- The Moneycessity Newsletter

- Posts

- Change Your Life by Investing in 2025

Change Your Life by Investing in 2025

2025 is my year to finally take control of my finances - because living paycheck to paycheck isn't an option anymore, and I'm ready for real change.

Brian Glass

December 14, 2024

If you’re still waiting for the perfect time to invest, here’s a hard truth.

It’s already here.

Let me show you why your age doesn’t matter, your income doesn’t matter, and if you’re waiting to start investing, it might cost you your dream life.

Watch the extended version HERE.

1. The “Why” of Investing

Before investing a single dollar, it’s important to understand why investing is such a powerful tool for improving our lives.

It all comes down to what money represents: freedom, time, and happiness. We need money to cover the essentials like shelter, food, and safety, but we also want it for the things and experiences that bring us joy.

Earning money takes time, so every dollar we spend represents a piece of our lives. If I waste money on something that doesn’t bring value, I’m essentially wasting the time I worked to earn it. That’s why I focus on spending only on what truly matters and saving the rest for things that will bring me even more value in the future. Saving also sets me up for the day I can’t or don’t want to work anymore.

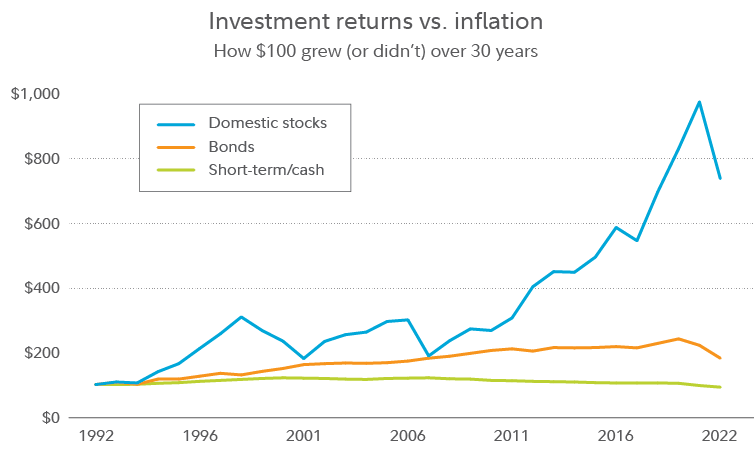

Investment returns VS Inflation

But here’s the problem: money sitting in a savings account loses value every year due to inflation. The price of everything keeps going up, so the same dollar buys less over time. That’s why saving alone isn’t enough. Investing stops the bleeding and goes a step further — it grows my money. When my investments earn enough to cover my expenses, I gain the ultimate freedom: the ability to stop trading my time for money.

Understanding this principle puts us ahead of most people, but knowing why investing matters is just the start. We need a solid plan.

2. The “How” of Investing

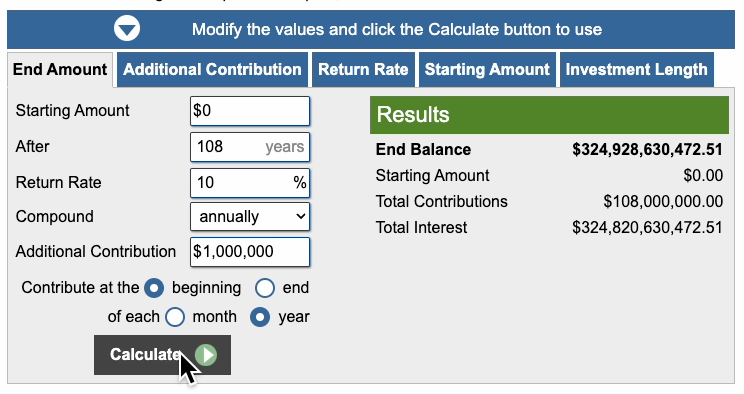

People love to point to someone like Elon Musk and say, “There’s no catching up to him, so what’s the point?” Sure, if Elon has $300 billion and I save $1 million every year, it would take me 300,000 years to match him. But Elon didn’t just save his money — he invested it.

If I invest a million dollars a year with 10% average stock market returns, it would only take 108 years to reach $300 billion. That’s the power of investing: turning an impossible timeline into something achievable.

Investment Calculator

I don’t have $1 million to invest every year, but if I start with $1,000 — money I’d usually waste on impulse buys, takeout, or random junk — and invest it consistently, it adds up. That $1,000 can double in about 7 years, turning into $2,000. If I invest $1,000 every year for 40 years, I could grow it into $486,000. When I’m 65 and ready to retire, that half a million will bring me so much more happiness than the junk I would’ve bought.

Investing $1,000 over 7 Years — Illustration by Moneycessity

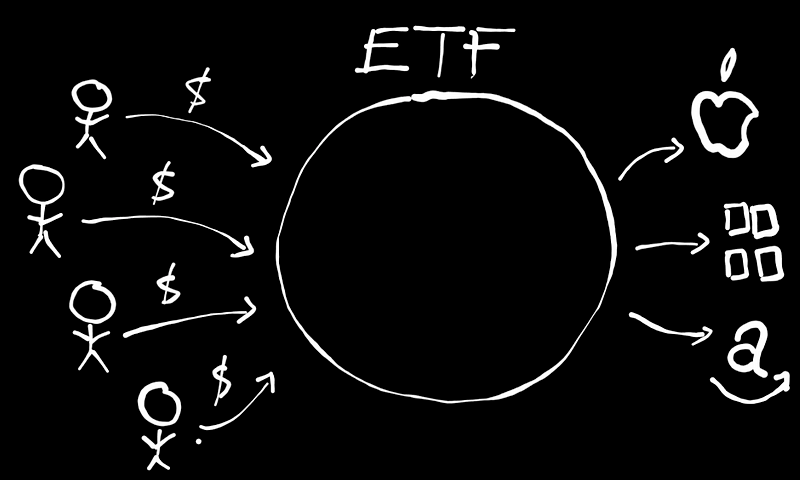

But investing isn’t about picking one hot stock. Companies rise and fall — look at Blockbuster. It was great for a while, but when it collapsed, investors who only bet on it lost everything. That’s why I don’t put all my eggs in one basket. Instead, I invest in index funds or ETFs. These funds pool money from lots of investors to buy shares in hundreds (or even thousands) of companies, spreading out the risk. It’s an easy way to invest in the entire U.S. economy — or even the global economy — and get reliable, average returns over time.

Index Fund and ETF— Illustration by Moneycessity

This isn’t about being flashy or finding the next meme stock. It’s about consistency. Small, steady investments can grow into something life-changing thanks to the power of compounding. It’s like building a Lego set piece by piece. And if you’re worried about starting too late, let me show you why that doesn’t matter.

3. The “When” of Investing

At what age does investing stop working?

It really comes down to time and probabilities.

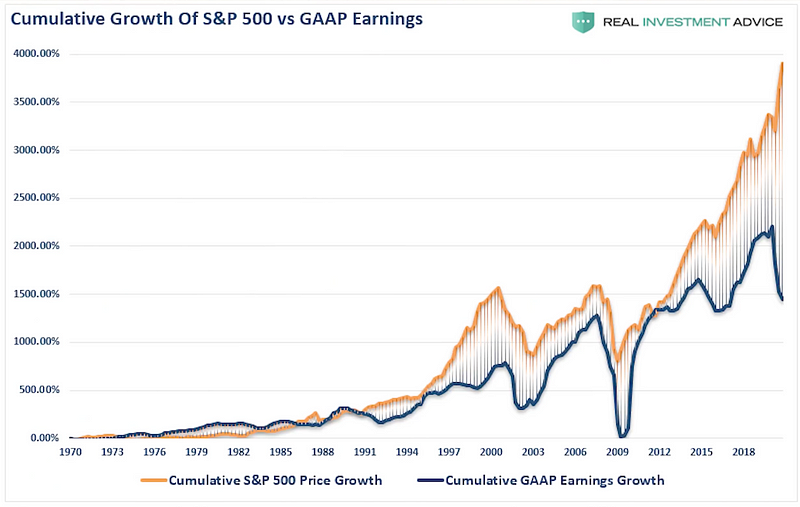

Over the past century, the stock market has returned an average of 10% per year, but that doesn’t mean it’s predictable in the short term. If I’m investing for just one year, it’s a coin toss — the market could go up or down, and no one knows for sure. Over 3 years, it’s a little more likely to go up, but still risky. By the time we’re looking at 10 years, though, the odds are overwhelmingly in my favor. Historically, 9 out of 10 ten-year periods in the U.S. market have been positive.

S&P 500 Performance VS GAAP Earnings

So, how does this tie into age?

It’s not so much about age as it is about how soon I’ll need the money. If I’m investing with a goal that’s 7 to 10 years away or more, I’m comfortable putting that money in the market. But if I need the money sooner — like right now my wife and I are planning for a baby — we save that money in a savings account. The stock market might go down in 2–3 years, and I couldn’t risk not having enough when the time came.

Even at 70 years old, if I came into some money and didn’t plan to use it for another 10 years, I’d still invest it. Why let it lose value sitting in a savings account when it could double in the market over that time?

The stock market rewards patience and long-term thinking. Once I understood that investing is about playing the long game, I stopped stressing over short-term dips. If you’re serious about building wealth, it’s all about time, strategy, and consistency.

If you’re serious about investing, there’s one more thing you need to know. I read and compiled 15 investing rules from the top 1% of investors and broke them down HERE.

Cheers!

Reply