- The Moneycessity Newsletter

- Posts

- Are Annuities a SCAM and Should You Get One?

Are Annuities a SCAM and Should You Get One?

Annuities receive A LOT of hate online, but is it really justified? Various types of annuities claim to solve different issues that a portfolio might face in retirement. I researched what actually goes wrong in retirement and whether or not the annuity is the right tool for the job.

Brian Glass

July 22, 2024

Is it true that all annuities are scams?

If you are near retirement, or you know somebody who is, then you’ve probably heard the term.

An annuity is just a service where I give my money to someone else, they invest it for me and pay me out over time.

These providers are profitable, otherwise they wouldn’t provide the service. The problem is that their profit comes directly out of my nest egg.

Success for the provider means that they’re paying me as little as possible and keeping as much of my money for themselves as possible. But there is a way to beat the system. There is a way to get more out of the providers than the providers get out of you.

On the go? Watch the video HERE.

Are Annuities a Scam?

How They Make Money Off Of Me?

Annuities make their money in three ways.

First, they will charge you fees over time for managing your investments and paying you out.

Second, they might cap your returns. If the annuity is linked to the market and the market goes up by 10%, they might only pay you out 8.5%.

Third, some annuities will NOT return your money to your beneficiaries upon death. Not getting your money back when you die sounds scary, but more on this one later.

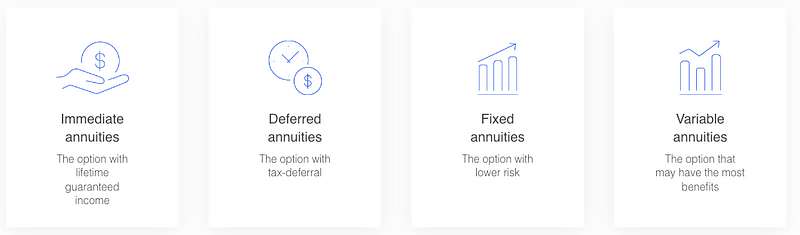

Four Types of Annuities

First, there are immediate annuities where you pay your premium upfront and then the provider immediately starts paying you a certain percentage each year.

Second, there are deferred annuities where you pay the premium and then after some years, the provider begins paying you out. It could be that you receive a set rate each year or you receive a lump sum based on how much money that annuity made during the deferral period.

Third, there are fixed annuities where the rate of return over time is a flat rate. The fixed annuity can apply to either immediate or deferred.

Finally, there are variable annuities where the rate of return is linked to an index of some kind. You’ll get a greater payout if the market does well, and you’ll get a lower payout if the market does poorly.

Four Types of Annuities

Why Would I Want an Annuity?

So the question is, why would you want an annuity? Annuities provide an insurance policy. They take some of the risk off the table.

The standard retirement portfolio is 60% stocks and 40% bonds with a withdrawal rate of 4% every year and then adjusted for inflation every year after that.

Historically, this portfolio has had a 10% chance of failing over a 30-year retirement. But, in today’s market conditions, new projections show a 57% chance of failure.

Is the 4 Percent Rule Working for Retirement Portfolios?

This scares a lot of retirees. They want to take some of that risk off the table for a small cost. Generally, an annuity will lock in a set amount of money for life at the expense of losing potential gains.

If the market does really well, you get a lot of benefits from having 60% stocks. Unfortunately, really good stock market performance is not guaranteed.

Before I can decide which annuity is best, I have to understand what ways a traditional portfolio will fail. Then, I have to pick the annuity that counters that failure scenario the best.

How do Retirement Portfolios Fail?

Sequence of Return Risk

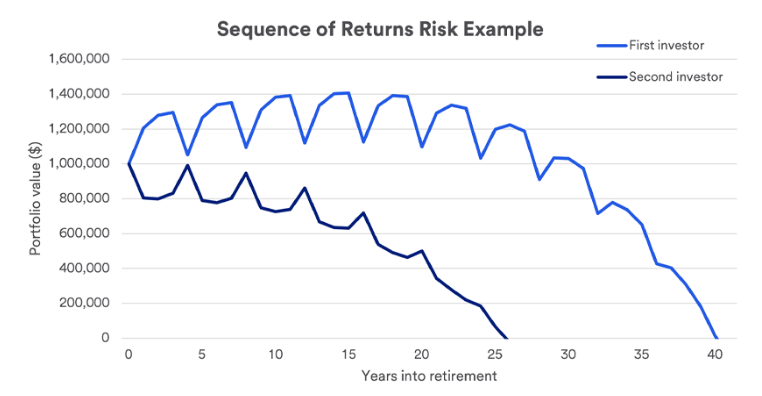

The first way that your retirement portfolio is likely to fail is through the sequence of return risk.

On average, the stock market does go up over time, but there will be periods of bad returns and negative returns. If you have the bad returns first, at the very beginning of your retirement, while you’re drawing it down, this is a recipe for disaster.

Your portfolio is more likely to run out of money if you have negative returns right off the bat. If we look at the chart below, the two different scenarios have the exact same returns happening in different orders.

Sequence of Return Risk

The first investor (light blue line) has a 25% return in the first year, a 10% return in the second year, a 5% return in the third year, and then a 15% loss in the fourth year. The pattern repeats until the portfolio fails in year 40.

The second investor (dark blue line) has a 15% loss in the first year, then a 5% return, then a 10% return, and a 25% gain in year four. This pattern repeats until the portfolio fails in 26 years.

In order to counter the sequence of return risk, I need my annuity to be insulated from the market. So I don’t want an annuity that has variable returns.

If my annuity is going to give me less of a payout when the market does poorly early on, then it’s not fixing the problem of sequence of return risk.

To counter the sequence of return risk, I need a fixed annuity.

Inflation Risk

The second way that a retirement portfolio commonly fails is from inflation risk.

If your basic expenses are $40,000 a year and then you experience 10% percent inflation, your expenses in year two will be $44,000.

And then if we have another year of 10% inflation, now you’re annual expenses are $48,400. It is easy to see how high inflation can get out of hand quickly.

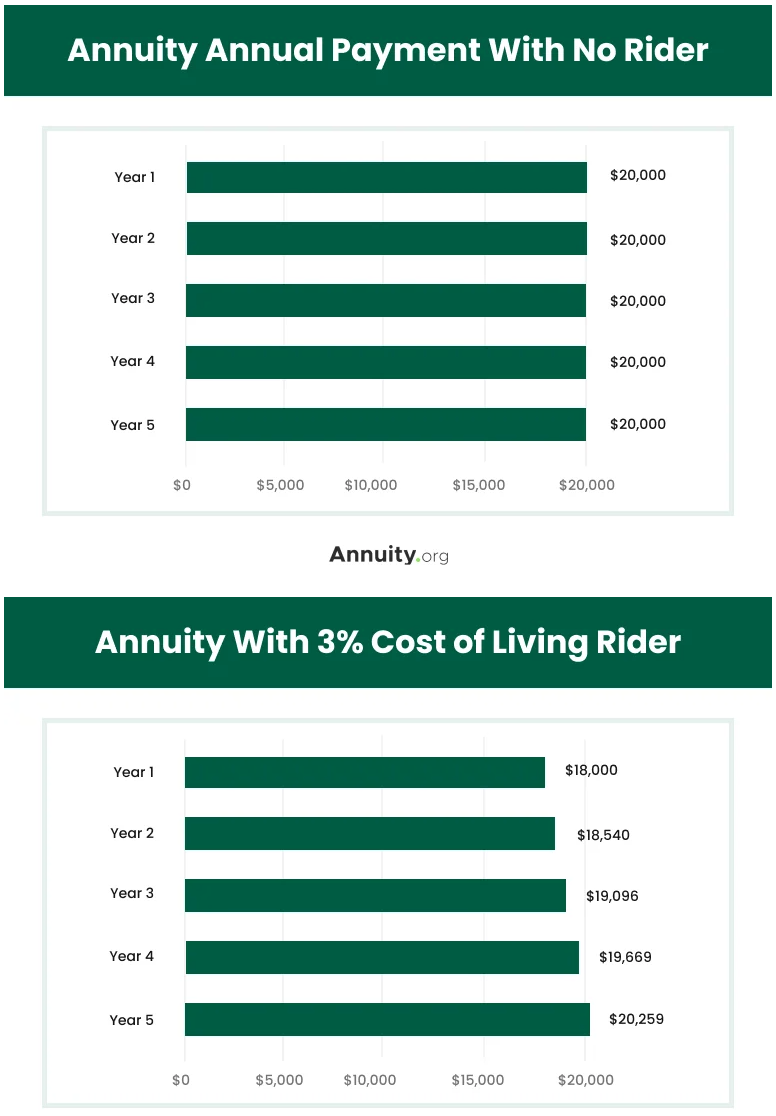

The way to counter inflation risk is not with a fixed annuity alone. With a fixed annuity, your flat payout over time will be diminished. We have to add a cost of living adjustment to the fixed annuity.

The example below compares the payout of a fixed annuity to a cost of living adjusted (COLA) fixed annuity.

Cost of Living Adjustment Rider

The COLA annuity starts with a lower initial payout but begins paying out a higher rate in year 5. The sum of all payouts for the COLA will still be lower in year 8 or 9, but will soon surpass the fixed annuity.

Adding a COLA Rider to a fixed annuity will cost more upfront, but is necessary to mitigate the inflation risk.

Longevity Risk

The third major risk that retirees face is longevity risk. If you live a really long time, which is a good problem to have, then you are much more likely to run out of money.

If I live longer than my life expectancy, then there is a chance that I will draw down your portfolio of 60% stocks and 40% bonds to $0.

Earlier I mentioned the death annuity and how it sounded scary. Ironically, it is the perfect solution to living a very long time.

The annuity provider is only willing to return your principal investment to your heirs for a price. The extra price results in a lower annual payout every year. Meaning, you have to pay more for the same return.

If you go with the death annuity, then you don’t have to put as much money down. The provider is going to give you a higher payout because they’re expecting to get that money back from you when you die.

Now, if you live a long time, then you get to benefit from that higher payout for many years. Thus, taking care of the final risk that your retirement portfolio might experience.

Losing your money in death does sound a little counterintuitive, but I have to remember that I want the higher rate for as long as I am alive.

I don’t want the annuity that pays me back in death. I want the annuity that gives me the most benefit if I live a really long time.

What Should I Do?

First of all, I do not plan to buy an annuity while I’m young. I want to be as invested as possible in the stock market.

As long as I am not taking money from my investments, I can easily ride out the periods of loss and benefit from the periods of high returns. This will give me the best chance of maximizing my wealth accumulation.

The second thing I’m going to do is invest in my health as much as possible. I want to have the problem of longevity risk.

When the annuity provider is calculating how they’re making money, they’re looking at averages. The provider is assuming the average person is going to die on the day of their life expectancy.

The people who die younger pay for the people who live longer. If I want to counter longevity risk, I want to be in that longer living category.

To do that, I’m going to invest in my health while I’m young. This is a win-win scenario in every way because I’m going to have I’m going to have a longer lifespan, a longer health span, and more annuity returns.

The third thing I’m going to do is purchase an annuity for a very specific purpose when I reach retirement age.

I’m not using all my money to buy a massive annuity. I’m going to pay for the bare minimum to cover my basic expenses. This calculation will absolutely include social security.

Social Security is a Death Annuity with Cost-of-Living Adjustment (COLA)

Social Security is an annuity that you pay for throughout your life, it has a cost of living adjustment, and when you die… it’s gone.

Social Security is basically a death annuity with a COLA!

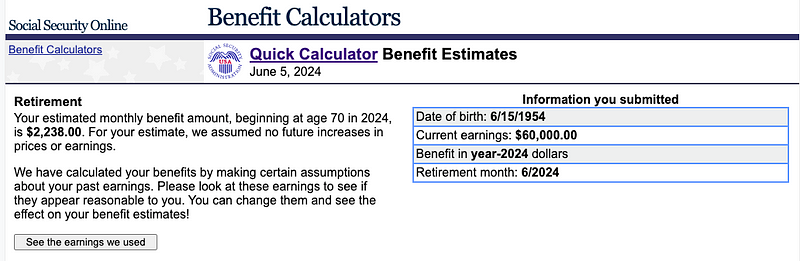

The benefits calculator below assumes I begin payments at age 70 for maximum benefit, my working salary was around $60,000 per year, and this results in a monthly payment of $2,238.

$2,238 per month comes out to about $27,000 per year.

Social Security Estimator

If that’s a little bit low for me, if I don’t think that can quite cover my bare minimum expenses, then I will buy an annuity that just covers the difference.

If, at the minimum, I need $40,000 a year to be comfortable, then I will pay for a COLA Fixed Annuity that pays me $13,000 per year.

That being said, if I have a pension from a company that I worked for, it may not make sense to buy an annuity.

The extra money from the pension might already make up the difference between what I need and the social security. That way, I can let the rest of my nest egg ride on the stock market and the bond market to pay for all of the extra stuff I want — the vacations, the travel, the toys, etc…

So What Now?

The main benefit that people get from an annuity is happiness.

You don’t have to worry about the fear, uncertainty, or doubt that the stock market might crash. You won’t have to use some of your fun money to fund your basic expenses, to keep a roof over your head, or food on the table.

It is so hard to just spend freely and have a good time when the possibility of failure in retirement is just looming over your head.

The primary reason for the annuity is because, in the end, planning for your happiness is the most important thing.

Many people are miserable in retirement, even though they’ve achieved financial independence and riches.

If you’re interested in planning for your happiness, I shared the stories of those who are miserable with financial independence and the lessons they wish they learned before it was too late.

Check it out HERE.

Catch you on the flip side.

Reply