- The Moneycessity Newsletter

- Posts

- 2024 is ENDING: Make Your Greatest Comeback in 2025

2024 is ENDING: Make Your Greatest Comeback in 2025

The next 30 days can set the stage for your greatest financial comeback with strategies to reset, automate savings, and start investing confidently. Discover actionable steps to take control of your money and prepare for a successful new year.

Brian Glass

December 24, 2024

The next 30 days can define your entire next year.

The clock is ticking, and the decisions you make could set you up for the greatest financial comeback of your life. Last year may not have gone the way you wanted. Maybe you missed some goals or you feel stuck, but I’m going to share three powerful strategies to reset, rebuild, and come out stronger than ever in the new year, no matter where you’re starting from.

Watch the extended version HERE.

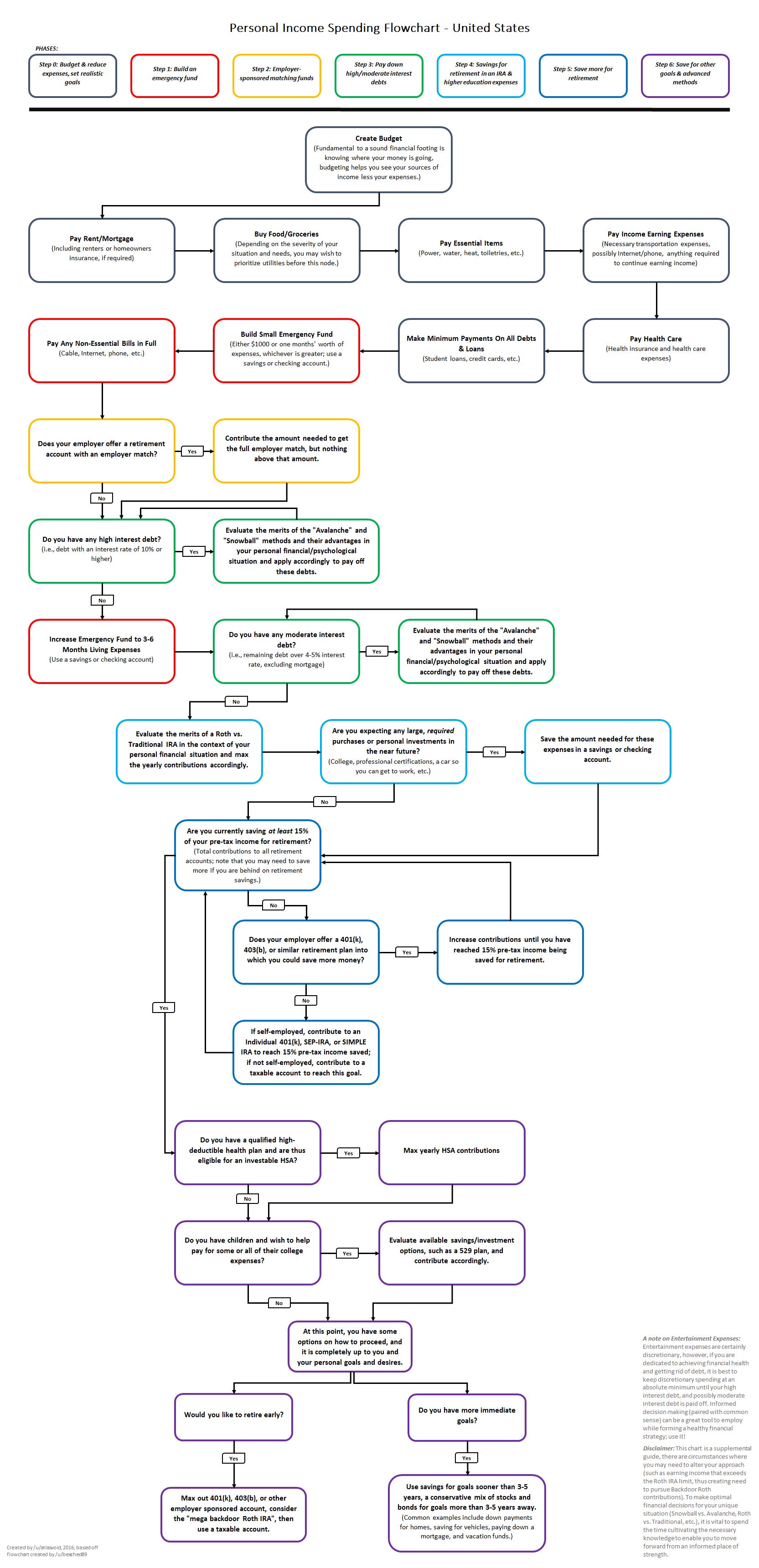

1. Master the Basics of Personal Finance

If you’re feeling like your money didn’t go far enough last year, there are two ways to address it. Sure, earning more can help, but without a plan, it’s like trying to outwork a bad diet — it won’t work long-term. Eventually, we all want to stop working, and if I haven’t managed my money wisely, even earning a lot won’t save me.

That’s where the Prime Directive comes in. It’s a step-by-step guide for managing every dollar, created by the Personal Finance subreddit. Here’s how it works:

Level 1: Essentials

Start by budgeting. It’s not fun, but it’s necessary to know where your money is going. Cover basics like rent, utilities, food, healthcare, and minimum debt payments. This keeps your finances stable and your credit intact.

Level 2: Emergency Fund

Save $1,000 or one month of expenses, whichever is greater, to handle small emergencies. Then, pay off non-essential bills like cable or a fancy phone plan if they’re not part of your income-earning essentials.

Level 3: Employer-Matching Funds

If your employer offers a retirement match (like a 401(k)), prioritize this next. Contributing enough to get the full match is like getting an instant raise — most employers match 50% of your contribution up to 6% of your salary. This is free money you don’t want to leave on the table.

Level 4: High-Interest Debt

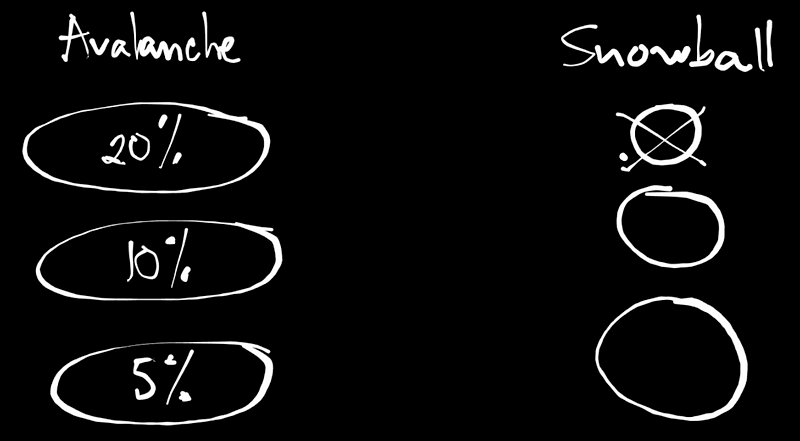

Next, tackle high-interest debt, typically anything above 10% like credit cards. Use the avalanche method (paying off the highest interest rate first) for faster results or the snowball method (starting with the smallest balances) for psychological wins. Both work, so pick the one that keeps you motivated.

After clearing high-interest debt, go back to Level 2 and build your full emergency fund — three to six months of expenses, depending on your job security and potential big-ticket costs. Then, move on to moderate-interest debt (4–10%).

Level 5: Retirement and Short-Term Savings

Here’s where things get interesting. Add more to your retirement accounts, choosing between a traditional or Roth IRA based on your tax situation. If you have big expenses coming up — like buying a house or a car — keep that money in a savings or checking account instead of investing it. The stock market is too unpredictable in the short term for money you’ll need soon.

Beyond Level 5

Levels 6 and 7 dive into extra retirement savings and advanced strategies, but reaching Level 5 is already a strong financial position. From there, you can customize based on your goals.

The Prime Directive has been a game-changer for me. It keeps my finances on track and ensures every dollar is working toward something meaningful. Following these steps builds a strong foundation that sets me up for long-term success.

2. Open an Investment Account

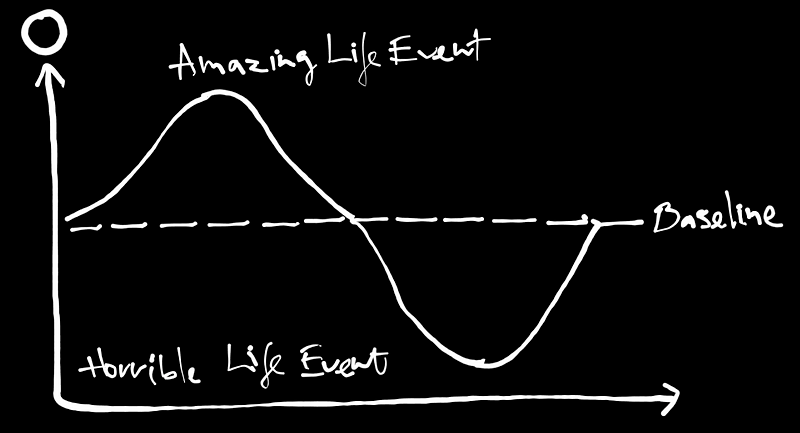

The best way I’ve found to save money takes advantage of a natural human ability: we adapt to almost anything. Studies show that once someone earns more than $75,000, extra money doesn’t significantly boost happiness. This is thanks to hedonic adaptation — our tendency to return to a baseline level of happiness after both amazing and terrible events.

When I get a raise, it’s tempting to spend more and enjoy that initial spike in happiness. But I know it’ll fade, and my spending will just lock me into a higher cost of living. To avoid this, I automate my savings. Every time I get paid, a portion of my paycheck goes directly into my savings and retirement accounts. By keeping my spending habits the same, I adapt to my current income while saving more for what really matters later.

With my plan in place and savings automated, it’s time to focus on building the best investing strategy.

3. Build Your 2025 Investing Plan

If you are feeling overwhelmed by the thought of investing, the simplest investing approach can be explained in three steps.

First, understand the spectrum of investing, as explained in The Intelligent Investor by Ben Graham. On one end is active investing — high effort, requiring skill and expertise to beat the market. It can work, but there are no guarantees. On the other end is passive investing — low effort, diversified, and focused on getting average market returns. Surprisingly, being fully passive often outperforms many active investors.

To start passive investing, I look for a diversified, low-cost index fund or ETF. A great example is the S&P 500, which tracks 500 of the largest U.S. companies and has delivered average annual returns of 10% over the last century. SPY is a popular fund with an expense ratio of less than 0.1%, meaning almost all my money stays invested. High fees, even just 2%, can eat up half my savings over decades, so keeping costs low is critical.

Consistency is the key to success. I don’t wait to save up a lump sum — I invest small amounts regularly. While investing all at once may be mathematically optimal, it’s tough psychologically if the market drops immediately. Spreading out investments makes it easier to ride out market swings and stick with the plan.

Finally, it’s important to use the right accounts. Retirement savings go into accounts like 401(k)s, IRAs, or HSAs, while general investing can go into brokerage accounts. Each account has unique pros and cons, so picking the right one is essential for maximizing returns so check out this video HERE to see the full breakdown on the traditional, Roth, and HSA accounts.

Cheers!

Reply