax.

If you sell your house before 2 years, then you will be subject to capital gains tax between 15% to 20% in 2024. However, in this case, there were no gains because it all got eaten up by fees so I left it out of this comparison.

If you do get lucky and have a significant appreciation on your home, you’re not going to want to sell before 2 years. So on that note, let’s check out the year 2 comparison.

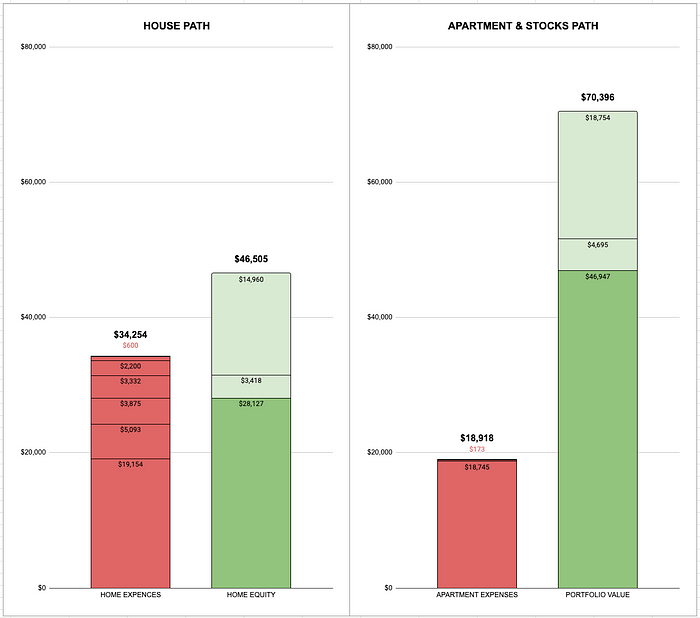

Year 2 Comparison between Buying VS Sharing

Buying a House VS Renting an Apartment visualization by author

At the beginning of the year 2 comparison, we can see where we’re starting off in this year.

We’ve got $28,127 in home equity, and we’ve got $46,947 in S&P 500 index funds in our portfolio. This is before we pay any expenses.

You might be thinking the expenses of owning a home should go down a little bit in the second year. You don’t have the closing costs after all. You would be right, but it’s still not looking very good for the homeowner.

House Path

Buying a House VS Renting an Apartment visualization by author

You can see in total, you’ve got $34,250 in home expenses. Keep in mind, this is the money that you are lighting on fire. None of this is going into the equity of your home. This is your interest. This is your fees. These are your taxes. This is your home maintenance. These are things that you’re not getting back.

On the home equity breakdown, you’ve got an additional $3,418 in principal this time. Every year, you’re going to get more money towards your principal and less money towards interest. However, it’s going to be a slow process.

The $14,960 is from home appreciation. That’s the 4.7% every year.

Apartment and Stocks Path

Meanwhile, your apartment expenses have actually gone down a bit in year 2. You don’t have to pay the additional last month of rent or an additional security deposit. You’re down to $18,918 so the expenses are lower.

And once again, your portfolio of stocks has grown more than what your home equity has grown by $4,695 due to appreciation over the whole year, and then the $18,754 is how much money you were able to afford putting into your stock portfolio because you didn’t have the added expenses of paying for your house.

Clearly after 2 years, it is more expensive to own an average home. And this is even accounting for the fact that apartments on average will increase their rents by 3.2% every year.

So you might be asking, in the long term, since your interest payment is slightly going down, is that going to be enough after 5 years or 10 years to reduce the expenses of owning a house? And maybe that cost of renting an apartment will catch up?

Let’s check out the 10 year comparison.

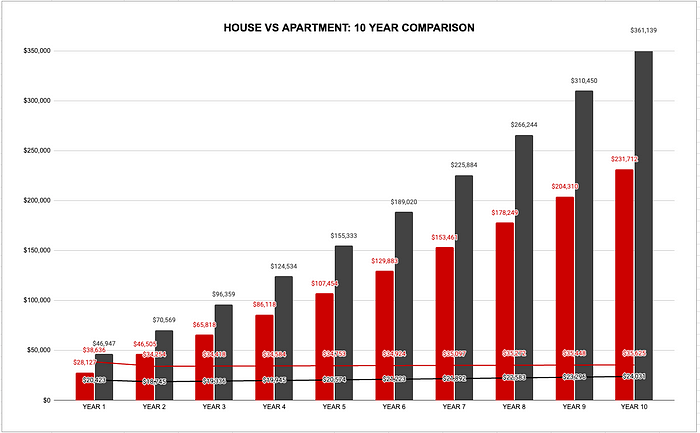

10-Year Comparison between Buying VS Sharing

Buying a House VS Renting an Apartment visualization by author

House Path

If we look at the red line, this is your housing expenses over time, you can see that the numbers are still slightly increasing.

Even though you’re chipping away at that loan, you’re paying off a little bit of principal every year, your interest rate’s going down, there are still other expenses that are going to offset it and then some.

The value of your home is appreciating every year. This increases your property taxes.

Unfortunately, inflation is a thing. The cost of maintenance is also going to go up as your house appreciates every year.

Apartment and Stocks Path

When we compare this to the black line, which is your apartment expenses over time, the price is going up slightly more than the house expenses every year because apartments are going to increase their rents about 3.2% every year.

Now this line is converging on the red housing expense line. However, in the 10-year period we’re looking at, our expenses are still going to be way higher for owning a home over renting an apartment.

On top of all that, the gap between our stock portfolio and our home equity is rising every year.

Now, what if I can find a below average house? And what if my only options in a big city are an above average apartment?

Quickly, I’m going to run through a 10 year example showing just that.

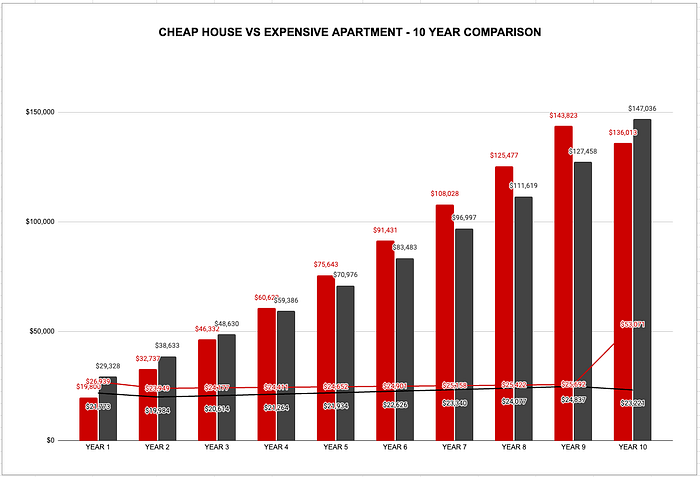

Cheap House VS Expensive Apartment

If we look at a more granular level and go by city, you can see that the average home price in Amarillo is about $214,000. While if you are comparing that to a more expensive apartment in Dallas or Austin, the average price is going to be closer to $1,600 per month.

So let’s make this comparison between the average house in Amarillo compared to the average apartment in Austin or Dallas.

Buying a House VS Renting an Apartment visualization by author

When we look at the 10 year line and bar graph:

The black bars represent your portfolio value and the red bars represent your house equity.

The black line represents your apartment costs per year and the red line represents your housing costs per year.

You can see that at year 8, the portfolio value and the home equity converge as we are actually building more home equity than you are portfolio value and the expenses are also very close.

Now, you’ve probably noticed there are some shenanigans happening at year 10. It’s because I’m showing you what happens when you sell your house at the end of 10 years.

You managed to go 9 years, you didn’t have to move to chase a better opportunity. You didn’t have to move to get a bigger house because you had kids. You didn’t have to move to be closer to family.

You went 10 years and finally at the end of that 10th year you sold, but because of the closing costs, you still lose out to just renting an apartment for 10 years.

So which team are you on?

Are you in the group of people that are renting an apartment OR are you like me and my wife, Natalie, you’re in the group of people who bought their house maybe a little prematurely?

If you’re like me, you’re probably wondering, is there a light at the end of the tunnel? Click HERE where I will be sharing 3 strategies to make MONEY from your first home.

Catch you on the flip side.

Reply