- The Moneycessity Newsletter

- Posts

- Watch This Before Buying GameStop

Watch This Before Buying GameStop

Is now a good time to invest in GameStop? I will analyze GameStop's most recent financials and business strategy to determine if it's a wise investment. Using a discounted future free cash flow model, I will evaluate the intrinsic value of GameStop stock and predict its future growth.

Brian Glass

August 17, 2024

Now that GameStop has settled down, is it now a good time to buy?

On the go? Watch my video HERE.

GameStop’s Annual Report

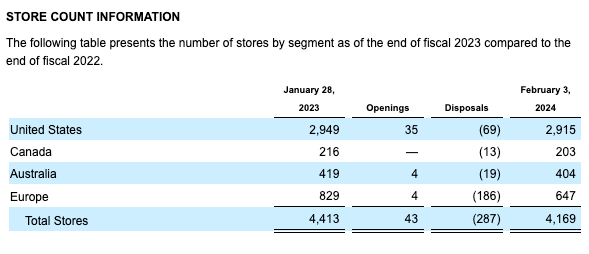

4 Geographic Segments

On GameStop’s most recent annual report, they claim four different geographic segments: the US, Canada, Australia, and Europe. Across those four segments, GameStop has 4,169 stores.

GameStop’s 2023 Annual Report

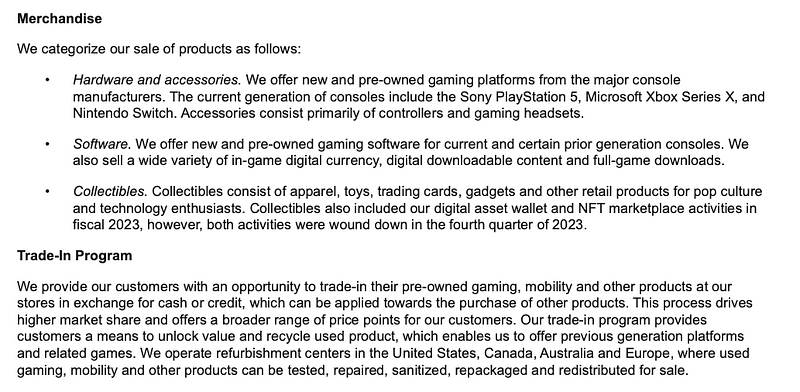

3 Types of Mech

They have three types of merchandise: hardware, software, and collectibles. GameStop sells the products brand new and has a complementary trade-in program.

Business Strategy

GameStop’s business strategy as stated on their most recent annual report shows that they have three major areas that they’re trying to improve.

First, omnichannel retail. GameStop is trying to improve its stores and e-commerce. The way technology is going, people want to buy things online. Brick and mortar is becoming increasingly outdated and it is less profitable than selling products online. As a result, GameStop plans to improve its e-commerce revenue and sales.

Increasing GameStop’s e-commerce plays into their second goal: to achieve profitability. GameStop’s sales margins have been decreasing over the last 5 years and they are trying to turn that around by containing their costs.

GameStop plans to do the above by leveraging its brand, which is the third major objective listed. GameStop is the only store that focuses solely on video games. Yes, you can buy video games and consoles at a Best Buy location. And you can also buy video games online, at Amazon. But neither store is 100% focused on video games which is an advantage that GameStop is trying to leverage.

GameStop’s 2023 Annual Report

Big Moves

Now that I know what GameStop’s plan is, I want to know what big moves GameStop has taken to achieve these three goals.

First of all, let’s look at profitability.

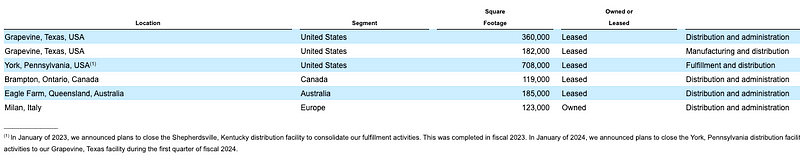

GameStop has closed two of its distribution centers. In January of 2023, they closed their Kentucky distribution center, and now in January of 2024, they have closed their Pennsylvania distribution center.

GameStop’s 2023 Annual Report

As far as their brick-and-mortar stores go, they have closed 287 locations. Between the end of fiscal year 2022 and 2023, they have only opened up 43.

GameStop’s 2023 Annual Report

In theory, Gamestop is closing their least productive stores and they’re opening stores that should perform.

So how has this played out?

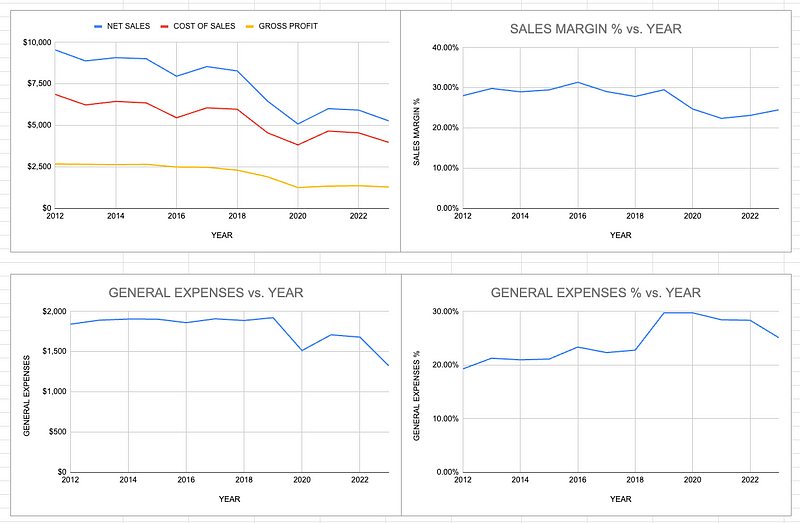

I have compiled GameStop’s financials going back to 2012. Clearly, the revenue and gross profit have been in decline.

However, I would expect to see an increasing sales margin if GameStop was truly becoming more profitable.

From 2012 to 2018, GameStop had historically a much higher sales margin. But more recently, from 2021 to 2023, they have shown a slight improvement. GameStop’s general expenses have also been trending down since 2019.

GameStop’s Financials— Spreadsheet by author

The second and probably the most important goal for GameStop is improving its e-commerce.

GameStop can cut all the costs it wants, but unless it can expand its revenue, GameStop will not return much value to shareholders.

What big steps has GameStop taken to expand its e-commerce?

Well, they have raised lots of cash.

GameStop is trying to raise $1.5 billion without revealing its e-commerce strategy

GameStop hasn’t been very upfront with how exactly they’re improving their e-commerce, but they’ve certainly raised a lot of cash to do it. Unfortunately, GameStop has done this by issuing more shares.

Risk Factors

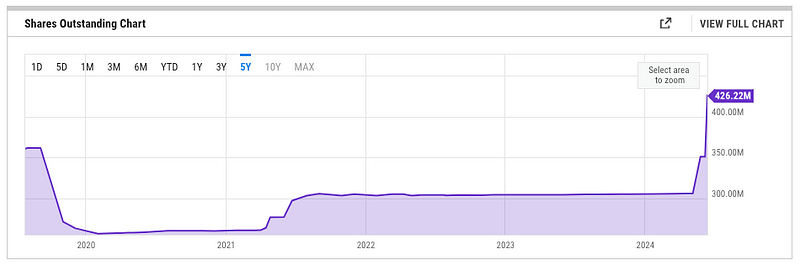

I’ll compare the number of outstanding shares to GameStop’s share price.

In 2019, when their share price was very low, GameStop performed a substantial share buyback, which is very good for investors.

However, when we had the first meme stock craze in 2021, to capitalize on that high share price, GameStop started issuing shares with the stated goal of expanding their e-commerce.

Then we had the meme stock craze round two, and GameStop issued even more shares.

GameStop’s Share Outstanding

GameStop’s Share Price

At the beginning of 2020, GameStop had 257 million shares outstanding. And now, in 2024, GameStop has 426 million shares outstanding. That is a 40% dilution for all shareholders that were holding back in 2020.

That is really bad for shareholders. However, if GameStop can create a lot of growth with that cash, maybe it’s not so bad. I wouldn’t mind being diluted 40% if GameStop was able to 10X their share price.

Has GameStop been successful with all of this dilution? What has it bought for shareholders?

To answer that question, I’m turning to their historical revenue.

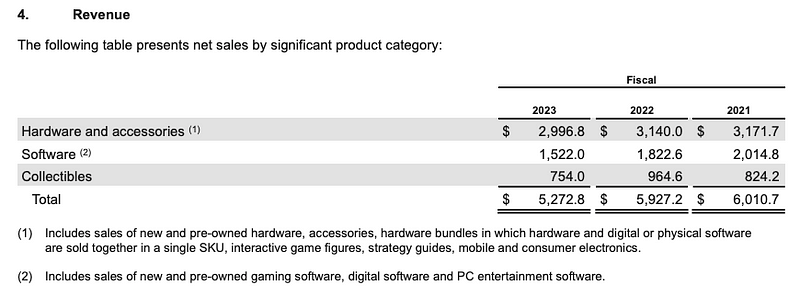

They have three major revenue streams: hardware and accessories, software, and collectibles.

GameStop’s 2023 Annual Report

Hardware and accessories have been dropping off since 2021 which we would expect as GameStop is shutting down stores. However, if GameStop was succeeding with e-commerce, I would expect to see software sales increase. Unfortunately, since 2021 software sales have dropped by 25%.

Furthermore, some of the hardware and accessories would be purchased through their e-commerce platform. If GameStop were truly expanding its e-commerce sales, I would expect to see that information front and center. I would expect to see revenue numbers broken out for both in-store purchases and e-commerce purchases.

I looked everywhere. I could not find that breakdown.

The fact that they’re not upfront with that information leads me to believe that it’s not going well.

Discounted Future Free Cash Flow

Now that I’ve created a narrative for myself and how I picture the direction of GameStop, it’s time to use some real numbers and model the intrinsic value of GameStop.

And for that, I like to use the discounted future free cashflow model.

Free cash flow is the money that a company uses to pay off its debt, reinvest in future growth, pay out dividends, or perform share buybacks. Basically, the free cash flow is my return on investment.

I don’t care about the earnings per share as much as I care about the free cash flow per share. I want to know how much free cash flow a company is generating right now and how much it expects to grow that free cash flow in the future.

I won’t go over every detail of the spreadsheet here. I’ve already made a full-length video for that or you can download my spreadsheet for free.

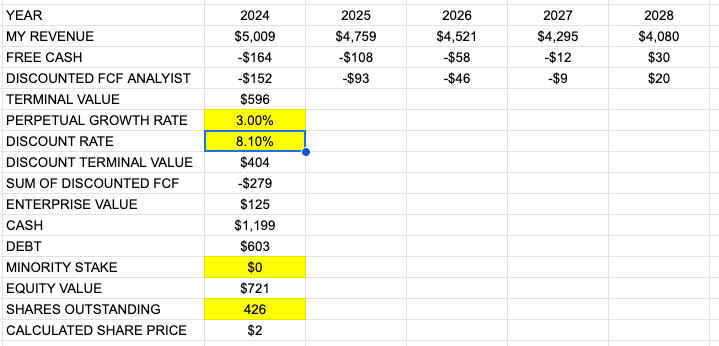

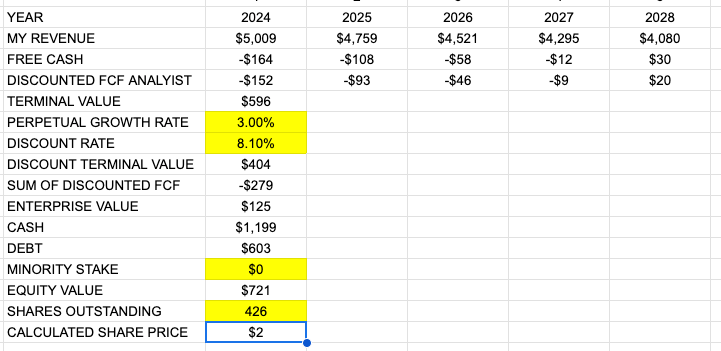

Calculating GameStop’s Intrinsic Value

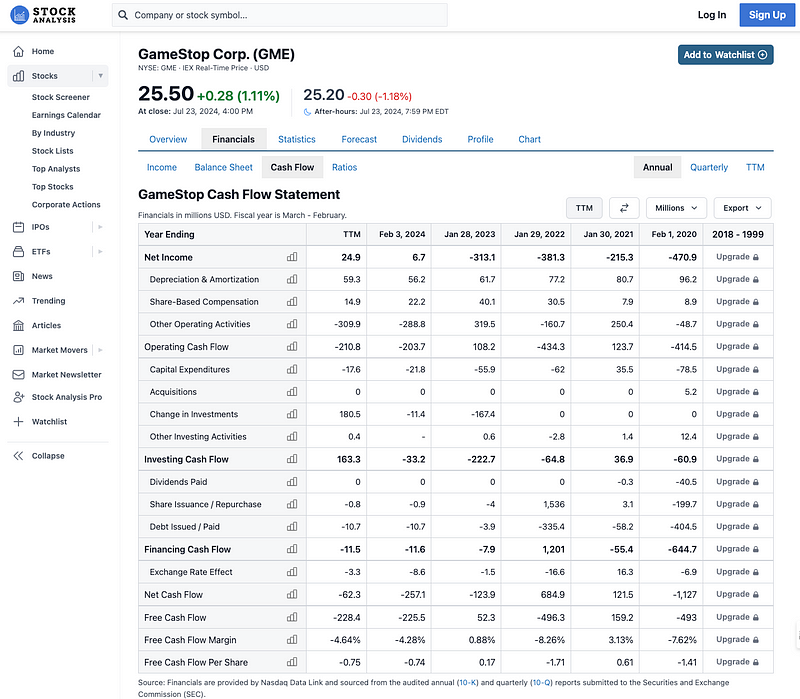

The past and present free cash flow I can find in GameStop’s financial documents.

GameStop’s Stock Analysis by Analysts

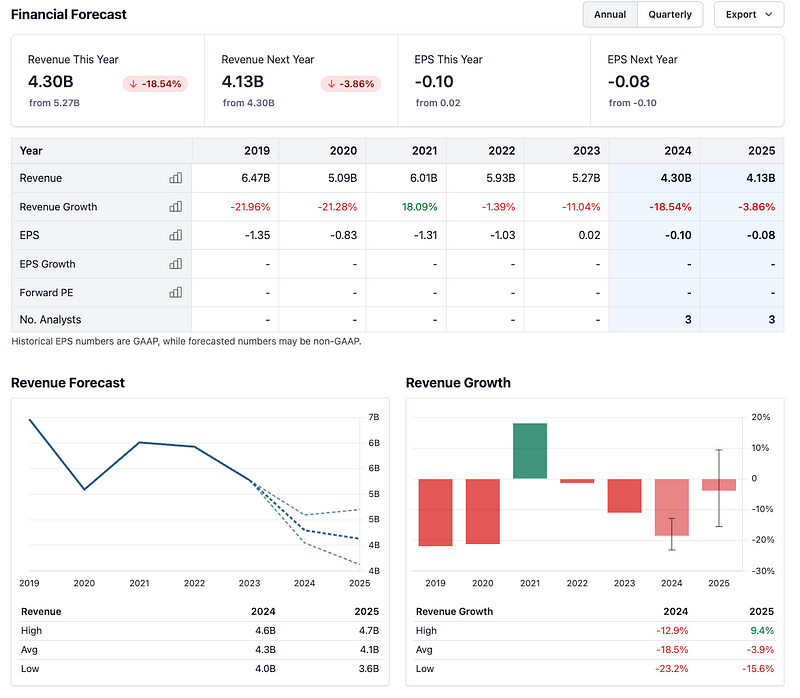

And the future expected free cash flow, I go to the analyst predictions. That’s their job after all.

And it’s not looking good.

GameStop’s Stock Analysis by Analysts

The analysts are projecting GameStop will lose revenue, dropping by 18.5% in 2024 and then a 4% drop in 2025.

This is not looking good.

Unfortunately, the analysts do not specifically predict the free cash flow, but one thing I can do is I can look at the past 5 years of free cash flow margin which is the percentage of revenue that is free cash flow.

I can use the historical average free cash flow margin, multiply by future revenues, and get a free cash flow projection.

GameStop’s Stock Analysis by Analysts

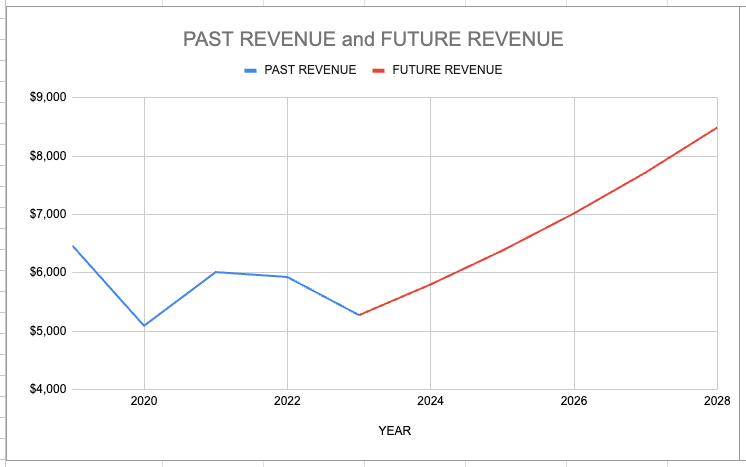

Also, for the discounted future free cash flow model, I need 5 years of revenue or free cashflow estimates.

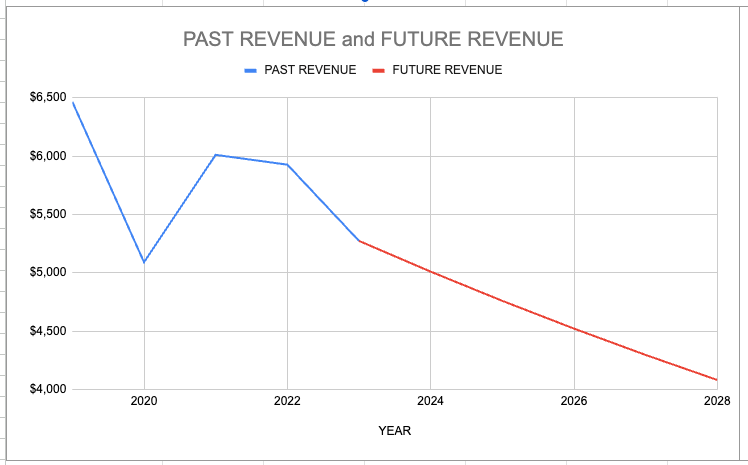

Unfortunately, the analyst did not project further out than 2 years. Since they are anticipating revenue decline, I will use the current trend to model future revenue.

I’m assuming that GameStop’s revenue will drop by 5% every year for 5 years, which is in line with what the analysts are projecting.

GameStop’s Financials — Spreadsheet by author

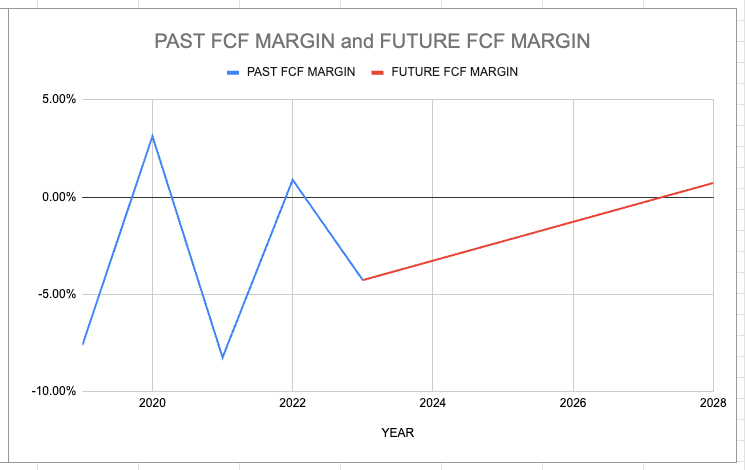

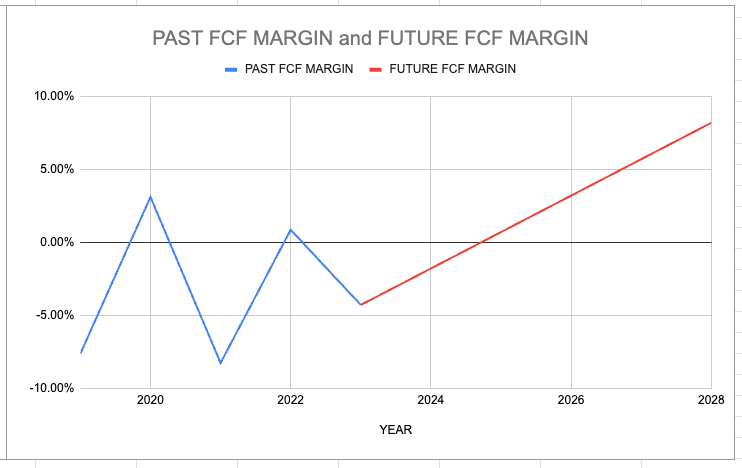

I’m also going to assume that GameStop’s free cash flow margin is going to improve over the next 5 years by 1 point every year.

Currently, their average free cash flow margin is -3%. So I assume that by 2028, they will have a 1% positive free cashflow margin, finally having a positive free cash flow.

GameStop’s Financials — Spreadsheet by author

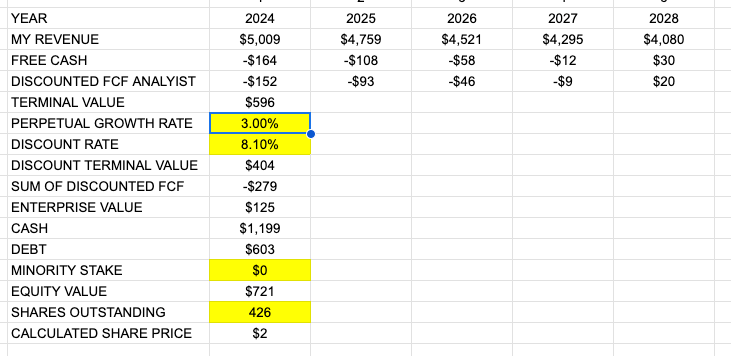

The next big assumption is the perpetual growth rate.

After the next five years, what is GameStop’s growth going into perpetuity? This is basically inflation.

I cannot use a growth rate faster than the growth of the economy because that would imply GameStop would eventually dwarf the entire economy. I will use 3% for the perpetual growth rate.

GameStop’s Financials — Spreadsheet by author

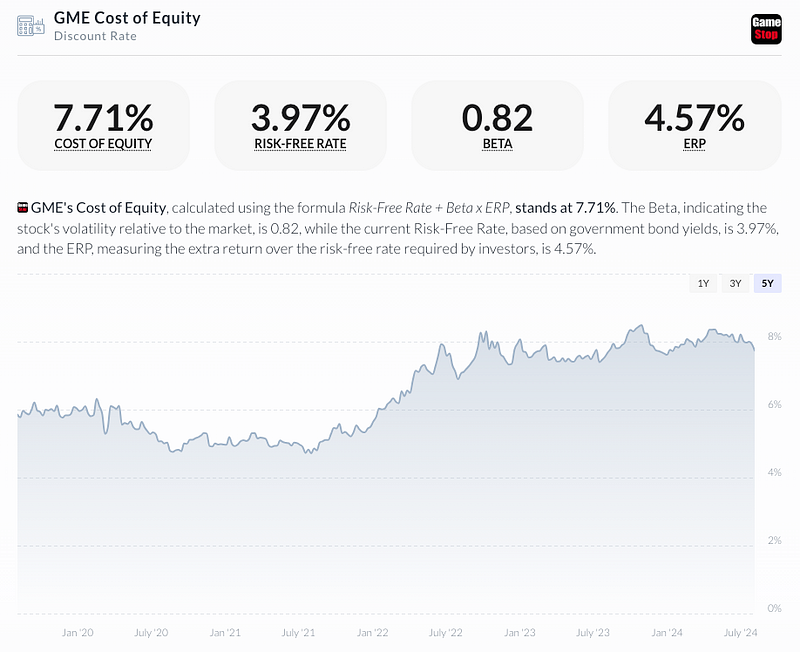

And the last assumption that I’m making, which is a big one, is the discount rate. I use the Cost of Equity as my discount rate.

GameStop’s Cost of Equity

This represents the return a company must offer investors to compensate for the risk of investing in the stock. That is also taking into account the inherent risk of investing in that company versus the market’s overall risk.

So for GameStop, that risk is about 7.71%. When I originally performed this analysis, the Cost of Equity was 8.1% but has dropped since then.

GameStop’s Financials — Spreadsheet by author

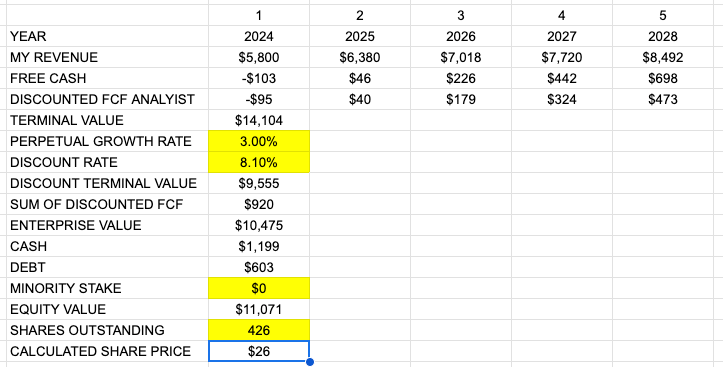

Now that all the assumptions are out of the way, the calculated fair value, according to the discounted future free cash flow model, is $2 per share for GameStop. And the current share price is about $25.

GameStop’s Financials — Spreadsheet by author

So, with this scenario, GameStop is way overpriced.

Next, I like to attack the problem from the other side.

What kind of revenue growth and free cash flow margin growth would justify the $25 share price today?

The following graphs show what it would take.

GameStop’s Financials — Spreadsheet by author

GameStop’s Financials — Spreadsheet by author

Despite what the analysts project, if GameStop can immediately start having a 10% revenue growth every single year for the next 5 years, succeed in improving their profitability, and increase their free cash flow margin by 2.5 points per year, then their fair value would be $26 while their current share price is $25.

GameStop’s Financials — Spreadsheet by author

However, when I look at the graphs and see the stark difference between what’s been happening and what would need to happen, and I also consider the analyst’s projections for just the next 2 years, it just doesn’t seem like it’s likely that GameStop is going to turn their situation around to such an extent.

Not only would they have to simultaneously shut down their worst-performing stores to improve their profitability, but GameStop would also have to generate positive revenue growth at the same time while shutting down stores. It just doesn’t seem likely.

So What Now?

Next, you’re probably going to want your own handy spreadsheet to perform the discounted future free cash flow analysis. You can DOWNLOAD MINE FOR FREE so you don’t have to worry about reinventing the wheel.

And you might want to use it to analyze NVIDIA. If you’re into games, then you’ve definitely heard of them. They have been absolutely popping off lately and I think a little bit too much. If you want to see my analysis on NVIDIA, you can check it out HERE.

Catch you on the flip side.

Reply