- The Moneycessity Newsletter

- Posts

- How The 2024 Proposed Tax Plan Will Affect You

How The 2024 Proposed Tax Plan Will Affect You

After reading Biden's 256-page tax proposal for 2025, I understood its real impact on taxpayers including a reduced standard deduction and adjusted tax brackets that could result in higher taxes for many.

Brian Glass

June 28, 2024

Biden promised not to raise taxes on anybody making less than $400,000 per year.

Now, I’ve seen a lot of headlines out there. Some of them say one thing, some of them say something else, but these are pretty politically charged.

So I’m going to come to my conclusion.

I read Biden’s 256-page budget proposal explanation document. And because I’m a huge spreadsheet nerd, I made a master Excel spreadsheet where I looked at a few different situations.

Are you making less than $60K or over $120K?

Are you married or single?

Are you renting, owning, or building your first home?

Are you having kids and planning to have kids?

I found five big changes that are going to affect the most amount of people.

Now, there are huge changes to people making more than $400,000 and people with net worths of over $100 million, but it’s just such a small percentage of the population, that is out of the scope of this issue.

On the go? Watch the video HERE.

Who Does Biden’s 2024 Tax Plan REALLY Help?

1. Standard Deduction

The standard deduction is how much money you get to deduct from your income so that you pay less taxes every year.

Most people do not itemize their deductions, so I’m not going to cover itemized deductions.

If the standard deduction is lowered, then that is definitely a bad thing because you’re not able to deduct as much of your income.

2018 Tax Cuts and Jobs Act (TCJA)

In 2018, the Tax Cuts and Jobs Act increased the standard deduction a lot amongst a few other things, and that will expire in the 2025 tax year.

In Biden’s proposal, he makes no mention of extending that benefit in terms of the standard deduction. So what it looks like right now is that that is going away next year.

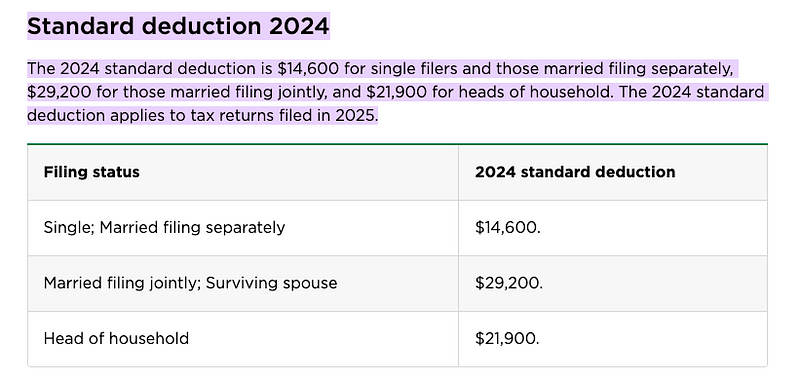

2024 Standard Deduction

So right now, the standard deduction for a single filer is $14,600. And if you’re married and filing jointly, then it doubles. That’s $29,200 you get to deduct from your income and pay less taxes.

Now if that goes down, the estimates that I’ve seen put the new standard deduction for single filers at $8,000 and for married would be $16,000.

2025 Tax and Budget Policy

So before I show you the numbers and how much it’s going to affect your bottom line, let’s look at how the tax brackets changed. So let’s go ahead and move on to that.

2. Tax Brackets

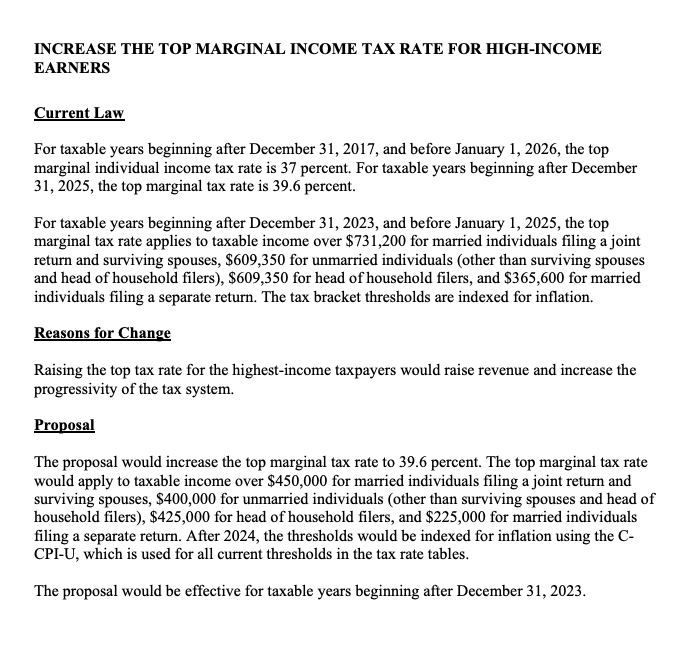

The proposal would increase the top marginal tax rate to 39.6% from 37%.

The top marginal tax rate would apply to taxable income over $450,000 for married individuals filing a joint return and $400,000 for unmarried individuals.

The proposal would be effective for taxable years after December 31st, 2023.

Biden’s 2024 Budget Proposal Explanation Document

This is a proposal so this may not get accepted. But if it is, whenever you’re paying taxes in April 2025 for this year, these rules are going to be in effect.

In the document, Biden does not give any guidance on how the other tax brackets are going to shake out below the top tax bracket.

There are two ways I think he can do this:

He can either truncate that tax bracket and keep everything below it the same

He can scale everything down, and keep it all proportional so that the top tax bracket is $400,000.

2024 Tax Brackets for Single Filers — Illustration by author

On the right is the one that I scrunched, I kept everything proportional. The bracket on the left, I just truncated that top bracket.

Now, if he is scrunching, people making less than $400,000 are absolutely going to be getting taxed more. We already saw that the standard deduction is being reduced. If you scrunch the tax brackets, then you are gonna be bumped up into a higher tax bracket at lower income levels.

I’m leaning more toward the truncated version.

The truncated version's tax brackets for a single filer would not be affected up to the 32% tax bracket. The 35% tax bracket would be truncated so that you would be jumped up into the 39.6% bracket once you make more than $400,000. Whereas before you had to be making $609,000 or more to be jumped up into that top tax bracket.

2024 Tax Brackets for Single Filers — Illustration by author

Now let’s look at married. This is where things get a little more interesting.

If you are married and filing jointly, the lower tax brackets are essentially doubled going from a single filer to a married filer. In this case, I cannot double the higher tax brackets from the single filer because it would push me above the $450,000 income limit that he specified for the 39.6% bracket.

The way I dealt with this on the truncated version is I doubled all the ones that I could and then I scaled back the higher tax brackets. And then on the scrunched version, everything could be doubled because everything is just proportionally reduced.

So that one looks a little bit cleaner for the married version but I still think the truncated version is more likely.

2024 Tax Brackets for Married Filers Filing Jointly — Illustration by author

Now on the truncated married filing jointly tax bracket, the upper tax brackets are scrunched a little bit so you will be bumped into a higher bracket sooner.

For married people filing jointly, if the household income is above $323,000, I’m projecting you’ll be bumped up into a higher tax bracket. So I find it hard to believe that people married filing jointly will be unaffected under $400,000 just because everything is going to get scrunched at those upper levels.

I think the truncated version is more likely to happen so I’m going with the truncated version. Now I’m going to look at a few different situations to see who is going to be benefiting and who is going to be paying more taxes.

1. Single Filers

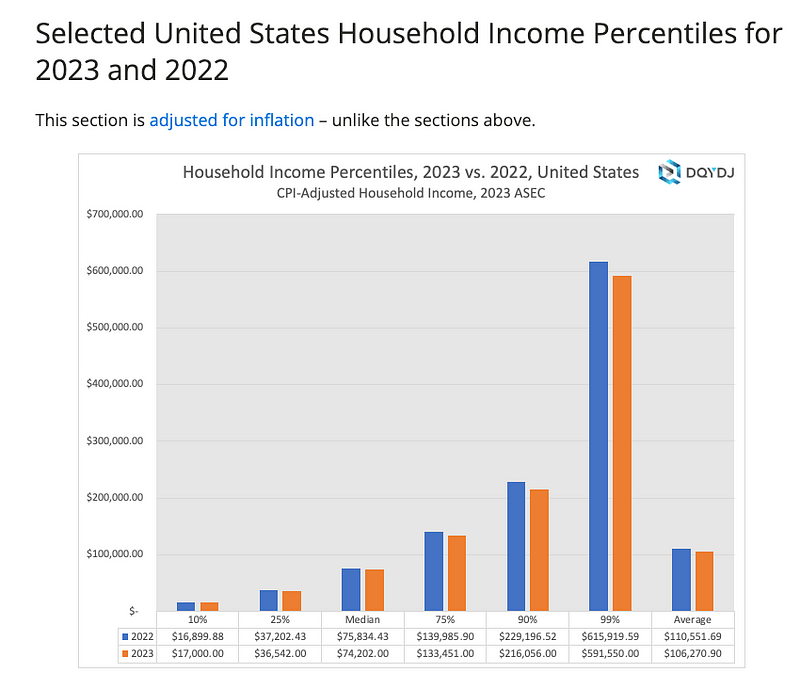

2023 vs 2022 US Household Income Percentiles

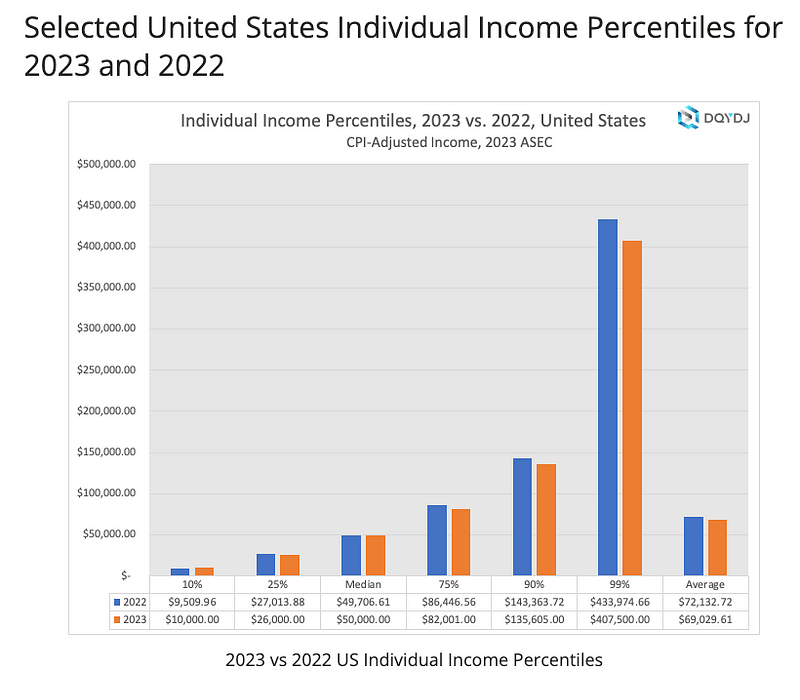

Let’s start with the medium single income which is $50,000 per year. And then I chose an income on the lower side which is $35,000 per year. And then I decided to go with a top 10% earner which is $135,000 per year.

2024 vs 2025 Tax Bracket for Single Filers — Illustration by author

Low Income: Using the new standard deduction and the truncated tax brackets, somebody making $35,000 per year would pay $792 more in taxes, which would be an increase of about 35%. Before the changes to the tax bracket, you’d be paying about $2,216. After the changes, you’re paying about $3,000.

Median Income: You’re paying $792 more per year, but this time it only represents about a 20% increase in taxes. Before, you’re paying about $4,000, now you’re paying about $4,800.

High Income: Before the tax changes and before the changes to the standard deduction, you’re paying about $22,082. Whereas after the changes, you’re paying $23,666. This is about a $1,600 tax increase which represents only a 7% increase to your taxes.

So in terms of percentage, the lower income earners are actually paying a greater percentage more on their taxes than the higher income earners. Just an interesting observation.

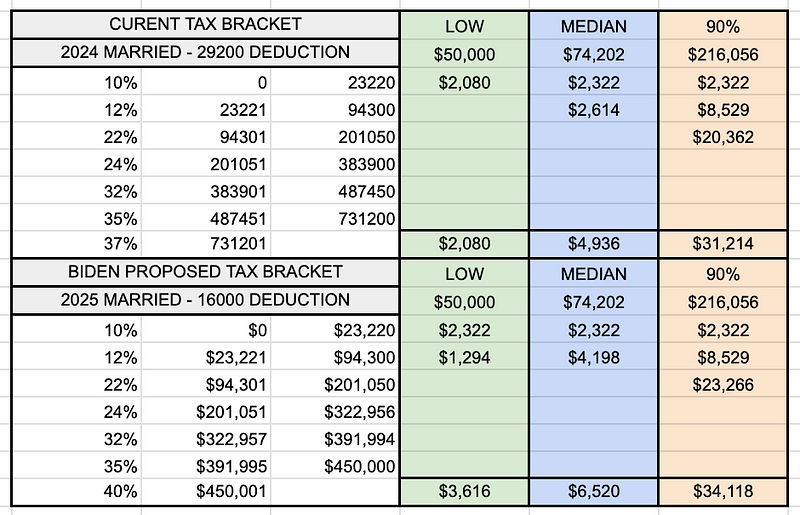

2. Married Filers Filing Jointly

2023 vs 2022 US Household Income Percentiles

For married individuals filing jointly, the median income is about $74,200. You’re expected to pay $4,936 in taxes before. After the tax plan, you are going to be paying $6,500 in taxes. So that is a $1,584 increase, a 32% gain.

2024 vs 2025 Tax Bracket for Married Filers Filing Jointly — Illustration by author

Low Income: The lower-income household filing jointly is $50,000 per year. You’re paying $2,000 before and now you’re paying $3,600. That is a $1,500 difference for a 74% increase.

Median Income: If you’re married and filing jointly, these scrunched tax brackets have a much bigger impact especially the fact that you have a lower standard deduction. This is a 32% increase.

High Income: If you’re a top-10 income household making $216,000 per year, you’re expected to pay $31,200 before and after $34,118. That is a $2,900 difference but only a 9% increase.

If you’ve made it this far, you’re probably feeling how I feel.

We’re going to be paying more in taxes and we’re screwed, right?

Well, don’t lose too much hope yet. There’s a light at the end of the tunnel.

Biden did include three huge tax credits in his proposal that affect people from different walks of life, in different situations.

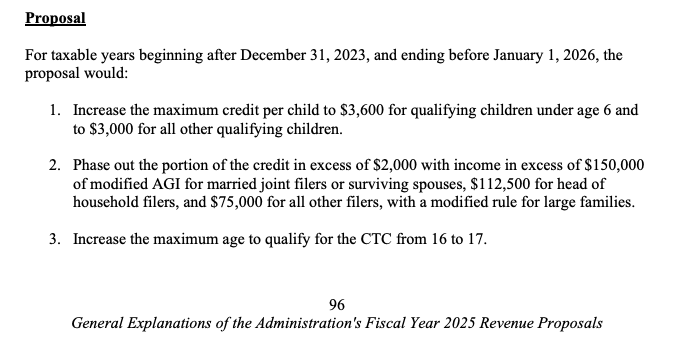

3. Child Tax Credit

Currently, this tax credit awards a maximum of $2,000 per qualifying child, but only $1,600 of it is refundable.

What refundable means in this context is:

If you owe $0 in taxes, you only get a $1,600 tax refund.

If you owe $2,000 in taxes, you get a $2,000 tax refund.

If you owe $3,000 in taxes, you still get a $2,000 tax refund.

Biden’s 2024 Budget Proposal Explanation Document

Biden is actually pumping this tax credit up quite a bit.

For children that are 5 years and younger, you’re getting $3,600 fully refundable for qualifying children. And then for 7 years and older up to 17, you get $3,000 fully refundable.

So if you have three kids between 7 and 17 years old and you make $0 income, you’re getting the full $9,000. Whereas before, you would only be getting $4,800 because before only the $1,600 is refundable.

I made this chart here just so at a glance you can see having different numbers of kids and how much more in credit you’ll get compared to the previous tax plan.

2024 Child Tax Credit — Illustration by author

If you have two kids 6 or older, you’re going to be getting at least $2,000 more in tax credit. If you have three kids all under 6, you’re getting at least $4,800 more in tax credit.

So if, this is the big IF, if you’re having kids that are under 17, then you are likely to benefit more from Biden’s tax plan.

Now, I’m not saying you should just go out and start having kids so you can make some money. Of course, kids are very expensive but this is a little bit of a silver lining. If you have some kids, you know, your taxes are not probably going to go up very much if at all.

That’s great for people who have kids or are planning to have kids, but that’s not everybody.

So let’s move on to the next substantial tax credit that’s going to affect a big group of people.

4. First-Time Homeowner Tax Credit

This credit gives first-time home buyers a $10,000 credit and first-time home sellers a $10,000 credit.

Biden’s 2024 Budget Proposal Explanation Document

So if you’re lucky enough to buy your first home and sell your first home, that’s $20,000 in credit.

Natalie and I already bought our first home, so we’re going to miss out on the $10,000 home buyer tax credit. But if we are going to sell, maybe we can catch the second half.

This credit does start to phase out for single-income earners who are making over $100,000 per year and married filing jointly household income of over $200,000 per year. So I’m just going to focus on below those limits.

Biden’s 2024 Budget Proposal Explanation Document

So if you are married and filing jointly and you’re making the median household income which is $74,202, then you are expected to pay $6,520 which is a $1,500 or $1,600 increase over the previous plan.

2024 vs 2025 Tax Bracket for Married Filers Filing Jointly — Illustration by author

If you’re able to get the $20,000 tax credit, then that’s going to make up for more than 10 years of that tax increase.

So if you’re going to be buying and selling your first house, you’re not going to have to pay more taxes, at least in the short term to medium term in the medium term because of those big tax credits.

I should also note that both of these tax credits are fully refundable, so it doesn’t matter what your income is at the time that you buy or sell the house, you’re still going to get the full $10,000 credit.

So that’s great for people who can buy and sell a home, but not everybody is in a position or even wanting to buy and sell their first home.

So let’s look at people in the low and moderate-level income tax brackets.

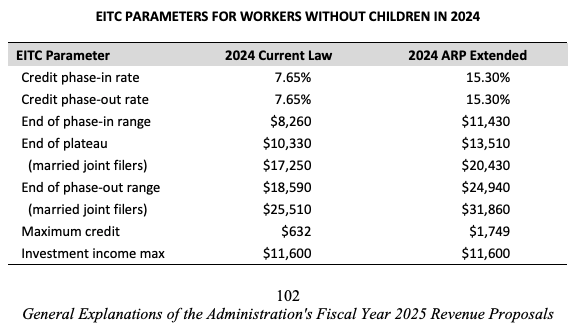

5. Earned Income Tax Credit

A tax credit that will benefit them is the earned income tax credit.

Low and moderate-income workers may be eligible for a refundable earned income tax credit.

Biden’s 2024 Budget Proposal Explanation Document

This means that you have to show an income within certain thresholds to get the credit.

This table here shows where the credits phase in and where they phase out.

The maximum credit under the current law is $632, whereas the ARP Extended version which is what Biden wants to reinstate $1,749.

This is more than a $1,000 increase which would more than make up for the increase in taxes that lower-income earners would expect to pay from the reduced standard deduction and the scrunched tax brackets.

So let’s see who qualifies for this.

Biden’s 2024 Budget Proposal Explanation Document

Current 2024 Version: This credit phases in as you make up to $8,260. And then from $8,260 to $10,330, it hits a plateau where you’re making a maximum of $632. And then it phases out as you get to $17,250.

Biden’s 2025 Version: The phase-in range goes to $11,430 when it hits its plateau. And then the top of the plateau is at $20,430 where you’re making a maximum of $1,749.

It’s important to remember at these income levels, you are going to be paying very little in taxes so it makes a huge difference that these credits are fully refundable.

Remember, you’re going to be in the 10% tax bracket and you’re going to be having the standard deduction. So even if you have $0 tax bill at the end of the year, you’re still going to get the full $1,750 credit.

So What Now?

Unless we fit into one of these categories: low income, having kids, having a house, we are going to be paying the taxes out our asses which is why I take full advantage of my tax-sheltered accounts.

I’m sharing all about how I save thousands of dollars every year HERE.

Catch you on the flip side.

Reply