- The Moneycessity Newsletter

- Posts

- 46% Americans Invest Their 401K WRONG (And How to NOT Be Them)

46% Americans Invest Their 401K WRONG (And How to NOT Be Them)

46% of Americans make critical mistakes regarding their 401(k) plans. Learn how to avoid high fees, understand the implications of early withdrawals, and make informed choices to optimize your retirement savings strategy.

Brian Glass

September 08, 2024

If I hadn’t made one small change to my 401k, I would have missed out on over $200,000 by the time I retired.

I made a mistake when I started early on. Your 401k is one of those things that you don’t have to think about very often when you’re young. It’s so easy to set it up in a rush when you start your new job and forget about it.

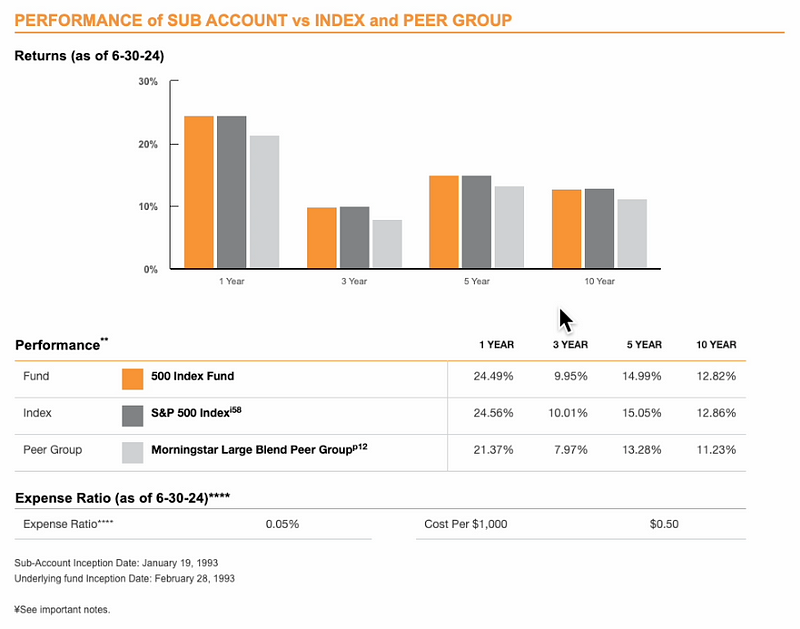

So I set up all my future contributions to go into an S&P 500 index fund which is normally a great idea. It’s got a solid historical 10% average annual return. It’s got typically very low expense ratios until I looked down the list at more of the details and found a problem.

On the go? Watch the video HERE.

46% of Americans are Messing up Their 401K

Problem #1: Picking Funds with High Expense Ratio

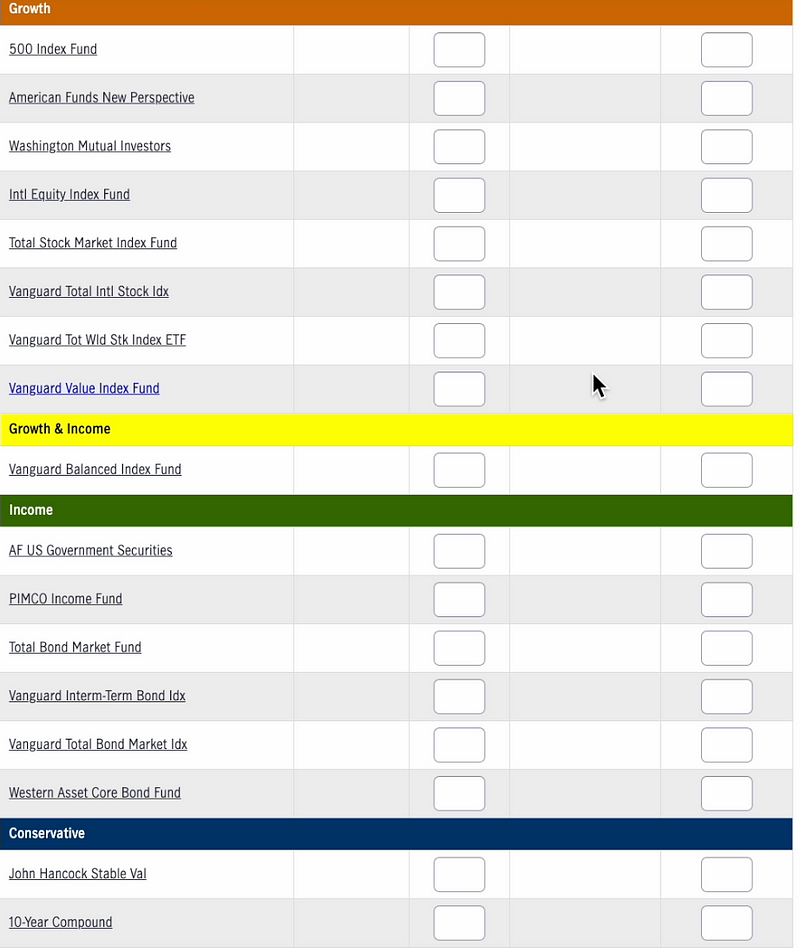

This is my John Hancock 401k portal where it shows me my different investment options. We can see we have different categories, target date, target risk, and aggressive growth.

Let me scroll down to the growth section. This is where I found my first fund that I invested in which is the 500 index fund.

When I pull that up, it’s all large companies and we have a blend of value and growth.

And when I scroll down this first instance of expense ratio, it shows 0. 05%. This is the type of expense ratio that I would want. However, when I scroll down a little bit further, I think this is a little bit deceptive.

There are two other expense ratios, gross and net. The gross expense ratio includes the expense ratio of the fund but it also reflects any fees and other expenses that the fund might incur. This is how much you could actually pay in maximum. And the net expense ratio is how much I actually paid over the last year. So they may have waived some fees or maybe they capped the fees off at a certain point.

If I’m choosing a fund to invest in, I’m going to assume the gross expense ratio, and I’m going to plan on paying that amount. So I’m looking to find a fund that has a much lower gross expense ratio and after this, I’ll show you how much this actually adds up to over a long investing time horizon.

The Target Date funds are great, especially from Vanguard. They have very low fees, and they will automatically rebalance your portfolio to have a greater percentage of bonds and other fixed-income assets as you get closer to retirement.

This is great for some people. Personally, I don’t like it because I want to have complete control over my investments so I will pass on those.

The first funds that they highlight for targeting risk are John Hancock funds. So these are the ones that they might push you into. They might come out and say: what kind of target risk do you have? If you come out and you say: I want to target growth because I’m going to be investing for a long time. This could be a fund that they point you towards.

These funds also have the highest expenses. If I click on the John Hancock Multi-Manager growth fund, right off the bat, the expense ratio shows 0.62% which is way too high.

When I scroll down to the key statistics, the gross expense ratio and the net expense ratio are 1.02% which adds up to be so much. I can’t wait to show you how much this will actually add up to over time.

This is the upper end of expense ratios that you might see in a 401k and you absolutely want to avoid that.

The next fund that has kind of the middle of the road expenses around 0.5%. That would be the S&P 500 one that I stumbled into on accident the first time. Unfortunately, they did not have an S&P 500 Vanguard fund so what I did was combine 50% Vanguard growth fund and 50% Vanguard value fund to get a similar allocation of stocks as the S&P 500.

So first when I scroll down to the Vanguard growth index fund, you can see it has a 0.05% fee in the expense ratio. And then when I scroll down to the gross and net expense ratios, they are the same, both 0.05%.

So by just simply combining the growth fund with the value fund, I was able to get a tenth of the expenses as the John Hancock S&P 500 fund.

So this fund up here at the top, it shows the asset class investment style. This is large-cap growth. And just to show you an example, when I go to the Vanguard value fund, this is comprised of large-cap value companies. So a simple 50/50 split gives me exactly what I want for a fraction of the cost.

How Does the Expense Ratio Affect My Bottom Line?

If I assume that I’m investing from the age of 25 to 65, that’s 40 years, $300 a month, with a 10% average annual return, I should expect to end up with $1,665,000.

That’s pretty good. But if we have a 1% expense ratio, now this is the more egregious funds, what that ends up being is now instead of a 10% average annual return, now I’ve just got a 9% average annual return. And the end result after 40 years, now I only have $1,265,000. That is a $400,000 difference. That is 26% less money at the end of the day just because of a 1% expense ratio. That is insane.

So that’s on the very high end of expense ratios. The fund that I was almost in until retirement was the S&P 500 index fund. It had a 0.5% expense ratio. If I reduce the return to 9.5% per year for 40 years, now my ending balance is $1,451,000. This is a $214,000 difference.

In reality, it would have ended up being more for me because this is assuming that I’m staying with $300 invested per month, every month. I would slowly be getting raises. I would be putting more and more money into my 401k and that would result in more and more losses. So $200,000 is really just the lower end for what I would have been leaving on the table.

Finally, the fund that I did end up going with had an expense ratio of 0.05% which is what I like to shoot for with all of my index funds and ETFs that I invest in. After 40 years, the average annual return of 9.95% per year leaves me with $1,642,000. So this is just $23,000 in total. I would be losing 1.5% of my total investment. That’s not so bad, especially over a 40-year period.

So that is just the first issue. That’s the first main problem that people have when they’re selecting their 401k if they’re not doing it carefully or if they let their 401k provider do it for them.

Problem #2: Withdrawing Early

The second major pitfall that people experience with their 401k has to do with taking money out.

1. Income Tax on Interest

Most people are familiar with the early withdrawal penalty. If you take money out before you’re 59.5, you pay 10% plus that money gets taxed at your ordinary income tax bracket.

Most people know that’s bad so they think they can get around all the expenses by doing a 401k loan. But there’s a major misconception here. By paying interest to yourself instead of to the bank, you’re effectively paying double taxation on your interest payment.

In the case of a $50,000 loan, you can expect to pay $13,372 in interest over 5 years. The $13,372 is the amount that gets taxed twice. It is deposited into your traditional 401k account post-tax and then gets taxed a second time when you withdraw.

You have already enjoyed a tax benefit from the $50,000 when it was originally deposited into the traditional 401K account.

Let’s say you’re in the 12% tax bracket, you’re losing 12% of your interest payment that would have gone to the bank.

12% TAX + $13,372 INTEREST = $1,605 LOSS IN TAXES

So that is an improvement, but it’s not the only expense. You also have opportunity costs when you pull money out of your 401k because you are losing out on the market gains.

2. Opportunity Cost

On average, we can expect the S&P 500 to have 10% gains per year. So whatever money you pull out, you’re going to be losing 10% of that money every year. But what if the market doesn’t go up?

Sometimes the market goes down in a year and you’ll be really happy that you took that money out. However, in some years the market might go up by 100% and you’ll be really sad that you took money out in those cases. So it’s really just a game of averages.

401K Loan Repayment Period

Over the 5-year period which is typically how long you have to pay back your loan, the market is going to go up by an average of 10% per year.

3. Job Termination

Another major problem with taking money out in the form of a loan is the case of losing your job, you no longer have 5 years to pay it back. You only have 90 days.

And if you don’t pay it off in 90 days, whatever loan is left on the account is going to count as an early withdrawal and you’re gonna take a 10% hit on that money.

Problem #3: Not Knowing How to Pick Funds

The third major pitfall that 401k investors fall into is not knowing how to pick funds.

With my 401k provider, they have it divided into easy-to-understand categories. You’ve got aggressive, you’ve got growth, you’ve got conservative. So somebody might erroneously think: Hey, I’m a conservative guy. Maybe I just want a conservative investment. I don’t like to gamble. This shows a consistent return of 2% to 3%. I’ll go with that.

The problem is you are still taking a major risk. You’re still taking a major gamble on inflation. Some years inflation is as high as 15%, some years it’s as low as 0%, or maybe even slightly negative. But on average, inflation is about 2.5%.

Even when you think you’re being conservative, you are still setting yourself up for failure if you don’t know what you’re looking for and if you don’t know the type of returns that you need at different stages in your life.

In this case, you could expect 2.5% inflation. The expense ratio of this fund is 0.42%. So you are, you’re not guaranteed, but you are likely to lose 2.92% on this fund due to a combination of inflation and the expense ratio.

2.5% INFLATION + 0.42% ER = 2.92% LOSS ON AVERAGE EVERY YEAR

Whereas the return, historically, it has not broken above 3%. So with this fund, it seems like you’re likely to lose money.

So What Now?

Picking out funds that are obviously bad is one thing. And picking out funds that are consistently going to perform well is another thing altogether. Check out this video HERE where I go over my method for evaluating index funds and ETFs that tend to outperform the S&P 500.

Catch you on the flip side.

Reply