- The Moneycessity Newsletter

- Posts

- EASIEST Credit Card Combo in 2024

EASIEST Credit Card Combo in 2024

What is the best credit card combo for 2024? I grew tired of carrying around so many credit cards that I didn't even use. So I set out on a mission to find the EASIEST credit card strategy to maximize points and benefits, while avoiding the hassle of carrying multiple cards.

Brian Glass

February 12, 2024

8 credit cards in my wallet, and I don’t even use them all.

So, over the past week, I’ve researched 30 different credit card combinations to achieve 2 goals:

Take advantage of multiple credit cards for maximum points.

Avoid the annoyance of carrying 8 or more credit cards in my wallet and having to use a different one for every store.

And don’t get me wrong I’ve seen a lot of strategies out there that utilize a ton of credit cards. But for me, it’s just not sustainable.

If I fail to utilize all the credit cards, then the annual fees start to eat into my hard earned gains. And there is nothing more frustrating.

So I have put together the ultimate 5 credit card combination that maximizes passive bonuses while minimizing card swapping for different occasions.

On the go? Watch the video HERE.

Let’s get into it.

What Should the Perfect Credit Card Combo Have?

There are three roles that a convenient credit card combo needs to fill.

Daily Spender

First, I need a solid daily spender. I need a workhorse, a card that I can use for the vast majority of my purchases.

The more I can utilize my workhorse while still benefiting passively from my other credit cards, the more convenient my strategy will be.

Bonus Boys

Second, I need my bonus boys. I need some cards that I rarely have to use and I still benefit passively from annual bonuses.

Specialty Spending

And finally, the third category is specialty spending credit cards.

This is the category that I’m looking to minimize.

These are cards that you only use in very specific circumstances. You might have a card for Amazon. You might have a card for groceries, for dining out, for home improvement, etc.

For this category I am only picking up a specialty card if it has no annual fee and significant upside. That way there’s no pressure if I don’t use it at least I won’t get hit by an annual fee.

Which One Credit Card Are We Ranking Against?

Now, before I show you my workhorse credit card, let me first explain the benchmark by answering the questions: What are we trying to beat?

In this case, I want to compare it to the simplest strategy out there. The quintessential one credit card user that wants simplicity. They don’t have to think about rotating categories, they don’t have to think about any categories.

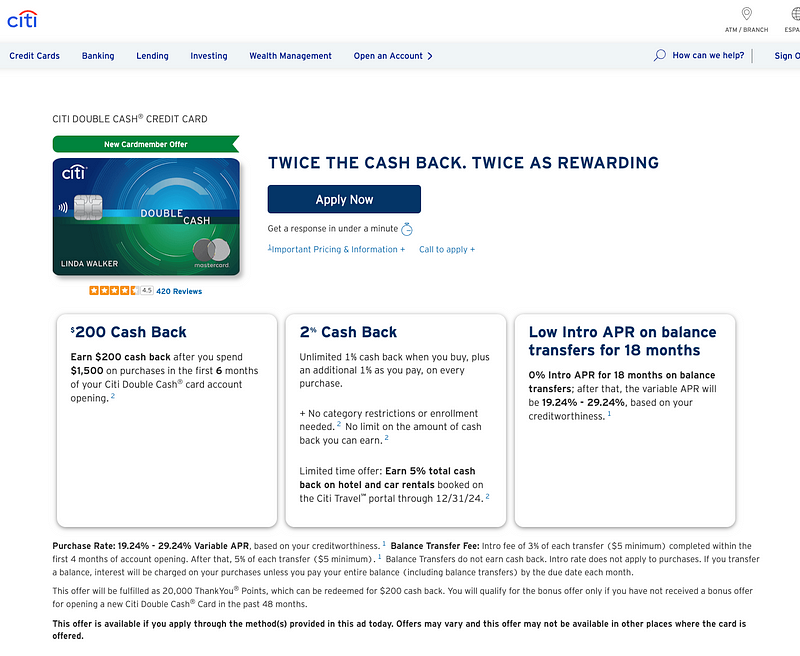

The card that fits this bill is the Citi Double Cash credit card.

Citi Double Cash Credit Card Sign-up Bonus

This credit card gives you a flat 2 points per dollar spent. There’s no annual fee. There’s no annual bonuses. You just use that card all year.

Easy.

I’m gonna use mine and my wife Natalie’s budget to compare how many points we get from the City Double Cash card versus the 5 credit card combination.

The Daily Spender

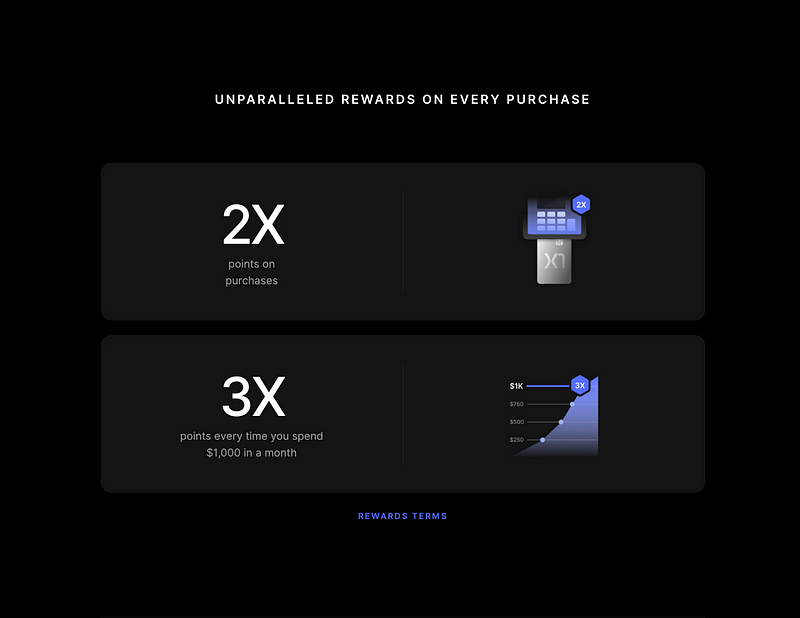

The workhorse credit card that I’ve selected for this system is like the Citi Double Cash Plus Plus.

It’s got no annual fee, it’s got no annual bonuses, and it gets 2 points per dollar spent until you spend $1,000 in that month. Every dollar after that, you get 3 points per dollar spent.

Are you familiar with this card? It’s the X1 credit card.

Robinhood X1 Credit Card

Let’s pop over to my ultimate spreadsheet and see how this credit card fits into mine and Natalie’s budget.

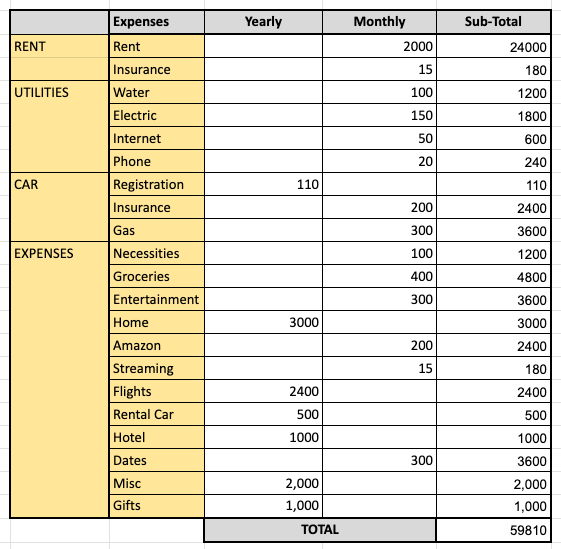

Budget Spreadsheet by author

There are 10 categories where the X1 will be used in our budget. This accounts for almost all of our daily spending categories — the only exception being groceries and necessities.

Our entertainment, home expenses, Amazon, streaming, date night, gifts, miscellaneous — this is the credit card that we’re going to be using more than any other card.

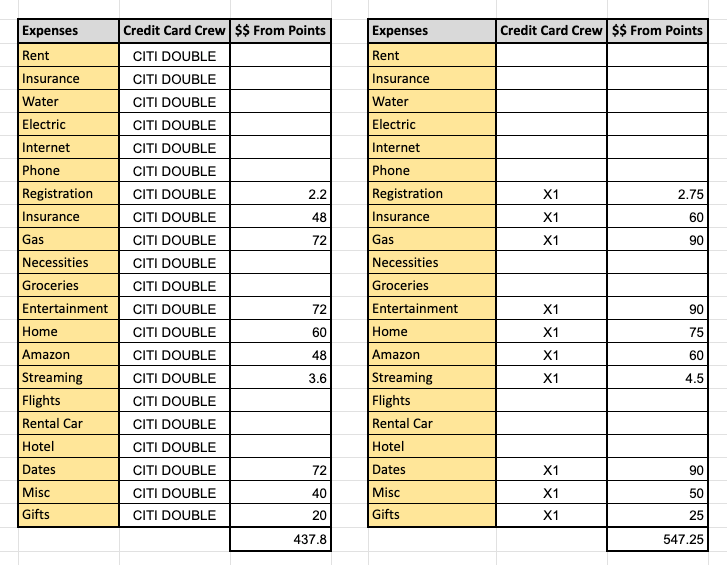

Annual Credit Card Spending by author

And then you can see at the bottom. that we’re getting nearly $550 in value from the X1, while the Citi Double Cash from those same categories is only going to get us about $440 in value.

The Bonus Boys

The second role in my credit card system is the bonus boys. These are the credit cards that take advantage of passive annual bonuses and automatic payments online.

The One Who Rents

The first bonus boy in my system takes advantage of the rent payment. This is the first and only credit card that I’m aware of that gives you cash back on your rent payment and refunds that service fee that you get if you try to pay your rent with a credit card.

The only catch here is you have to have at least 5 transactions on your credit card every month in order to get the bonus. The most convenient way to make sure you get 5 transactions on this credit card is to use it for your monthly repeatable expenses.

The first bonus boy is BILT.

BILT Mastercard Reward Points

This card has got $0 annual fee and it has pretty decent points per dollar spent. You get 3 on dining and 2 on travel, but that’s a little bit irrelevant because we’re going to set this card up to hit the 5 transactions with just the automatic monthly expenses.

Now, if worse comes to worse and you can’t hit all 5 with your automatic monthly expenses, then you can go out to eat once a month or twice a month and get 3 points per dollar spent on dining.

Annual Credit Card Spending by author

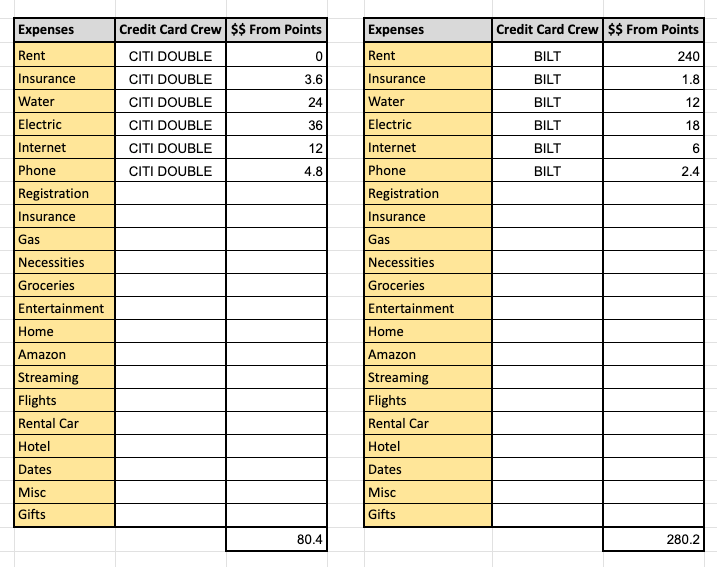

The BILT credit card fits into mine and Natalie’s budget in 6 different categories.

Of course, we’re going to take advantage of the rent points, which no other credit card can do. To make sure that we hit our 5 transactions per month, we’re going to pay our renter’s insurance, water bill, electric bill, internet, and phone bill on the BILT card.

The BILT credit card is giving us $280 in value from those six categories, while the city double cash credit card is only giving us 80 points.

This is mainly because it is not able to take advantage of the rent payment.

The One Who Travels

The second bonus boy in my credit card system is a travel beast.

This credit card is intimidating at first because of the really high annual fee of $395 but the annual bonuses quickly make up for that. You get a $300 annual travel credit, a $100 anniversary bonus, and $150 in lounge access. And you get free Global Entry and Pre-check, which is a $100 value every 4 years which averages out to about $25 per year.

On a quick side note, I’m not factoring in any of the signup bonuses on any of these credit cards. I’m not planning to use this as a churning strategy. These boys are here to stay.

The second bonus boy is the Venture X credit card. On top of all the annual perks I just brought up, this card gets really good miles per dollar spent on flights and rental cars.

Venture X Credit Card

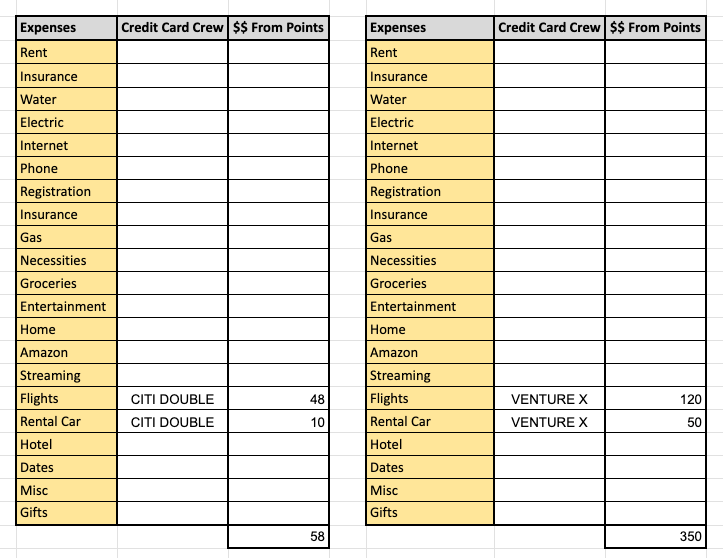

Since I only take about three trips per year and I’m already in a planning mode when I’m making these transactions, I’m okay with busting out a different credit card to pay for my flights and my rental car, especially since it’s going to get me some extra value.

On my credit card spreadsheet, I’ve added up all the annual bonuses and subtracted the annual fee for a total yearly value of $180.

Then on mine and Natalie’s budget, you can see that the Venture X gets us $120 for flights and about $50 from paying for a rental car. You add that to the annual bonuses and we’re getting $350 from Venture X and only about $58 from the Citi Double Cash.

Annual Credit Card Spending by author

The One Who Loves to Stay in Hotels

The third and final bonus boy is a hotel credit card.

This hotel credit card has a $95 annual fee, but it makes up for it instantly with an anniversary bonus of $180 in hotel credits. Additionally, we’ve got the second Global Entry and Pre-check. I’ve got mine paid for from the Venture X and Natalie gets her paid for with the hotel credit card.

On top of the great bonuses, this card has pretty good cash back on gas, home improvement, phone, grocery, and Choice Hotels which might give away that this card is the Choice Privileges Select Credit Card.

This credit card fits into mine and Natalie’s budget in just one spot: hotel expenses. This card gives you an insane 12.5 points back for every dollar spent while the city double cash just gives you 2 points per dollar spent.

Annual Credit Card Spending by author

After adding the points earned from dollars to the annual bonuses, the Choice Preferred credit card gives you $235 in value compared to the $20 from the City Double Cash.

The Specialty Spending

This is the last credit card I’m going to show you before we look at the final scoreboard comparing the Citi Double Cash to my 5 credit card system.

The final category is the specialty spending credit cards. I only threw one specialty credit card into this system because:

It has no annual fee

It’s very easy to implement

It provides significant value above my workhorse credit card.

This specialty credit card has a rotating cashback schedule. And I know I talked trash about rotating cashback earlier, but this one is different than any that I’ve seen before.

It doesn’t change categories based on a rotating quarterly calendar. You effectively get to pick your own category. Whichever category you spend the most on in a given month, that is the category that gets the 5 points per dollar spent.

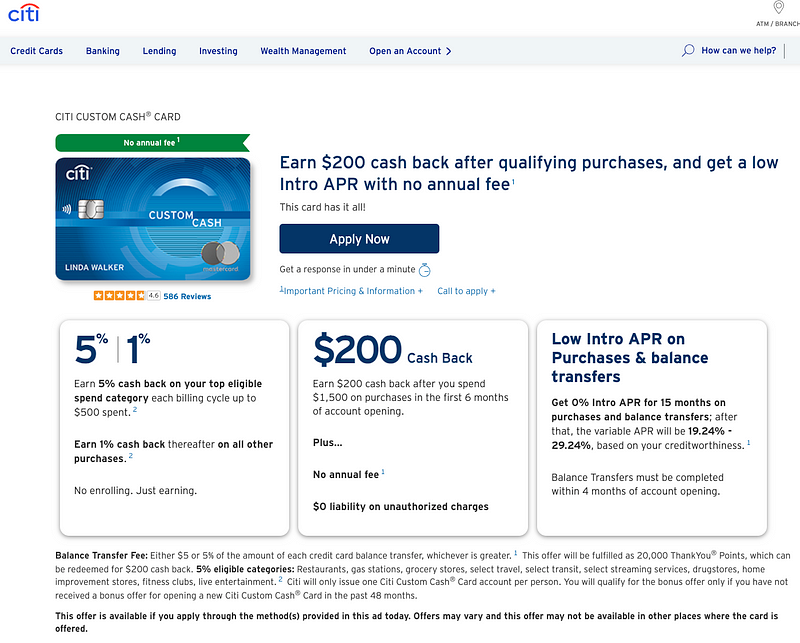

This is an incredibly useful credit card to fill in the gap if there’s any category that you missed with your other credit cards. Maybe you’ve heard of this card. This is the City Custom Cash credit card.

Citi Custom Cash Sign-up Benefits

The most natural spot for this credit card to fill in mine and Natalie’s budget is grocery stores. At 5 points per dollar spent, we’re getting $300 in value in total from the Citi Custom, when we would only get $120 from the Citi Double Cash Credit Card.

Annual Credit Card Spending by author

How Much Money Did We Make From This Credit Card Combo?

Here’s the moment you’ve been waiting for the final scoreboard comparing the City Double Cash to my 5 credit card crew featuring the bonus boys, the workhorse and the one specialty spender.

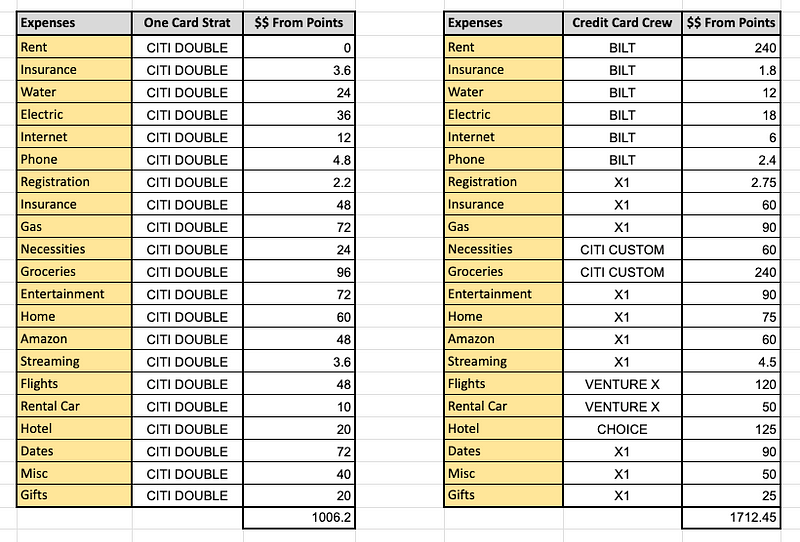

After it’s all said and done, the City Double Cash credit card gives you $1,000 in value for our budget while the 5 credit card crew gives you $1,712. This is a $706 increase over the City Double Cash credit card.

Annual Credit Card Spending by author

However, there is one thing I should probably tell you. The Citi Double Cash Credit Card is not the best solo credit card.

If you’re hell bent on just using one workhorse, no bonus boys. Then click HERE to see the ultimate workhorse credit card.

Catch you on the flip side.

Reply