- The Moneycessity Newsletter

- Posts

- He Lost $215K in Intel Stock in 24 Hours (And How to Not Be Like Him)

He Lost $215K in Intel Stock in 24 Hours (And How to Not Be Like Him)

Many investors and stock traders post their trades on Reddit for the world to see. But one man took it to the next level by publically investing his grandma's inheritance money - $700K.

Brian Glass

September 16, 2024

This user, Sad_Nefariousness, managed to pick the single, worst stock to buy on that day. He bought Intel at an average price of $30.45 on the day that Intel would announce its quarterly earnings after market hours.

After purchasing the stock, he was down about $8K by the time he made the post on Reddit.

When the market closed that day, the price dropped to $29.11 as the market was expecting poor performance from Intel on their quarterly report.

He was now down about $30K, but this was only the beginning.

Intel significantly underperformed, earning only $0.02 per share which was just 20% of the expected earning which is $0.10 per share.

When the stock market re-opened the next day, Intel was now worth $21.06 and he had lost $215K of his grandma’s inheritance in less than 24 hours.

Intel stock had dropped more than any other stock in the S&P500.

On the go? Watch my video HERE.

He LOST $215K in Intel Stock in 24 Hours (And How to Not Be Like Him)

Why Should You Care?

I share this story not to pile on. I am sure this guy has enough of that going on in his life.

In fact, his head was in the right place. He was thinking long-term and he didn’t go out and blow his inheritance on drugs and alcohol. I share this story to cement an important lesson in my head: How to invest an unexpected windfall of money.

For investing a large sum of money, there are two factors to consider: what and how. What am I investing in and How am I going to invest it?

What to Invest In?

We have a young man who will be invested for a LONG time and will most likely not need this money any time soon. This is an important factor. He does not want to invest money in the stock market that he will need to spend in the near future. This is because the stock market can go through long periods of decline.

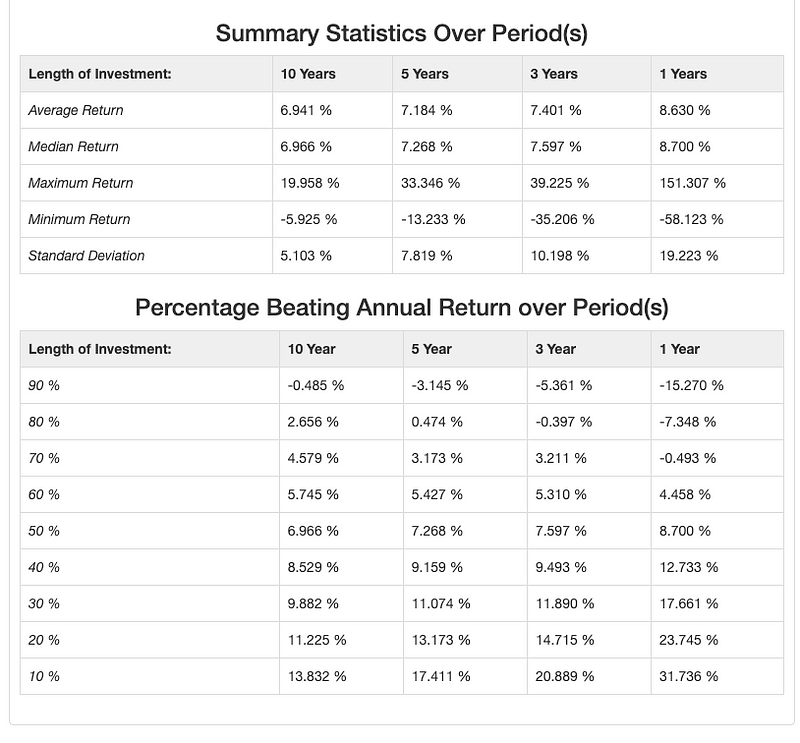

A good rule of thumb is to only invest money in the stock market that you will not need in the next 5 years. That way, you have over a 90% chance of making money at 6 years and beyond.

Even though he didn’t give context, it seems like Sad_Nefariousness accounted for this because he put $100K in a high-yield savings account. This amount would easily cover a downpayment on a house, buying a car, or any other emergencies that might come up. That is more than enough money to cover spending in the next 5 years. The remaining $700K is good to go for investing in the stock market.

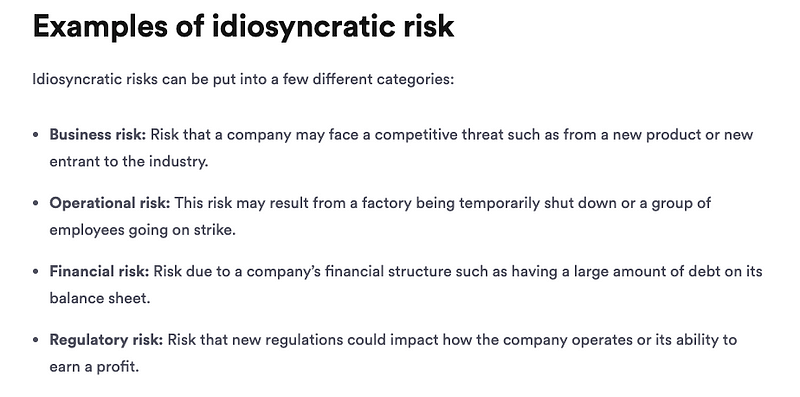

The risk of investing such a life-changing amount of money in a single company is too high. A single company carries additional risks that well-diversified index funds do not.

When I am invested in a basket of 500 companies with the S&P 500, all of these risks go away as they are spread out over all the companies.

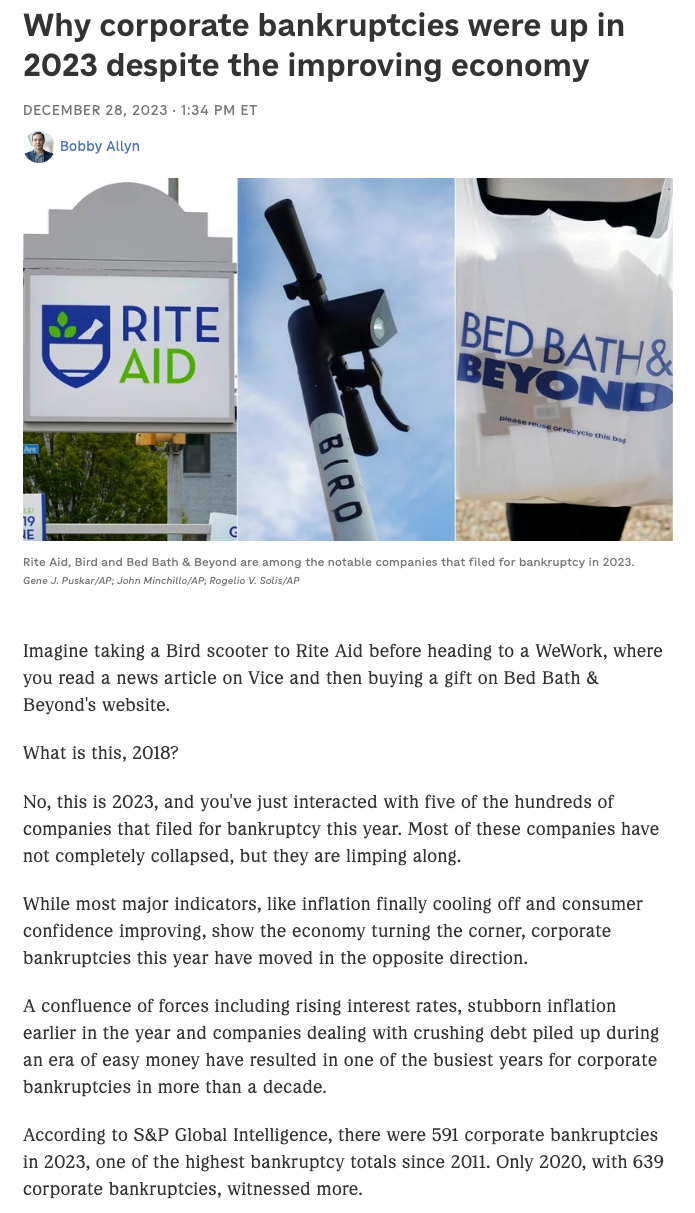

It is entirely possible that Intel will never recover back to $30 per share. Companies go to $0 every year. In fact, 591 companies in 2023 alone including Bed, Bath, and Beyond who filed for bankruptcy.

When you are talking about a life-changing amount of money, the chance to increase your investment returns by risking it with a single company is not worth the chance of reducing it to a not-life-changing amount of money.

How to Invest a Windfall of Cash?

The second factor to consider is how: Do I invest everything at once? What if the market crashes in the near future like with Intel? Maybe we should spread it out over many years and invest a small amount every day. What if the market flies and we miss a huge chunk of gains?

Either way you go, there is a chance that you will regret your decision. This debate is about lump sum investing vs dollar cost averaging.

Historically speaking, the odds are better with a lump sum investment. The stock market goes up over the long term so it is reasonable that I would want to get in as much as possible, as soon as possible.

In fact, Vanguard has already done the math. Lump-sum investing has outperformed dollar-cost-averaging 68% of the time. Not bad odds! However, there is a huge psychological element to consider.

It does not matter how mathematically sound your investment strategy is if you cannot stick to the plan!

Many people get too stressed by seeing their investments on the decline. Even though staying invested in the market is the correct decision, scared investors will pull their money out and won’t buy back in until the market seems safe — usually, they end up selling low and buy back in high.

All of this to say, the best plan for YOU might not be the best plan for EVERYONE because the single most important metric for success is adherence to the plan.

What Would I Do?

I am turning to Ben Graham, author of The Intelligent Investor, the most iconic investing book of all time and recommended by the greatest investors of all time.

Graham recommends investing between 25% and 75% of your portfolio in the stock market and the remaining percentage in bonds.

If I were to receive a windfall of cash, I would start at the bottom of Ben Graham's stock percentage and move to the top. I would invest 75% in a diversified bond fund like Vanguard’s BND and the other 25% in a diversified stock fund like Vangaurd’s VTI.

These are both great funds because they have very low fees. That is the main thing to consider when choosing a passive investing strategy.

Every year, I would sell 10–20% of my bonds and buy stocks. This way, I don’t risk ALL of my portfolio in the stock market in case of a crash and get to dollar-cost-average my bond investments into the stock market while still making a small return on that money. Once my portfolio is 75% stocks and 25% bonds, I will stop the dollar-cost-averaging.

I like this approach because I am confident that I can stick to it and I am always safely in the recommended portfolio allocation zone.

Additionally, the stock market is currently higher than the average according to the Shiller ratio.

I could not find a calculation comparing lump-sum to dollar-cost-averaging that took market conditions into account. But, higher valuations today do have a negative effect on future expected stock returns.

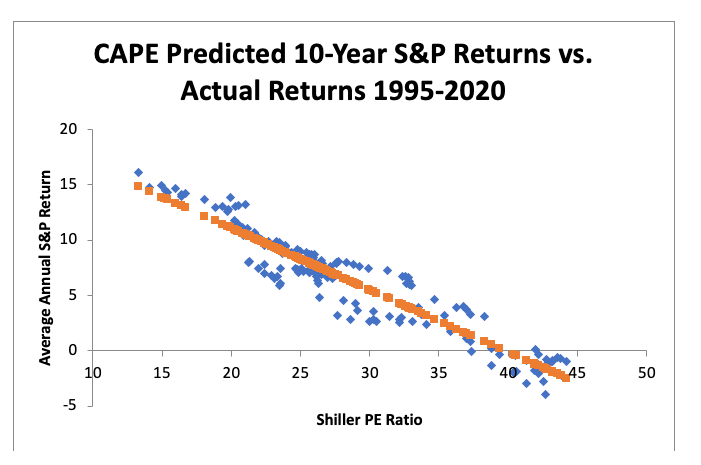

The Shiller Ratio is the average earnings per share of the S&P 500 over the last 10 years. When the Shiller ratio is very high, this is heavily correlated with lower expected future returns.

This graph shows the strong correlation between the Shiller Ratio (also known as CAPE) and the average annual return. Clearly, we are at a historically high Shiller Ratio.

I generally do not advocate for timing the market but if I am talking about a life-changing amount of money, I would err on the side of caution. A portfolio with a large bond percentage should have less volatility, and with today's market conditions, there is a good chance that I will have superior returns.

So What Now?

That being said, I currently do NOT have a life-changing amount of money so I do take on some additional risk. I use a small portion of my portfolio to invest in individual companies.

My favorite tool for analyzing companies is the discounted future cash flow model. Check out this video HERE to see my tutorial and snag my spreadsheet so you can easily perform the analysis yourself.

Catch you on the flip side.

If you enjoyed this article, consider joining my newsletter HERE.

Reply