- The Moneycessity Newsletter

- Posts

- #1 Investor Peter Lynch Reveals The Worst Thing to Do With Your Money

#1 Investor Peter Lynch Reveals The Worst Thing to Do With Your Money

Peter Lynch does not believe in diversification. Does this mindset only apply to elite investors? Or can average investors like myself benefit as well?

Brian Glass

November 01, 2024

“I don’t believe in diversification at all. I would own one stock… if I could find one great stock. Diversification is a big mistake. I call it di-WORST-ification.” — Peter Lynch

Peter Lynch talks big about Di-WORST-ification, but he has one phrase in there that was doing the heavy lifting: “IF I could find one great stock.”

That’s the trick, isn’t it?

Peter Lynch is saying a lack of diversification is a privilege. Don’t think you can just forgo index funds without the FINDING.

I am left with more questions after hearing Peter’s words of wisdom. Luckily for me, he goes on to explain how the common man, like myself, might FIND one great stock.

On the go? Watch the video HERE.

#1 Investor Peter Lynch’s Investing Advice No One Wants to Hear

Do I Really Need to Diversify?

Peter Lynch doesn’t start with one stock, he starts with several “top” stories. He says “ten” but the exact number isn’t important. The number of compelling stocks you find will depend on how much time you have to research companies.

But isn’t buying ten companies diversifying?

While I do agree that buying ten companies is more diversified than buying one, there are 2 big distinctions to make here.

First Distinctions

First of all, traditional diversification means you are buying many companies in every sector of the economy. Investments in every sector are made to mitigate the damage if a single sector takes a big hit.

For instance, if I owned 100 different stocks but they are all oil and gas companies, then my portfolio would take a major hit if regulations are passed limiting fossil fuels.

Sectors of the Stock Market

And I couldn't just own one company in each sector because I would not be protected from individual risk to that specific company.

For instance, a single company in a sector could be severely damaged by lawsuits if an employee gets hurt on the job while the rest of the sector is flourishing.

So I would want to own many companies in every sector to ensure that my only major risk is market risk. My portfolio should only go down if the whole market is going down on average.

Peter Lynch is NOT talking about that kind of diversification. He makes no distinction between different sectors or different companies that are highly correlated. Peter Lynch is hunting for just a handful of standout companies wherever he can find them.

Second Distinction

The second major distinction between Peter Lynch’s “ten stories” and traditional diversification is the filter aspect. Peter is starting with ten but he is filtering that list down as he sees the different stories play out. He might only end up with one company in the end.

In the short term, the stock market will go up and down in a seemingly random and volatile way. The volatility presents opportunities as one company may drop in stock price while another increases with no material change to the company's situation.

Peter Lynch will sell off shares in both underperforming companies and overpriced companies while loading up on the cream of the crop. So Peter will start with ten and narrow them down to just oneif the situation presents itself.

But how does he come up with his short list of ten or so solid stories?

How Do I Find a Great Company?

The first step is qualitative research that leverages your natural advantage.

What are the quality companies in your industry?

What are the quality companies that you interact with outside of work?

What are the quality companies that you see expanding and growing in your area?

Asking myself these 3 questions gets me a list of companies that I know, that I like, that I see growing, or all of the above. It doesn’t take very much effort or time out of my day to be conscious of the companies around me.

Maybe you aren’t ready with a list of companies off the top of your head, but you can start being more conscious as you go about your daily life.

I used to think investing had to be so complicated. But it doesn't have to be. Successful investing starts with identifying great companies any way you know how.

Peter Lynch points out that you didn’t have to get in early, it could have been 10 years after Walmart went public and you still would have 50X your money. You just have to start with a good story.

Let me run with the Walmart example for a minute.

I live in Texas and a huge grocery store in Texas is HEB. I love shopping there, everyone loves shopping there, it's almost always packed. This is a great story and they have 339 stores only in Texas! Unfortunately, this company is private so I cannot invest. But if they ever went public, this would be the first company I look at investing in.

For a publically traded example, I recently went to Costco for the first time. Yes, I am late to the party. Everyone raved about it and I was stubborn. That store was BADASS.

It is a great company with a great business model. You have to pay for a membership just to get in the store so they are making money on you before you even walk in. And I was happy to pay it because the good prices make up for the membership.

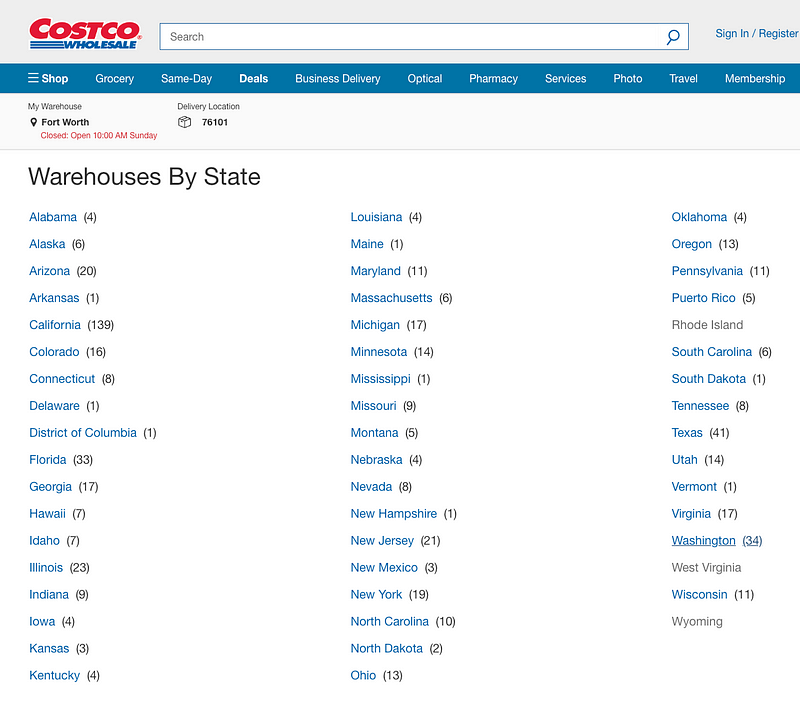

Costco Store Locations by State

Anyway, when I look at the map, Costco has roughly 600 stores with the largest chunk is in California with 139 stores and second place being Texas with 41 stores. Most of the states have just a handful and a few have none at all so it’s not overly saturated. There’s still a lot of room to grow.

Top Grocers in the USA

When I compare to the other top grocery stores in the US, Walmart has over 5,000 stores. Kroger and Albertsons have over 2,000 stores. Costco has a long way to go and they’re not stopping at the United States. They also have stores in other countries as well.

Costco’s Global Presence

So I have established that I think Costco is a great story as Peter Lynch says. Does that mean I go ahead and buy a large position in Costco today?

No.

I still have to determine if now is a good time to buy.

Is Costco overpriced?

Is Costco underpriced?

Is Costco fairly priced?

How to Know If a Company is Overpriced?

If Peter likes a company at a fair price, he still won’t buy it. He waits for a haircut. He wants the stock to drop down to at least slightly underpriced.

In Peter Lynch’s book One Up on Wall Street, he gives a simple formula to determine when a stock is priced fairly. This way, I can make a short list of companies that I have great experiences with, and then I can apply the formula to see if any of these companies are underpriced, fairly priced, or overpriced.

Let’s keep rolling with the Costco example to see if now is a good time to buy according to Peter Lynch’s pricing model.

Peter Lynch’s formula only requires three terms:

Earnings per share Growth

Dividend Yield

Current P/E Ratio which are super easy to find on Yahoo Finance.

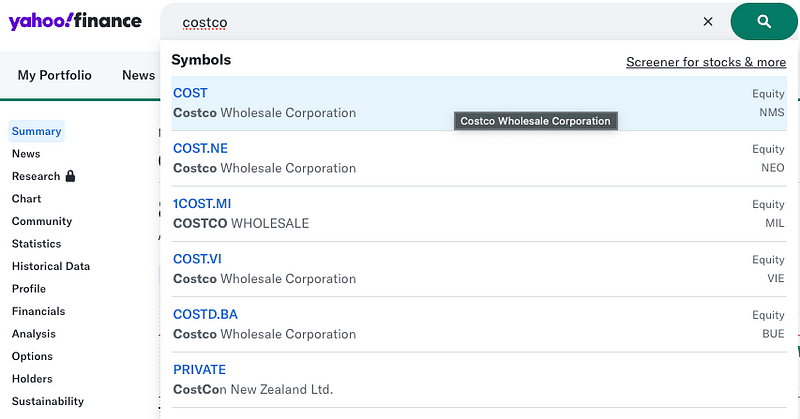

All three numbers can be found on Yahoo Finance. First, I will type in “Costco” in the search bar and then select their ticker “COST” in the drop-down menu.

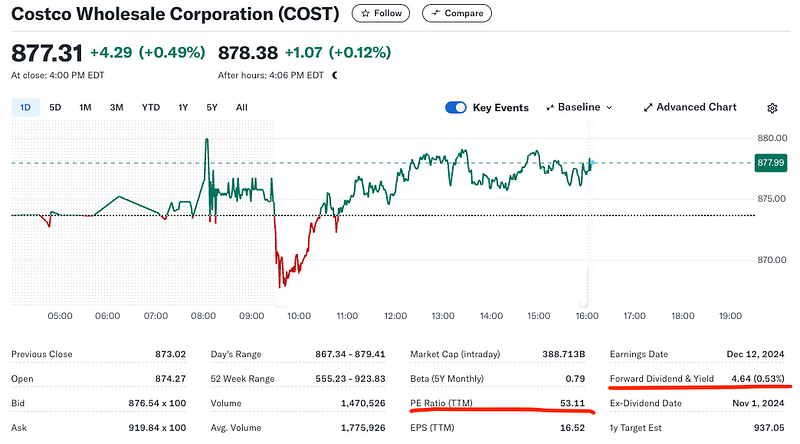

The second two numbers can be found straight away on the Summary tab.

PE Ratio (TTM) which stands for trailing (previous) twelve months is 54.11 currently.

Forward Dividend and Yield is 0.53% currently so we’ll use 0.53.

To find the first number, we will go to the Analysis tab and scroll down to the bottom where we can find the Growth Estimates area.

Next 5 years (per annum) is estimated to grow by 9.87% per year so that’s a score of 9.87.

Now that we have the three numbers, the equation is super simple as well. All I need is the calculator app on my cell phone and I can perform this.

(EPS Growth + Dividend Yield) / PE Ratio = Peter Lynch Number

For Costco, the Earnings Per Share Growth is 9.87 plus the Dividend Yield of 0.53 gives us 10.40. Then we divide that by the current PE ratio which is 54.11, and we get a score of 0.19.

According to Peter Lynch, a higher score is considered better. When Peter Lynch wrote his book, he would target companies with a score of 1.5 or higher. Any company with a score 1.0 or lower, Peter Lynch considered to be overvalued.

Therefore, although Costco is a great company, Costco is very overvalued right now and it is not a good time to buy.

For that to change, either Costco’s share price needs to go down or their expected future earnings and dividend yield needs to go up or both of those things could happen. That would be ideal.

Small Caviat

Many investors today argue that Peter Lynch’s numbers are too low for today’s market and that it’ll be too difficult to find companies with a score of greater than 1.5.

I think there is some truth to this. I like to target companies with a score of greater than 1.0 instead of greater than 1.5 to account for the fact that markets have gotten more expensive over time.

Now, that still doesn’t change Costco’s fate since they have a score of 0.19. That’s still very overpriced so I’m going to keep waiting on Costco.

That being said, there are still some companies today with very high scores. Take Toyota Motors, for example.

They have an earnings per share growth estimate of 16.8% which is really high, a dividend yield of 2.26%, and a PE ratio of just 6.9 which is very low. This gives them a score of 2.76 which is huge and puts them into the very undervalued category.

(16.8 + 2.26) / 6.9 = 2.76

However, although the number looks great on paper, I don’t have much experience with Toyota so I don’t know if it’s a great story like Peter Lynch is looking for. If you do have a lot of experience or if you’re willing to do some research into Toyota, it could be a great purchase right now.

So What Now?

If you have never done extensive research on a company before, you can check out this video HERE to see my process for reference.

Catch you on the flip side.

Reply