- The Moneycessity Newsletter

- Posts

- How to COAST to Financial Independence (EVEN IF YOU'RE BROKE)

How to COAST to Financial Independence (EVEN IF YOU'RE BROKE)

What is Coast FIRE and how can we use Coast Fi to reach financial freedom? Instead of focusing on the dollar amount, tracking share count is a more stable metric towards financial independence especially when using dividend reinvestment plans (DRIP). Using the S&P 500 ETF (VOO) as an example, I am trying to figure out the share count to cover basic expenses taking into account compound interest and dividend reinvestment.

Brian Glass

March 14, 2024

Forget about a target dollar amount to reach financial independence — I use a much better metric.

Everyone’s portfolio is going to have massive swings up and down throughout our investing journey as the market booms and busts.

Focussing on my portfolio value just sets me up for depression.

I would overestimate my progress only to snap back to reality at the next market correction.

A much better metric of progress is to focus on share count.

Let me show you what I mean!

On the go? Watch my video HERE.

For quick context, financial independence is when our investments generate enough profit to cover our basic expenses for life. This can mean early retirement or pursuing a project I actually love.

With our basic expenses covered, the number of options exploded. Before financial independence, I can’t afford to be a full time Reddit moderator…

Back to the article.

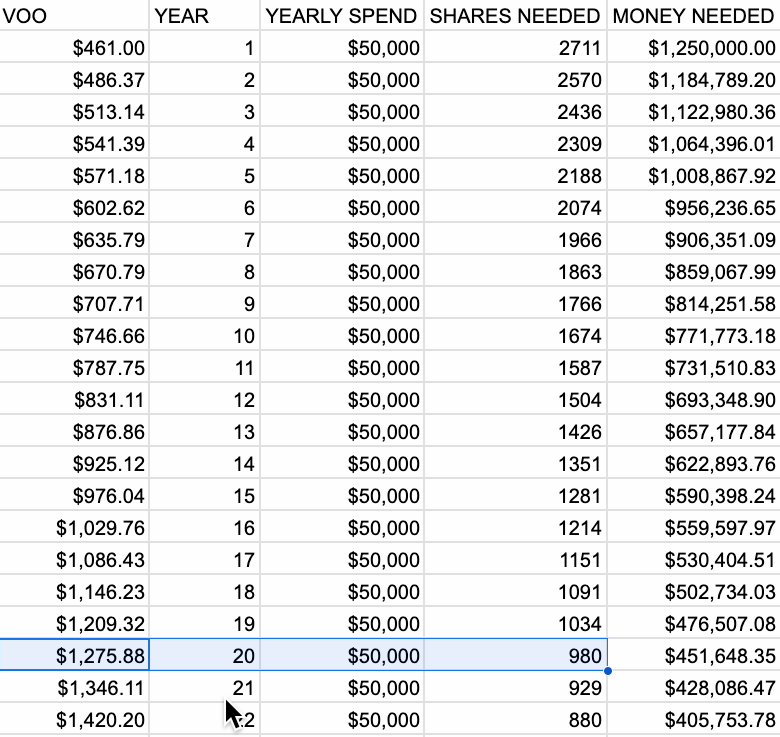

Let’s use the S&P 500 as our benchmark, specifically VOO — Vanguard’s S&P 500 ETF which is currently $461 per share.

The first question is, how many shares do I need today to be financially independent right now?

4% Rule to Retirement

If I need $50,000 per year to cover my basic expenses, then my portfolio value today will need to be roughly 25 times that amount.

This calculation is known as the 4% rule. Basically, you withdraw 4% from your portfolio initially in the first year, and then all following years, you increase that amount by inflation.

$50,000 times 25, which is the same thing as dividing by 4%, is $1.25 million.

The 4% rule is hotly debated. Many say it’s too aggressive but that is a topic for another video. Let me know in the comments what you think.

This means I would need 2,711 shares of VOO to be financially independent today. Unfortunately, that is not a reasonable goal for me.

Let’s say my goal was to achieve financial independence in 10 years.

How many shares would I need to have in the year 2034?

Let me give you a hint.

WAY less than $2,711.

Over the last 30 years, the S&P 500 has an average annualized return of just over 8%.

S&P 500 Investment Return Calculator

If we adjust for inflation and keep all of our numbers in today’s dollars, then the average annualized return drops to 5.5%.

That means, in 10 years, a single share of VOO adjusted for inflation will be worth about $745.

Long Term S&P 500 Investment Return Calculation by author

If I do the same math as before using a yearly spend of $50,000, then I will need 1,674 shares in 2034 to reach financial independence.

Thats more than a 1,000 fewer shares.

Let’s look at a second example.

If my goal was a little bit more conservative, and I wanted to reach financial independence in 20 years, that’s the year 2044, then a single share of VOO would be worth about $1,276.

Long Term S&P 500 Investment Return Calculation by author

Once again, a yearly spend of $50,000 adjusted for inflation means that I only need 980 shares of VOO to be financially independent in 20 years.

It gets even better when we expand on that.

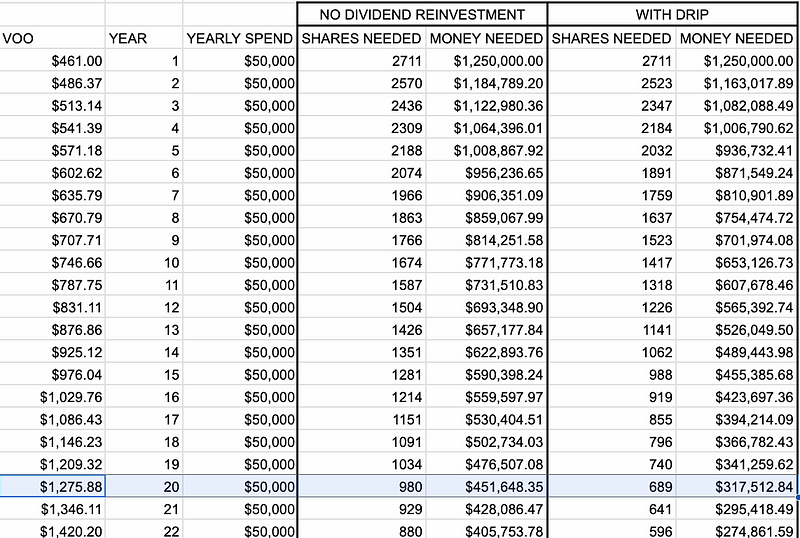

If I was able to buy 980 shares today worth $450,000, then I would actually have way more than 980 shares in 20 years if I were to reinvest my dividends.

This is known as DRIP (aka Dividend Re-Investment Plan).

What is a Dividend Investment Plan (DRIP Investing)

The average annualized return goes up to 7.5% if dividends are reinvested and used to buy more shares.

S&P 500 Investment Return Calculator

After accounting for the DRIP, we would only need to 689 shares today.

Long Term S&P 500 Investment Return Calculation by author

That would take $317,000, which is a huge improvement from $1.25 million. But still, that is a massive sum of money.

Let’s look at a more realistic scenario of dividend reinvestment.

In reality, I have savings to buy some shares, but not 689 shares.

For this example, let’s say I am 30 years old and I want financial independence by 50.

That’s technically 21 years so my target will be 645 shares of VOO.

Long Term S&P 500 Investment Return Calculation by author

Whether the market goes up or down in the meantime, I’m just stacking up the shares.

If I have $50,000 saved up between all my accounts (401k, Roth IRA, HSA, and brokerage), then I can buy 108 shares right now.

Just 581 to go, right??

Not exactly.

Dividend Investment Calculator

By the time I hit 50 years old with dividends reinvested, that original 108 shares will buy me 52 additional shares for a total of 160 shares.

Every share I buy early on will generate more shares of VOO.

From here on out, if I commit to buying 20 shares every year with DRIP, then I will have 645 shares at 50 years old.

And I only had to actually buy 508 shares with money out of my pocket thanks to DRIP.

With this mentality, market downturns are no longer a source of stress, but an opportunity to buy more shares for less money.

Now I must admit, I have not been completely honest. VOO might be one of the most popular ETF’s out there, but it is not my ETF of choice.

A higher annualized return allows me to cut years off of my financial independence timeline. Check out this video where I go over how to find the best ETFs that can outperform the S&P 500.

Catch you on the flip side.

Reply